아연 도금 및 코팅 철 및 강판 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

Galvanized And Coated Iron and Steel Sheets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1750506

리서치사:Global Market Insights Inc.

발행일:2025년 05월

페이지 정보:영문 225 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

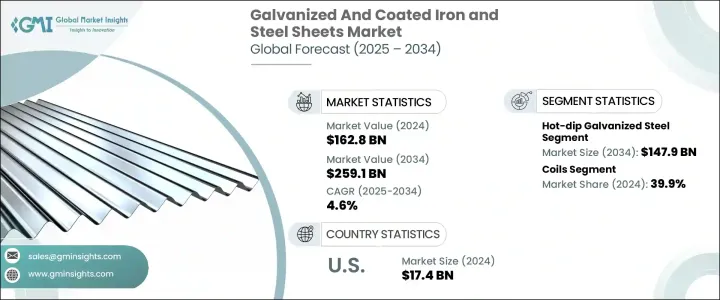

세계의 아연 도금 및 코팅 철 및 강판 시장은 2024년에 1,628억 달러로 평가되었고 자동차, 건설, 소비재 등의 산업에서의 수요의 급증에 의해 CAGR 4.6%를 나타내 2034년까지는 2,591억 달러에 이를 것으로 추정되고 있습니다.

선진국과 신흥 경제 국가의 급속한 도시화와 산업 확대가 내구성과 내식성이 뛰어난 강재 수요를 뒷받침하고 있습니다.

게다가 내식성, 내구성, 미관을 향상시키는 고도의 표면 처리의 개발에 의해 아연 도금 및 코팅 철 및 강판의 응용 범위가 확대하고 있습니다. 친환경 건축재료와 제조재료를 요구하는 규제의 압력과 고객의 요구의 고조와 일치하고 있습니다. 그 결과, 이러한 기술 혁신은 성능을 향상시킬 뿐만 아니라 지속가능성 기준에의 준거를 서포트해, 건설, 자동차, 공업용도로의 사용을 세계적으로 매력적으로 하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

1,628억 달러

예측 금액

2,591억 달러

CAGR

4.6%

이 시장에서는 용융 아연 도금 강판이 계속해서 가장 널리 사용되고 있는 도장 기술입니다. 장기적인 부식 보호, 합리적인 가격에서 발생합니다. 용융 아연 도금은 아연과 강철의 결합을 형성하고 가혹한 환경에서도 차폐 역할을 하기 때문에 농업, 인프라, 운송, 산업 프로젝트 등에서 충격이 큰 용도에 이상적인 재료입니다.

코일 모양의 아연 도금 및 강판은 운송의 용이성과 재고 비용 절감으로 인해 대규모 사용자들 사이에서 여전히 인기있는 옵션입니다. 이러한 특성으로 인해 자동차 생산 라인, 모듈식 주택 프로젝트, 조립식 구조물에 있어서 합리화 작업에 최적입니다.

미국의 아연 도금 및 코팅 철 및 강판 시장은 2024년에 174억 달러가 되었고, 2034년까지의 CAGR은 4.9%를 나타낼 것으로 예상됩니다. 견조한 수요를 견인하고 있는 것은 내식성과 재료 수명의 연장이 중 주요 요건인 이 나라의 자동차 및 인프라 섹터의 확대입니다. 교량, 상업 빌딩, 수송망 등의 프로젝트에서는 다양한 환경하에서의 탄력성과 성능에 의해 이러한 강재의 채용이 계속되고 있습니다.

이 시장 주요 기업은 POSCO, ArcelorMittal, Baowu Steel Group, TATA Steel, Nippon Steel Corporation 등이 있습니다. 이러한 기업은 첨단 아연 도금 기술에 대한 투자, 생산 능력 확대, 최종 이용 산업과의 전략적 파트너십 형성을 통해 경쟁력을 강화하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

아연 도금 및 코팅 철 및 강판 : 기초와 진화

아연 도금 및 코팅 철 제품의 정의와 분류

코팅 기술의 역사적 개발

원재료와 구성

베이스강의 유형과 특성

아연 및 아연 합금

알루미늄 및 알루미늄 아연 합금

폴리머 및 유기 코팅

기타 코팅재

제조 공정

용융 아연 도금

전기 아연 도금

갈바니 링

알루미늄 도금 및 갈바륨 코팅

사전 도장 및 컬러 코팅

기타 코팅 기술

비교 분석 : 아연 도금 및 기타 코팅 철 제품

코팅 공정에서의 기술적 진보

트럼프 정권에 의한 관세에 대한 영향

무역에 미치는 영향

무역량의 혼란

보복 조치

업계에 미치는 영향

공급측의 영향(원재료)

주요 원재료의 가격 변동

공급망 재구성

생산 비용에 미치는 영향

수요측의 영향(판매가격)

최종 시장에의 가격 전달

시장 점유율 동향

소비자의 반응 패턴

영향을 받는 주요 기업

전략적인 업계 대응

공급망 재구성

가격 설정 및 제품 전략

정책관여

전망과 향후 검토 사항

무역 통계(HS코드)

주요 수출국(2021-2024년)

주요 수입국(2021-2024년)

요약

시장 개요 주요 조사 결과

시장 규모와 성장 예측

주요 시장 성장 촉진요인과 제약

경쟁 구도의 스냅샷

투자 기회와 전략적 제안

미래 전망과 시장의 가능성

세계의 아연 도금 강판 시장 개요

시장 정의와 범위

시장 규모와 성장 분석

시장 역학

시장 성장 촉진요인

내부식성 재료 수요 증가

건설 및 인프라 개발 확대

자동차 생산 증가와 경량화의 동향

신재생에너지 용도에서 채용 증가

시장 성장 억제요인

원재료 가격 변동

대체 재료의 경쟁

환경 문제와 규제상의 과제

시장 기회

신흥 시장 수요 증가

코팅 기술의 혁신

신재생에너지 인프라 확대

시장의 과제

엄격한 환경 규제

공급망의 혼란

변동하는 에너지 비용

COVID-19의 영향과 팬데믹 후의 회복

Porter's Five Forces 분석

PESTEL 분석

밸류체인 분석

원재료 공급자

제조업체

판매자와 소매업체

최종 사용자

제조·생산 분석

제조 공정 개요

원재료 조달 및 준비

파운데이션 철강 생산

표면 처리

코팅 도포 공정

코팅 후 처리

품질 관리 및 테스트

생산비용 분석

원재료비

에너지 비용

인건비

제조 간접비

비용 최적화 전략

제조시설 분석

주요 제조 거점

생산 능력 평가

시설 확장 계획

공급망의 과제와 해결책

제조 공정에서의 지속가능성

에너지 효율 대책

폐기물 삭감 전략

절수 대책

친환경 코팅 기술

규제 상황과 기준

세계의 규제 틀

지역 규제 틀

북미

ASTM 규격

건축 기준법과 규제

환경규제

유럽

EN 규격

CE 마킹 요건

환경규제

아시아태평양

JIS 규격(일본)

GB 규격(중국)

BIS 규격(인도)

세계의 기타 지역

제품 인증 및 규격

품질 기준

안전기준

환경 기준

컴플라이언스 과제와 전략

향후 규제 동향과 그 영향

환경·사회·거버넌스(ESG) 분석

환경 영향 평가

탄소 발자국 분석

수명 주기 평가(LCA)

에너지 소비와 배출량

폐기물 관리와 재활용

사회적 영향

노동 관행과 노동 조건

커뮤니티에 대한 영향과 관여

건강과 안전에 관한 고려 사항

거버넌스와 윤리적 배려

기업 지배 구조의 실천

윤리적인 공급망 관리

투명성과 보고

주요 기업의 ESG 성능 벤치마크

ESG 리스크 평가 및 경감 전략

아연 도금 및 코팅 철 업계에 있어서 향후 ESG 동향

소비자 행동과 시장 동향의 분석

소비자의 기호와 구매 패턴

구매결정에 영향을 미치는 요인

가격 감도

품질과 성능 요건

환경에의 배려

미적 선호

업계 고유의 취향

건설 업계의 취향

자동차 업계의 취향

가전 업계의 취향

소비자 행동의 지역차

디지털 변혁이 소비자 참여에 미치는 영향

미래의 소비자 동향과 그 영향

기술적 상황과 혁신 분석

아연 도금강·코팅 철의 현재의 기술 동향

신흥기술과 그 잠재적인 영향

고급 코팅 배합

나노기술의 응용

디지털 제조 및 인더스트리 4.0

코팅 공정에서의 자동화와 로봇 공학

연구개발활동과 혁신허브

용도 전체에 걸친 기술 채용 동향

기술 준비 상황 평가

향후 기술 로드맵(2025-2033년)

가격 분석과 경제적 요인

가격 동향 분석

역사적 가격 동향

현재 가격 시나리오

가격 예측

가격에 영향을 미치는 요인

원재료비

에너지 가격

인건비

수급 동향

무역정책과 관세

지역별 가격 차이

가격과 가치의 관계 분석

시장에 영향을 미치는 경제지표

GDP 성장과 건설 활동

공업생산지수

자동차 생산 동향

인프라 투자

주요 시장 기업의 가격 전략

지속가능성과 순환형 경제

지속 가능한 원재료 조달

생산에 있어서의 에너지 효율

폐기물 삭감과 리사이클의 대처

이산화탄소 배출량 저감 전략

아연 도금강 및 코팅 철의 순환형 경제 모델

제품 수명 연장 전략

종말기 관리

재활용과 업사이클의 기회

지속 가능한 실천 사례 연구

업계에서의 지속가능성의 미래

시장 기회와 전략적 제안

미개척 시장 기회

시장 진출기업에의 전략적 제안

제조업체용

투자자용

최종 사용자 산업용

신제품 개발의 기회

신규 참가자 시장 진출 전략

다양화의 기회

전략적 파트너십 및 협업 기회

투자분석과 시장의 매력

현재 투자 시나리오

부문별 투자 기회

지역별 투자 기회

ROI 분석

벤처 캐피탈과 프라이빗 에퀴티의 상황

M&A 활동 분석

미래 투자 전망

리스크 평가 및 경감 전략

시장 위험

기술적 위험

규제 위험

경쟁위험

공급망의 위험

환경과 지속가능성의 위험

리스크 경감 전략

미래 전망과 시장 발전

장기 시장 예측

새로운 용도과 이용 사례

기술 진화 시나리오

미래 시장 역학

잠재적인 파괴자와 게임 체인저

미래경쟁 구도

제4장 경쟁 구도

주요 기업의 시장 점유율 분석

경쟁 포지셔닝 매트릭스

채용하고 있는 경쟁 전략 : 주요 기업별

제품의 혁신과 개발

합병 및 인수

파트너십 및 협업

확대 전략

주요 기업의 SWOT 분석

주요 시장 기업의 상세한 기업 프로파일

ArcelorMittal

Nippon steel corporation

POSCO

Tata steel

Baowu steel group

JFE steel corporation

Nucor corporation

Thyssenkrupp

United States steel corporation

Cleveland-cliffs

Steel dynamics

Hyundai steel

Bluescope steel

Jindal steel & power

기타 주요 기업

아연 도금 및 코팅 철 및 강판 시장에 있어서의 신흥 기업과 스타트업 기업

특허 분석과 지적재산의 정세

최근 특허출원

특허소유권 분석

특허에 기초한 기술 동향 분석

제5장 시장 규모와 예측 : 코팅 유형별(2021-2034년)

주요 동향

용융 아연 도금 강철

전기 아연 도금 강철

갈바닐 처리 강철

갈바륨(아연 알루미늄 코팅) 강철

알루미늄 도금 강철

사전 도장 아연 도금 강철(PPGI)

기타

제6장 시장 규모와 예측 : 제품 형태별(2021-2034년)

주요 동향

코일

시트

플레이트

바 및 와이어

기타

제7장 시장 규모와 예측 : 도공량별(2021-2034년)

주요 동향

라이트 코팅(G30-G60)

미디엄 코팅(G90-G235)

헤비 코팅(G240 이상)

제8장 시장 규모와 예측 : 베이스강 등급별(2021-2034년)

주요 동향

상업용 강철

드로잉 스틸

구조용 강철

고강도 저합금강(HSLA)

고급 고강도 강철(AHSS)

기타

제9장 시장 규모와 예측 : 최종 용도 산업별(2021-2034년)

주요 동향

건설 및 인프라

주택건설

상업건설

산업건설

인프라 개발

자동차 및 운송

승용차

상용차

철도 및 지하철 시스템

조선

가전제품 및 전자기기

백색 가전

HVAC 시스템

전자 인클로저

에너지 및 전력

태양에너지 시스템

풍력에너지 인프라

전력 전송 및 분배

농업

산업기기 및 기계

기타

제10장 시장 규모와 예측 : 용도별(2021-2034년)

주요 동향

지붕재 및 외벽재

구조 부품

자동차 바디 부품

가전제품 케이스

전기 배관 및 인클로저

HVAC 덕트

기타

제11장 시장 규모와 예측 : 유통 채널별(2021-2034년)

주요 동향

직접 판매

유통업체 및 서비스 센터

소매점

전자상거래

기타

제12장 시장 규모와 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

기타 유럽

아시아태평양

중국

인도

일본

한국

호주

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

기타 중동 및 아프리카

제13장 기업 프로파일

ArcelorMittal

Nippon Steel Corporation

POSCO

Tata Steel

Baowu Steel

JFE Steel Corporation

Nucor Corporation

ThyssenKrupp

United States Steel

Cleveland-Cliffs

Steel Dynamics

Hyundai Steel

BlueScope Steel

Jindal Steel &Power

KTH

영문 목차

영문목차

The Global Galvanized And Coated Iron and Steel Sheets Market was valued at USD 162.8 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 259.1 billion by 2034, shaped by the surge in demand from industries such as automotive, construction, and consumer goods. Rapid urbanization and industrial expansion in developed and emerging economies help boost demand for durable and corrosion-resistant steel materials. These sheets offer longevity, structural integrity, and cost-effectiveness, essential in heavy-duty and long-term applications.

Additionally, the development of advanced surface treatments that enhance corrosion resistance, durability, and aesthetic appeal is expanding the application range of galvanized and coated iron and steel sheets. Manufacturers incorporate eco-friendly coating formulations that reduce toxic emissions and energy consumption during production. This aligns with growing regulatory pressures and customer demand for greener building and manufacturing materials. As a result, these innovations not only improve performance but also support compliance with sustainability standards, making them more appealing for use in construction, automotive, and industrial applications globally.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$162.8 Billion

Forecast Value

$259.1 Billion

CAGR

4.6%

Within the market, hot-dip galvanized steel continues to be the most widely used coating technique. This segment generated USD 95.7 billion in 2024 and is projected to reach USD 147.9 billion by 2034. Its dominance stems from superior durability, long-term corrosion protection, and affordability. The hot-dip process creates a zinc-steel bond that acts as a shield in aggressive environments, making it an ideal material for high-impact use in agriculture, infrastructure, transportation, and industrial projects.

Galvanized and coated steel in coil form remains a popular choice among large-scale users due to its ease of transportation and reduced inventory costs. In 2024, the coils segment accounted for a 39.9% share. Coils can be processed into specific dimensions on-site, minimizing waste and optimizing material usage. These characteristics make them ideal for streamlined operations in automotive production lines, modular housing projects, and prefabricated structures. Additionally, galvanized coils are seeing heightened demand as key raw materials in painted and aesthetic-grade building components, aligning with growing interest in green and energy-efficient construction.

United States Galvanized And Coated Iron and Steel Sheets Market stood at USD 17.4 billion in 2024 and is expected to register a CAGR of 4.9% through 2034. Robust demand is driven by the country's expanding automotive and infrastructure sectors, where corrosion resistance and extended material lifespan are critical requirements. Projects in bridges, commercial buildings, and transport networks continue to adopt these steel products due to their resilience and performance in various environments.

Key players in this market include POSCO, ArcelorMittal, Baowu Steel Group, TATA Steel, and Nippon Steel Corporation. These companies are strengthening their competitive edge by investing in advanced galvanizing technology, expanding production capacities, and forming strategic partnerships with end-use industries. A strong emphasis is placed on environmentally responsible methods and automation in manufacturing to reduce costs and support long-term scalability.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Report scope and objectives

1.2 Research design and approach

1.3 Data collection methods

1.3.1 Primary research

1.3.2 Secondary research

1.4 Market estimation and forecasting methodology

1.5 Assumptions and limitations

1.6 Data validation and triangulation techniques

Chapter 2 Executive Summary

2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

3.1 Galvanized and coated steel: fundamentals and evolution

3.1.1 Definition and classification of galvanized and coated steel products

3.1.2 Historical development of coating technologies

3.1.3 Raw materials and composition

3.1.3.1 Base steel types and properties

3.1.3.2 Zinc and zinc alloys

3.1.3.3 Aluminum and aluminum-zinc alloys

3.1.3.4 Polymers and organic coatings

3.1.3.5 Other coating materials

3.1.4 Manufacturing processes

3.1.4.1 Hot-dip galvanizing

3.1.4.2 Electro galvanizing

3.1.4.3 Galvannealing

3.1.4.4 Aluminizing and galvalume coating

3.1.4.5 Pre-painting and color coating

3.1.4.6 Other coating technologies

3.1.5 Comparative analysis: galvanized vs. Other coated steel products

3.1.6 Technological advancements in coating processes

3.2 Trump administration tariffs

3.2.1 Impact on trade

3.2.1.1 Trade volume disruptions

3.2.1.2 Retaliatory measures

3.2.2 Impact on the industry

3.2.2.1 Supply-side impact (raw materials)

3.2.2.1.1 Price volatility in key materials

3.2.2.1.2 Supply chain restructuring

3.2.2.1.3 Production cost implications

3.2.2.2 Demand-side impact (selling price)

3.2.2.2.1 Price transmission to end markets

3.2.2.2.2 Market share dynamics

3.2.2.2.3 Consumer response patterns

3.2.3 Key companies impacted

3.2.4 Strategic industry responses

3.2.4.1 Supply chain reconfiguration

3.2.4.2 Pricing and product strategies

3.2.4.3 Policy engagement

3.2.5 Outlook and future considerations

3.3 Trade statistics (HS Code)

3.3.1 Major exporting countries, 2021-2024 (USD Mn)

3.3.2 Major importing countries, 2021-2024 (USD Mn)

3.4 Summary

3.4.1 Market overview and key findings

3.4.2 Market size and growth projections

3.4.3 Key market drivers and restraints

3.4.4 Competitive landscape snapshot

3.4.5 Investment opportunities and strategic recommendations

3.4.6 Future outlook and market potential

3.5 Global galvanized and coated steel market overview

3.5.1 Market definition and scope

3.5.2 Market size and growth analysis

3.5.3 Market dynamics

3.5.3.1 Market drivers

3.5.3.1.1 Growing demand for corrosion-resistant materials

3.5.3.1.2 Expansion in construction and infrastructure development

3.5.3.1.3 Rising automotive production and lightweight trends

3.5.3.1.4 Increasing adoption in renewable energy applications

3.5.3.2 Market restraints

3.5.3.2.1 Volatility in raw material prices

3.5.3.2.2 Competition of alternative materials

3.5.3.2.3 Environmental concerns and regulatory challenges

3.5.3.3 Market opportunities

3.5.3.3.1 Growing demand in emerging markets

3.5.3.3.2 Innovations in coating technologies

3.5.3.3.3 Expansion in renewable energy infrastructure

3.5.3.4 Market challenges

3.5.3.4.1 Stringent Environmental Regulations

3.5.3.4.2 Supply chain disruptions

3.5.3.4.3 Fluctuating energy costs

3.5.4 Impact of covid-19 and post-pandemic recovery

3.5.5 Porter's five forces analysis

3.5.6 Pestle analysis

3.5.7 Value chain analysis

3.5.7.1 Raw material suppliers

3.5.7.2 Manufacturers

3.5.7.3 Distributors and retailers

3.5.7.4 End users

3.6 Manufacturing and production analysis

3.6.1 Manufacturing process overview

3.6.1.1 Raw material procurement and preparation

3.6.1.2 Base steel production

3.6.1.3 Surface preparation

3.6.1.4 Coating application processes

3.6.1.5 Post-coating treatments

3.6.1.6 Quality control and testing

3.6.2 Production cost analysis

3.6.2.1 Raw material costs

3.6.2.2 Energy costs

3.6.2.3 Labor costs

3.6.2.4 Manufacturing overheads

3.6.2.5 Cost optimization strategies

3.6.3 Manufacturing facilities analysis

3.6.3.1 Key manufacturing locations

3.6.3.2 Production capacity assessment

3.6.3.3 Facility expansion plans

3.6.4 Supply chain challenges and solutions

3.6.5 Sustainability in manufacturing processes

3.6.5.1 Energy efficiency measures

3.6.5.2 Waste reduction strategies

3.6.5.3 Water conservation practices

3.6.5.4 Eco-friendly coating technologies

3.7 Regulatory landscape and standards

3.7.1 Global regulatory framework

3.7.2 Regional regulatory frameworks

3.7.2.1 North America

3.7.2.1.1 ASTM standards

3.7.2.1.2 Building codes and regulations

3.7.2.1.3 Environmental regulations

3.7.2.2 Europe

3.7.2.2.1 EN standards

3.7.2.2.2 CE marking requirements

3.7.2.2.3 Environmental regulations

3.7.2.3 Asia-pacific

3.7.2.3.1 JIS standards (Japan)

3.7.2.3.2 GB standards (China)

3.7.2.3.3 BIS standards (India)

3.7.2.4 Rest of the world

3.7.3 Product certification and standards

3.7.3.1 Quality standards

3.7.3.2 Safety standards

3.7.3.3 Environmental standards

3.7.4 Compliance challenges and strategies

3.7.5 Future regulatory trends and their implications

3.8 Environmental, social, and governance (ESG) analysis

3.8.1 Environmental impact assessment

3.8.1.1 Carbon footprint analysis

3.8.1.2 Life cycle assessment (LCA)

3.8.1.3 Energy consumption and emissions

3.8.1.4 Waste management and recycling

3.8.2 Social implications

3.8.2.1 Labor practices and working conditions

3.8.2.2 Community impact and engagement

3.8.2.3 Health and safety considerations

3.8.3 Governance and ethical considerations

3.8.3.1 Corporate governance practices

3.8.3.2 Ethical supply chain management

3.8.3.3 Transparency and reporting

3.8.4 ESG performance benchmarking of key players

3.8.5 ESG risk assessment and mitigation strategies

3.8.6 Future ESG trends in the galvanized and coated steel industry

3.9 Consumer behavior and market trends analysis

3.9.1 Consumer preferences and purchasing patterns

3.9.2 Factors influencing purchase decisions

3.9.2.1 Price sensitivity

3.9.2.2 Quality and performance requirements

3.9.2.3 Environmental considerations

3.9.2.4 Aesthetic preferences

3.9.3 Industry-specific preferences

3.9.3.1 Construction industry preferences

3.9.3.2 Automotive industry preferences

3.9.3.3 Appliance industry preferences

3.9.4 Regional variations in consumer behavior

3.9.5 Impact of digital transformation on consumer engagement

3.9.6 Future consumer trends and their implications

3.10 Technological landscape and innovation analysis

3.10.1 Current technological trends in galvanized and coated steel

3.10.2 Emerging technologies and their potential impact

3.10.2.1 Advanced coating formulations

3.10.2.2 Nanotechnology applications

3.10.2.3 Digital manufacturing and industry 4.0

3.10.2.4 Automation and robotics in coating processes

3.10.3 R&D activities and innovation hubs

3.10.4 Technology adoption trends across applications

3.10.5 Technology readiness assessment

3.10.6 Future technology roadmap 2025–2033

3.11 Pricing analysis and economic factors

3.11.1 Pricing trends analysis

3.11.1.1 Historical price trends

3.11.1.2 Current pricing scenario

3.11.1.3 Price forecast

3.11.2 Factors affecting pricing

3.11.2.1 Raw material costs

3.11.2.2 Energy prices

3.11.2.3 Labor costs

3.11.2.4 Supply-demand dynamics

3.11.2.5 Trade policies and tariffs

3.11.3 Regional price variations

3.11.4 Price-value relationship analysis

3.11.5 Economic indicators impacting the market

3.11.5.1 GDP growth and construction activity

3.11.5.2 Industrial production index

3.11.5.3 Automotive production trends

3.11.5.4 Infrastructure investment

3.11.6 Pricing strategies for key market players

3.12 Sustainability and circular economy

3.12.1 Sustainable sourcing of raw materials

3.12.2 Energy efficiency in production

3.12.3 Waste reduction and recycling initiatives

3.12.4 Carbon footprint reduction strategies

3.12.5 Circular economy models in galvanized and coated steel

3.12.5.1 Product life extension strategies

3.12.5.2 End-of-life management

3.12.5.3 Recycling and upcycling opportunities

3.12.6 Case studies of sustainable practices

3.12.7 Future of sustainability in the industry

3.13 Market opportunities and strategic recommendations

3.13.1 Untapped market opportunities

3.13.2 Strategic recommendations for market participants

3.13.2.1 For manufacturers

3.13.2.2 For investors

3.13.2.3 For end-user industries

3.13.3 New product development opportunities

3.13.4 Market entry strategies for new players

3.13.5 Diversification opportunities

3.13.6 Strategic partnerships and collaboration opportunities

3.14 Investment analysis and market attractiveness

3.14.1 Current investment scenario

3.14.2 Investment opportunities by segment

3.14.3 Investment opportunities by region

3.14.4 Roi analysis

3.14.5 Venture capital and private equity landscape

3.14.6 M&A activity analysis

3.14.7 Future investment outlook

3.15 Risk assessment and mitigation strategies

3.15.1 Market risks

3.15.2 Technological risks

3.15.3 Regulatory risks

3.15.4 Competitive risks

3.15.5 Supply chain risks

3.15.6 Environmental and sustainability risks

3.15.7 Risk mitigation strategies

3.16 Future outlook and market evolution

3.16.1 Long-term market forecast

3.16.2 Emerging applications and use cases

3.16.3 Technological evolution scenarios

3.16.4 Future market dynamics

3.16.5 Potential disruptors and game-changers

3.16.6 Future competitive landscape

Chapter 4 Competitive Landscape, 2024

4.1 Market share analysis of key players

4.2 Competitive positioning matrix

4.3 Competitive strategies adopted by key players

4.3.1 Product innovation and development

4.3.2 Mergers and acquisitions

4.3.3 Partnerships and collaborations

4.3.4 Expansion strategies

4.4 Swot analysis of key players

4.5 Detailed company profiles of major market players

4.5.1 ArcelorMittal

4.5.2 Nippon steel corporation

4.5.3 POSCO

4.5.4 Tata steel

4.5.5 Baowu steel group

4.5.6 JFE steel corporation

4.5.7 Nucor corporation

4.5.8 Thyssenkrupp

4.5.9 United States steel corporation

4.5.10 Cleveland-cliffs

4.5.11 Steel dynamics

4.5.12 Hyundai steel

4.5.13 Bluescope steel

4.5.14 Jindal steel & power

4.5.15 Other notable players

4.6 Emerging players and startups in galvanized and coated steel market

4.7 Patent analysis and intellectual property landscape

4.7.1 Recent patent filings

4.7.2 Patent ownership analysis

4.7.3 Technology trend analysis based on patents

Chapter 5 Market Size and Forecast, By Coating Type, 2021-2034 (USD Million) (Tons)

5.1 Key trends

5.2 Hot-dip galvanized steel

5.3 Electrogalvanized steel

5.4 Galvannealed steel

5.5 Galvalume (zinc-aluminum coated) steel

5.6 Aluminized steel

5.7 Pre-painted galvanized steel (PPGI)

5.8 Other

Chapter 6 Market Size and Forecast, By Product Form, 2021-2034 (USD Million) (Tons)

6.1 Key trends

6.2 Coils

6.3 Sheets

6.4 Plates

6.5 Bars and wires

6.6 Others

Chapter 7 Market Size and Forecast, By Coating Weight, 2021-2034 (USD Million) (Tons)

7.1 Key trends

7.2 Light coating (G30–G60)

7.3 Medium coating (G90–G235)

7.4 Heavy coating (G240 and above)

Chapter 8 Market Size and Forecast, By Base Steel Grade, 2021-2034 (USD Million) (Tons)

8.1 Key trends

8.2 Commercial steel

8.3 Drawing steel

8.4 Structural steel

8.5 High-strength low-alloy steel (HSLA)

8.6 Advanced high-strength steel (AHSS)

8.7 Others

Chapter 9 Market Size and Forecast, By End Use Industry, 2021-2034 (USD Million) (Tons)

9.1 Key trends

9.2 Construction and infrastructure

9.2.1 Residential construction

9.2.2 Commercial construction

9.2.3 Industrial construction

9.2.4 Infrastructure development

9.3 Automotive and transportation

9.3.1 Passenger vehicles

9.3.2 Commercial vehicles

9.3.3 Railway and metro systems

9.3.4 Shipbuilding

9.4 Home appliances and electronics

9.4.1 White goods

9.4.2 HVAC systems

9.4.3 Electronic enclosures

9.5 Energy and power

9.5.1 Solar energy systems

9.5.2 Wind energy infrastructure

9.5.3 Power transmission and distribution

9.6 Agriculture

9.7 Industrial equipment and machinery

9.8 Others

Chapter 10 Market Size and Forecast, By Specific Applications, 2021-2034 (USD Million) (Tons)

10.1 Key trends

10.2 Roofing and cladding

10.3 Structural components

10.4 Automotive body parts

10.5 Appliance casings

10.6 Electrical conduits and enclosures

10.7 HVAC ductwork

10.8 Others

Chapter 11 Market Size and Forecast, By Distribution Channel, 2021-2034 (USD Million) (Tons)

11.1 Key trends

11.2 Direct sales

11.3 Distributors and service centers

11.4 Retail outlets

11.5 E-commerce

11.6 Others

Chapter 12 Market Size and Forecast, By Region, 2021-2034 (USD Million) (Tons)