셀룰로오스 나노결정 및 나노섬유 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

Cellulose Nanocrystals and Nanofibers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1750488

리서치사:Global Market Insights Inc.

발행일:2025년 05월

페이지 정보:영문 235 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

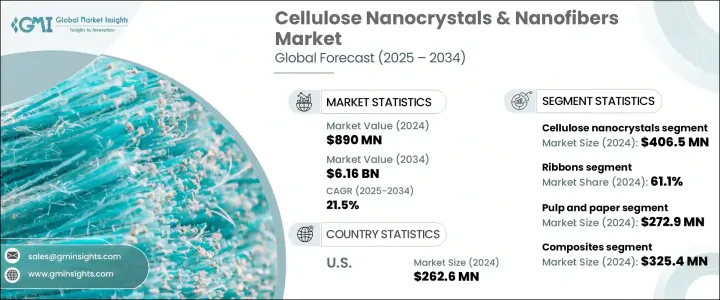

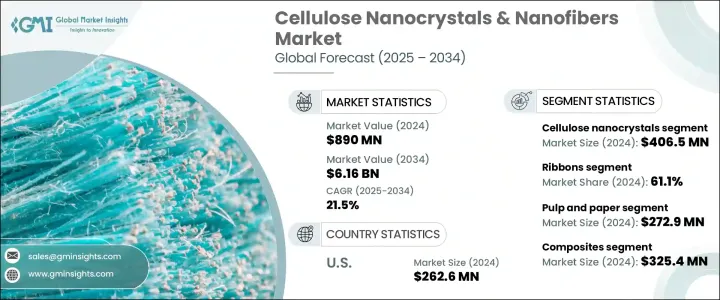

세계의 셀룰로오스 나노결정 및 나노섬유 시장은 2024년에는 8억 9,000만 달러로 평가되었고, 2034년에는 61억 6,000만 달러에 이를것으로 예측되며, CAGR 21.5%로 성장할 것으로 추정됩니다.

목재 펄프와 농업 잔여물에서 추출된 나노셀룰로스는 탄소 배출량을 줄이고 환경 친화적 실천을 채택하려는 다양한 산업에서 매력적인 선택지로 부상하고 있습니다. 이 식물 기반 나노재료는 환경적 이점뿐 아니라 복합재료, 전자기기, 의료기기, 친환경 포장재 등 신흥 응용 분야의 성능 요구사항을 충족시키는 우수한 기능을 제공합니다.

재료 과학 분야의 지속적인 발전은 셀룰로오스 나노재료의 성능을 새로운 영역으로 확장시키고 있습니다. 높은 인장 강도, 강성, 낮은 열팽창률과 함께 오일 및 산소 저항성과 같은 우수한 차단 특성은 엄격한 사용 조건에 적합합니다. 또한 산업계는 항균성, 내열성, 전도성까지 통합한 다기능 제형으로 눈을 돌리고 있습니다. 이러한 진화하는 기능은 항공우주, 건설, 전자, 생명 과학 등 다양한 분야에서 상용화가 확대되고 있습니다. 지속 가능한 대안에 대한 규제 모멘텀과 대중의 압력이 계속 확대되면서 이 분야의 혁신이 널리 촉진되고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작금액

8억 9,000만 달러

예측 금액

61억 6,000만 달러

CAGR

21.5%

셀룰로오스 나노결정 부문은 2024년에 4억 650만 달러의 매출을 올렸으며, 2034년까지 연평균 22.1%의 성장률을 보일 것으로 예상됩니다. 산 가수분해를 통해 얻은 고결정성 구조는 뛰어난 보강 능력을 제공합니다. 이러한 특성으로 인해 CNCs는 고급 코팅, 필름, 구조용 복합재에 이상적입니다. 반면, 기계적 또는 효소적 과정을 통해 생산된 셀룰로오스 나노섬유는 유연성을 갖추고 포장, 필터링, 개인 위생 제품에 적합합니다. 그들의 네트워크 형성 구조는 내구성을 유지하면서 생분해성을 유지해 친환경 성능을 중시하는 최종 사용 시장에서의 가치를 높입니다.

펄프 및 제지 부문은 2024년에 2억 7,290만 달러의 시장 규모를 차지했으며, 연평균 22.4%의 성장률을 보일 것으로 예상됩니다. 이 부문은 경량, 강도 및 퇴비화 특성으로 인해 나노셀룰로오스를 계속해서 활용하고 있습니다. 지속 가능한 포장에의 적용은 소비재 및 산업 부문에서 생분해성 대체재에 대한 수요 증가와 부합합니다. 기업들은 플라스틱 의존도를 줄이면서 내구성과 성능을 유지하기 위해 종이 코팅, 차단층, 성형 포장 솔루션에 셀룰로오스 나노 소재를 점점 더 많이 채택하고 있습니다. 단일 사용 플라스틱에 대한 규제가 강화됨에 따라 식품, 음료, 소매 산업에서 라벨링, 포장재, 용기 등에 나노셀룰로오스 기반 대체재에 대한 수요가 지속적으로 증가하고 있습니다.

미국의 셀룰로오스 나노결정 및 나노섬유 시장은 2024년에 2억 6,260만 달러로 평가되었으며, 2034년까지 연평균 20.9%의 성장률을 보일 것으로 예상됩니다. 이러한 성장은 혁신 허브, 연구 협력, 전자, 의료 및 지속 가능한 포장 분야의 응용으로 뒷받침됩니다. 강력한 연방 연구 자금 지원, 대학과 민간 기업 간의 전략적 파트너십, 순환 경제 모델로의 전환이 개발을 촉진하고 있습니다. 기술 상업화 위한 탄탄한 생태계를 갖춘 미국 시장은 의료 기기, 스마트 포장, 유연 전자 기판 분야에서 조기 채택을 통해 글로벌 나노셀룰로오스 혁신 분야에서 선도적 위치를 유지하고 있습니다.

Sappi Limited, Nippon Paper Industries Co., Ltd., Borregaard ASA, CelluForce Inc. 및 American Process Inc.와 같은 주요 기업들은 R&D 시설을 확장하고, 확장 가능한 생산 공정을 개발하며, 최종 사용 산업 전반에 걸쳐 전략적 파트너십을 구축하여 시장 지위를 강화하고 있습니다. 이러한 기업들은 글로벌 시장의 진화하는 요구를 충족하고 비용 효율적인 상용화를 촉진하기 위해 차세대 제형 및 대량 생산에 투자하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

시장 정의와 진화

트럼프 정권의 관세 영향 - 구조화된 개요

무역에 미치는 영향

무역량의 혼란

보복 조치

업계에 미치는 영향

공급측의 영향(원자재)

주요 원자재의 가격 변동

공급망 재구성

생산 비용에 미치는 영향

수요측의 영향(판매가격)

최종 시장에의 가격 전달

시장 점유율 동향

소비자의 반응 패턴

영향을 받는 주요 기업

전략적인 업계 대응

공급망 재구성

가격 설정 및 제품 전략

정책관여

전망과 향후 검토 사항

무역 통계(HS 코드) 참고 : 위의 무역 통계는 주요 국가에 대해서만 제공됩니다

주요 수출국

국가 1

국가 2

국가 3

주요 수입국

국가 1

국가 2

국가 3

업계 밸류체인 분석

원자재의 정세와 공급망의 동향

원료 분석

지속 가능한 조달 관행

공급망의 과제와 해결책

가격 분석과 비용 구조

생산비용 분석

가격 동향

비용 절감 전략

기술의 상황

추출 및 생산 기술

기계적 방법

화학적 방법

효소법

복합적인 접근

특성 평가 기술

기술의 진보와 혁신

시장 역학

시장 성장 촉진요인

지속 가능한 재료에 대한 수요 증가가

우수한 기계적 및 차단 특성

R&D 투자 증가

바이오 기반 재료를 우대하는 정부 규제

시장 성장 억제요인

높은 생산 비용

확장성의 과제

가공 기술의 한계

전통적 재료와의 경쟁

시장 기회

의료 및 전자 분야에서의 신규 응용 분야

표면 개질 기술의 발전

다른 나노 재료와의 통합

미개척 지역 시장

시장의 과제

표준화 문제

분산 및 호환성 과제

습기에 대한 민감성

규제상의 장애물

규제 프레임워크과 기준

지역의 규제 상황

인증 및 품질 기준

환경규제의 영향

혁신과 지속가능성의 대처

순환형 경제의 통합

이산화탄소 배출량 저감 전략

폐기물 재활용 접근 방식

PESTEL 분석

Porter's Five Forces 분석

지속가능성과 ESG 분석

제4장 경쟁 구도

시장 점유율 분석

주요 이해관계자와 전략적 포지셔닝

기업의 시장 포지셔닝 및 히트맵 분석

경쟁 전략과 전략적 노력

합병, 인수, 제휴

신제품 출시와 혁신

투자 및 자금조달 시나리오

스타트업 생태계 분석

특허 분석과 지적재산의 정세

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

주요 동향

셀룰로오스 나노결정(CNC)

황산화 CNC

카르복실화 CNC

인산화 CNC

기타 CNC

셀룰로오스 나노섬유(CNF)

기계적 섬유화 CNF

TEMPO 산화 CNF

효소 처리 CNF

기타 CNF

박테리아 나노셀룰로오스(BNC)

셀룰로오스 나노피브릴(CNF)

기타 나노셀룰로오스 제품

제6장 시장 추계 및 예측 : 소스별(2021-2034년)

주요 동향

목재

연목

경목

비목재 식물원

농업 잔류물

코튼

대마

아마

기타

세균 합성

조류 밑 해면동물

재활용 자원

종이 폐기물

섬유 폐기물

기타 재활용 자원

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

복합재료

폴리머 매트릭스 복합재료

시멘트 복합재

기타 복합재료

종이 및 포장

종이 강화

배리어 필름

식품 포장

기타 포장 용도

코팅 및 필름

광학 필름

배리어 코팅

항균 코팅

기타 코팅

바이오메디컬 및 제약

약물전달 시스템

상처 치유 재료

조직 공학용 지지체

기타 생물의학적 응용

전자기기 및 센서

플렉서블 전자기기

생체 센서

에너지 저장 장치

기타 전자 용도

레올로지 개질제

석유 및 가스

페인트 및 코팅

퍼스널케어 제품

기타 레올로지 응용

여과 및 분리

에어로젤 및 폼

기타 용도

제8장 시장 추계 및 예측 : 최종 이용 산업별(2021-2034년)

주요 동향

펄프 및 제지

패키지

식품 및 음료

의료 및 의약품

전자와 광전자

자동차 및 수송

건설자재

섬유 및 의류

퍼스널케어 및 화장품

석유 및 가스

도료, 코팅제, 접착제

기타

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제10장 기업 프로파일

Celluforce

American Process Inc.

Borregaard

Nippon Paper Industries Co.,Ltd.

Stora Enso

UPM-Kymmene Oyj

Sappi Limited

Kruger Inc.

Daicel Corporation

Weidmann Fiber Technology

Melodea Ltd.

Blue Goose Biorefineries Inc.

Oji Holdings Corporation

VTT Technical Research Centre of Finland

FPInnovations

Cellucomp Ltd.

Forest Products Laboratory(FPL)

Nanografi Nano Technology

Asahi Kasei Corpo

HBR

영문 목차

영문목차

The Global Cellulose Nanocrystals and Nanofibers Market was valued at USD 890 million in 2024 and is estimated to grow at a CAGR of 21.5% to reach USD 6.16 billion by 2034, driven by increasing industry demand for renewable, biodegradable materials that serve as sustainable alternatives to petroleum-based products. Nanocellulose, derived from wood pulp and agricultural residues, is becoming an attractive choice for multiple industries aiming to reduce their carbon footprint and adopt eco-conscious practices. These plant-based nanomaterials not only offer environmental benefits but also deliver superior functionality that supports the performance needs of emerging applications in composites, electronics, medical devices, and green packaging.

Ongoing advances in material science have pushed the capabilities of cellulose nanomaterials into new territories. Their high tensile strength, stiffness, and low thermal expansion, combined with impressive barrier properties-such as oil and oxygen resistance-make them suitable for demanding use cases. Industries are also turning to multifunctional formulations, where the material integrates antimicrobial protection, heat resistance, and even conductivity. These evolving features lead to broader commercial adoption across sectors like aerospace, construction, electronics, and life sciences. Supportive regulatory momentum and growing public pressure for sustainable alternatives continue to drive widespread innovation in this space.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$890 Million

Forecast Value

$6.16 Billion

CAGR

21.5%

Cellulose nanocrystals segment generated USD 406.5 million in 2024 and is expected to witness a CAGR of 22.1% through 2034. Their highly crystalline structure, obtained through acid hydrolysis, provides excellent reinforcement capabilities. These properties make CNCs ideal for advanced coatings, films, and structural composites. On the other hand, cellulose nanofibers-produced through mechanical or enzymatic processes-offer flexibility and are well-suited for packaging, filtration, and personal care products. Their network-forming structure supports durability while maintaining biodegradability, adding value in end-use markets focused on eco-friendly performance.

The pulp and paper segment accounted for USD 272.9 million of the market in 2024 and is projected to grow at a CAGR of 22.4%. This segment continues to leverage nanocellulose for its lightweight, strong, and compostable nature. Its application in sustainable packaging aligns with the rising demand for biodegradable alternatives across consumer and industrial sectors. Companies are increasingly adopting cellulose nanomaterials in paper coatings, barrier layers, and molded packaging solutions to reduce reliance on plastics while maintaining durability and performance. As regulations tighten around single-use plastics, demand for nanocellulose-based alternatives in labeling, wrapping, and containers continues to rise across food, beverage, and retail industries.

United States Cellulose Nanocrystals and Nanofibers Market was valued at USD 262.6 million in 2024 and is projected to grow at a 20.9% CAGR through 2034. This growth is supported by innovation hubs, research collaborations, and applications in electronics, healthcare, and sustainable packaging. Strong federal research funding, strategic partnerships between universities and private firms, and a shift toward circular economy models fuel development. With a robust ecosystem for technology commercialization, the U.S. market benefits from early adoption across medical devices, smart packaging, and flexible electronic substrates, helping it maintain a leading position globally in nanocellulose innovation.

Key companies such as Sappi Limited, Nippon Paper Industries Co., Ltd., Borregaard ASA, CelluForce Inc., and American Process Inc. are strengthening their market position by expanding R&D facilities, developing scalable production processes, and forming strategic partnerships across end-use industries. These players are investing in next-gen formulations and high-volume production to meet the evolving needs of global markets and drive cost-effective commercialization.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope & definition

1.2 Base estimates & calculations

1.3 Forecast calculation

1.4 Data sources

1.4.1 Primary

1.4.2 Secondary

1.4.2.1 Paid sources

1.4.2.2 Public sources

1.5 Primary research and validation

1.5.1 Primary sources

1.5.2 Data mining sources

Chapter 2 Executive Summary

2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

3.1 Market definition and evolution

3.2 Impact of trump administration tariffs – structured overview

3.2.1 Impact on trade

3.2.1.1 Trade volume disruptions

3.2.1.2 Retaliatory measures

3.2.2 Impact on the industry

3.2.2.1 Supply-side impact (raw materials)

3.2.2.2 Price volatility in key materials

3.2.2.3 Supply chain restructuring

3.2.2.4 Production cost implications

3.2.2.2 Demand-side impact (selling price)

3.2.2.1 Price transmission to end markets

3.2.2.2 Market share dynamics

3.2.2.3 Consumer response patterns

3.2.3 Key companies impacted

3.2.4 Strategic industry responses

3.2.4.1 Supply chain reconfiguration

3.2.4.2 Pricing and product strategies

3.2.4.3 Policy engagement

3.2.5 Outlook and future considerations

3.3 Trade statistics (HS code) Note: the above trade statistics will be provided for key countries only.

3.3.1 Major exporting countries

3.3.1.1 Country 1

3.3.1.2 Country 2

3.3.1.3 Country 3

3.3.2 Major importing countries

3.3.2.1 Country 1

3.3.2.2 Country 2

3.3.2.3 Country 3

3.4 Industry value chain analysis

3.5 Raw material landscape and supply chain dynamics

3.5.1 Feedstock analysis

3.5.2 Sustainable sourcing practices

3.5.3 Supply chain challenges and solutions

3.6 Pricing analysis and cost structure

3.6.1 Production cost analysis

3.6.2 Pricing trends

3.6.3 Cost reduction strategies

3.7 Technology landscape

3.7.1 Extraction and production technologies

3.7.1.1 Mechanical methods

3.7.1.2 Chemical methods

3.7.1.3 Enzymatic methods

3.7.1.4 Combined approaches

3.7.2 Characterization techniques

3.7.3 Technological advancements and innovations

3.8 Market dynamics

3.8.1 Market drivers

3.8.1.1 Growing demand for sustainable materials

3.8.1.2 Superior mechanical and barrier properties

3.8.1.3 Increasing R&D investments

3.8.1.4 Government regulations favoring bio-based materials

3.8.2 Market restraints

3.8.2.1 High production costs

3.8.2.2 Scalability challenges

3.8.2.3 Technical limitations in processing

3.8.2.4 Competition from conventional materials

3.8.3 Market opportunities

3.8.3.1 Emerging applications in healthcare and electronics

3.8.3.2 Advancements in surface modification techniques

3.8.3.3 Integration with other nanomaterials

3.8.3.4 Untapped regional markets

3.8.4 Market challenges

3.8.4.1 Standardization issues

3.8.4.2 Dispersion and compatibility challenges

3.8.4.3 Moisture sensitivity

3.8.4.4 Regulatory hurdles

3.9 Regulatory framework and standards

3.9.1 Regional regulatory landscape

3.9.2 Certification and quality standards

3.9.3 Environmental regulations impact

3.10 Innovation and sustainability initiatives

3.10.1 Circular economy integration

3.10.2 Carbon footprint reduction strategies

3.10.3 Waste valorization approaches

3.11 PESTEL analysis

3.12 Porter's five forces analysis

3.13 Sustainability and ESG analysis

Chapter 4 Competitive Landscape, 2024

4.1 Market share analysis, 2024

4.2 Key stakeholders and strategic positioning

4.3 Company market positioning and heat map analysis

4.4 Competitive strategies and strategic initiatives

4.5 Mergers, acquisitions, and collaborations

4.6 New product launches and innovations

4.7 Investment and funding scenario

4.8 Start-up ecosystem analysis

4.9 Patent analysis and intellectual property landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million) (Kilo Tons)

5.1 Key trends

5.2 Cellulose nanocrystals (CNCs)

5.2.1 Sulfated CNCs

5.2.2 Carboxylated CNCs

5.2.3 Phosphorylated CNCs

5.2.4 Other Modified CNCs

5.3 Cellulose nanofibers (CNFs)

5.3.1 Mechanically fibrillated CNFs

5.3.2 TEMPO-oxidized CNFs

5.3.3 Enzymatically pretreated CNFs

5.3.4 Other modified CNFs

5.4 Bacterial nanocellulose (BNC)

5.5 Cellulose nanofibrils (CNF)

5.6 Other nanocellulose products

Chapter 6 Market Estimates and Forecast, By Source, 2021 - 2034 (USD Million) (Kilo Tons)

6.1 Key trends

6.2 Wood

6.2.1 Softwood

6.2.2 Hardwood

6.3 Non-wood plant sources

6.3.1 Agricultural residues

6.3.2 Cotton

6.3.3 Hemp

6.3.4 Flax

6.3.5 Other plant sources

6.4 Bacterial synthesis

6.5 Algae and tunicates

6.6 Recycled sources

6.6.1 Paper waste

6.6.2 Textile waste

6.6.3 Other recycled sources

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

7.1 Key trends

7.2 Composites

7.2.1 Polymer matrix composites

7.2.2 Cement composites

7.2.3 Other composites

7.3 Paper and packaging

7.3.1 Paper strengthening

7.3.2 Barrier films

7.3.3 Food packaging

7.3.4 Other packaging applications

7.4 Coatings and films

7.4.1 Optical films

7.4.2 Barrier coatings

7.4.3 Antimicrobial coatings

7.4.4 Other coatings

7.5 Biomedical and pharmaceutical

7.5.1 Drug delivery systems

7.5.2 Wound healing materials

7.5.3 Tissue engineering scaffolds

7.5.4 Other biomedical applications

7.6 Electronics and sensors

7.6.1 Flexible electronics

7.6.2 Biosensors

7.6.3 Energy storage devices

7.6.4 Other electronic applications

7.7 Rheology modifiers

7.7.1 Oil and gas applications

7.7.2 Paints and coatings

7.7.3 Personal care products

7.7.4 Other rheological applications

7.8 Filtration and separation

7.9 Aerogels and foams

7.10 Other applications

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Million) (Kilo Tons)

8.1 Key trends

8.2 Pulp and paper

8.3 Packaging

8.4 Food and beverage

8.5 Healthcare and pharmaceuticals

8.6 Electronics and optoelectronics

8.7 Automotive and transportation

8.8 Construction and building materials

8.9 Textiles and apparel

8.10 Personal care and cosmetics

8.11 Oil and gas

8.12 Paints, coatings, and adhesives

8.13 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)