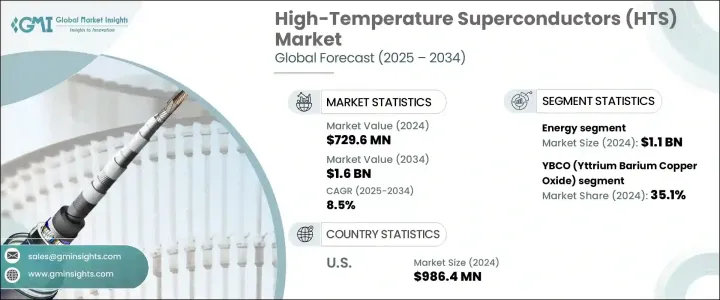

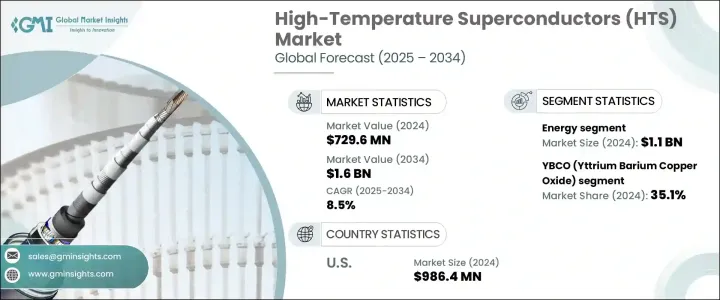

세계의 고온 초전도체 시장은 2024년에 7억 2,960만 달러로 평가되었고 2034년에는 16억 달러에 이를 것으로 예측되며, CAGR 8.5%로 성장할 전망입니다.

고온 초전도체(HTS)는 전통적인 초전도체보다 훨씬 높은 온도에서 저항 없이 전기를 전달할 수 있는 고급 재료입니다. 전통적인 초전도체는 절대 영도에 가까운 온도에서 작동하지만, HTS 재료는 77켈빈 이상에서 작동하며 액체 질소 냉각 시스템과 호환됩니다. 이 시스템은 비용 효율적이고 관리가 용이해 HTS를 고에너지 효율이 요구되는 응용 분야, 예를 들어 차세대 전력 시스템, 교통, 고급 의료 영상 기술 등에서 유망한 옵션으로 자리매김하고 있습니다.

모든 분야에서 전기 성능 개선에 대한 수요가 증가하면서 HTS 재료의 채택이 촉진되고 있습니다. 이러한 초전도체는 특히 송전 그리드를 업그레이드하고 에너지 손실을 최소화하기 위해 현대적인 에너지 인프라에 통합되고 있습니다. 전 세계 정부와 유틸리티 업체들은 노후화된 시스템의 개편에 중점을 두고 있으며, HTS 기반 솔루션은 효율성과 낮은 운영 손실로 더 높은 전력 부하를 처리할 수 있는 능력으로 인해 필수적인 요소로 간주되고 있습니다. 이러한 노력은 지속 가능한 에너지에 대한 전 세계적 추세와 증가하는 전기 소비 및 분산형 에너지 자원을 수용할 수 있는 탄력적인 전력 인프라의 필요성에 의해 더욱 촉진되고 있습니다. 초전도 장치를 고장 전류 제한, 전력 품질 향상, 전력망 성능 최적화에 활용하는 것은 이 추세를 가속화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작금액 | 7억 2,960만 달러 |

| 예측 금액 | 16억 달러 |

| CAGR | 8.5% |

다양한 HTS 유형 중에서 이트륨 바륨 구리 산화물(YBCO)이 계속 시장을 독점하고 있습니다. 이 부문은 2024년에 전 세계 점유율의 35.1%를 차지하고 11억 달러의 가치를 달성했습니다. YBCO는 약 90 켈빈에서 안정적인 성능을 발휘해 냉각 로지스틱스를 단순화하며 우수한 전류 밀도와 강한 자기장 저항성을 제공합니다. 이러한 특징으로 고출력 및 자석 중심 응용 분야에 적합합니다. 기존 초전도체와 비교해 YBCO는 열 관리 및 운영 효율성이 우수해 상업용 및 실험용 배포에서 널리 채택되고 있습니다.

1세대 HTS 전선 부문은 2034년까지 7억 6,180만 달러에 달할 것으로 예상되며, 연평균 11.6%의 놀라운 성장률을 보일 것으로 전망됩니다. BSCCO 화합물을 기반으로 한 1세대 전선은 파우더 인 튜브(Powder-In-Tube) 방법과 같은 성숙한 생산 기술 덕분에 상용화되었습니다. 이 과정은 초전도 분말을 은 기반 관에 넣고 와이어로 형성하는 방식으로, 효율적이고 대량 생산이 쉬운 전도체를 생성합니다. 이 와이어는 액체 질소와 호환되는 온도에서 효율적으로 작동하며, 냉각 비용을 줄여 에너지 시스템과 과학 연구 분야의 시범 규모 및 소량 생산 응용 분야에서 매력적인 옵션으로 부상하고 있습니다.

에너지는 HTS 재료의 가장 큰 응용 부문으로, 2024년에는 11억 달러의 규모로 2025년부터 2034년까지 연평균 12%의 성장률을 보이며 전체 시장의 35.4%를 차지할 것으로 예상됩니다. 전 세계 전력 인프라의 전환은 전기 손실 없이 전기를 전송할 수 있는 재료에 크게 의존합니다. HTS를 적용한 전력선 및 부품은 전통적인 구리나 알루미늄 케이블보다 장거리에서 더 높은 전류를 전송할 수 있으며, 특히 인구 밀도가 높고 신규 설치 공간이 제한된 지역에서 효과적입니다. 이러한 기술의 도입은 에너지 손실을 줄이고 시스템 신뢰성을 향상시켜 현대적인 전기 배전 네트워크에 필수적입니다.

미국에서는 2024년 시장 규모가 9억 8,640만 달러에 달했으며, 2034년까지 연평균 성장률(CAGR) 12.4%로 확장될 것으로 예상됩니다. 연방 기관, 민간 기업, 연구 기관 간의 자금 지원과 협력이 국가의 전력망 현대화 및 방위 및 청정 에너지 분야 신기술 탐색 노력의 핵심입니다. 시스템의 취약성을 해결하면서 더 뛰어난 성능을 발휘할 수 있는 초전도 전력 장치에 초점을 맞춘 프로젝트에 투자가 집중되고 있습니다. 이러한 투자는 국가 인프라를 강화하고 에너지 독립을 추진하기 위한 광범위한 전략의 일환입니다.

고온 초전도체의 시장 전망은 기존 기업과 틈새 시장 혁신 기업이 혼재된 상태로, 경쟁이 다소 치열합니다. 이 분야에 종사하는 기업들은 경쟁력을 유지하기 위해 수직 통합형 운영, 첨단 연구 역량, 협력 파트너십을 갖추고 있는 경우가 많습니다. 대형 기업은 광범위한 제조 경험과 인프라를 제공하며, 소규모 기업은 전문 기술과 재료 개발을 통해 기여합니다. 의료, 에너지, 교통 등 분야에서의 변화하는 수요에 대응하기 위해 지속적인 혁신과 산업, 학계, 정부 간의 전략적 협력은 필수적입니다. 이 지속적인 협력이 고온 초전도체 기술의 다음 단계 발전을 이끌 것으로 예상됩니다.

The Global High-Temperature Superconductors Market was valued at USD 729.6 million in 2024 and is estimated to grow at a CAGR of 8.5% to reach USD 1.6 billion by 2034. High-temperature superconductors, often referred to as HTS, are advanced materials capable of conducting electricity without resistance at temperatures significantly higher than traditional superconductors. Unlike conventional counterparts that operate near absolute zero, HTS materials function at or above 77 Kelvin, making them compatible with liquid nitrogen cooling systems, which are both cost-effective and easier to manage. This key attribute positions HTS as a favorable option in applications requiring high energy efficiency, including next-generation power systems, transportation, and advanced medical imaging technologies.

Growing demand for enhanced electrical performance across sectors is playing a pivotal role in driving the adoption of HTS materials. These superconductors are being integrated into modern energy infrastructures, particularly for upgrading transmission grids and minimizing energy losses. Governments and utilities worldwide are placing emphasis on revamping aging systems, and HTS-based solutions are being considered essential due to their efficiency and ability to handle higher power loads with lower operational losses. These initiatives are further encouraged by the global push for sustainable energy and the need for resilient power infrastructures that can accommodate rising electricity consumption and distributed energy resources. The use of superconducting devices in limiting fault currents, enhancing power quality, and optimizing grid performance is adding to the momentum.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $729.6 Million |

| Forecast Value | $1.6 Billion |

| CAGR | 8.5% |

Among various HTS types, Yttrium Barium Copper Oxide (YBCO) continues to dominate the market. This segment accounted for 35.1% of the global share in 2024 and reached a valuation of USD 1.1 billion. YBCO remains preferred due to its stable performance at nearly 90 Kelvin, which simplifies cooling logistics while providing superior current density and the ability to withstand strong magnetic fields. These features make it suitable for use in high-power and magnet-centric applications. Compared to older superconductors, YBCO delivers better thermal management and operational efficiency, which has led to its wide-scale use in commercial and experimental deployments.

The first-generation HTS wires segment is projected to hit USD 761.8 million by 2034, growing at an impressive CAGR of 11.6%. First-generation wires, based on BSCCO compounds, have achieved commercial availability thanks to mature production techniques like the Powder-In-Tube method. This process involves placing superconducting powder into silver-based tubes and forming them into wires, resulting in conductors that are both effective and easier to produce at scale. These wires function efficiently at temperatures compatible with liquid nitrogen, reducing the overall cost of cooling and making them an attractive option for pilot-scale and low-volume applications in energy systems and scientific research.

Energy remains the largest application segment for HTS materials, with a valuation of USD 1.1 billion in 2024 and expected to grow at a CAGR of 12% from 2025 to 2034, capturing 35.4% of the total market. The transformation of global power infrastructure relies heavily on materials that can transmit electricity without losses. HTS-enabled power lines and components are capable of transmitting higher currents over long distances compared to conventional copper or aluminum cables, particularly in areas with dense urban populations and limited physical space for new installations. Their deployment reduces energy dissipation and enhances system reliability, making them essential for modern electricity distribution networks.

In the United States, the market reached a valuation of USD 986.4 million in 2024 and is set to expand at a CAGR of 12.4% through 2034. Increased funding and collaboration between federal agencies, private entities, and research institutions are central to the country's efforts to modernize its power grid and explore new technologies for defense and clean energy. Investments are being channeled into projects focusing on superconducting power devices that can deliver greater performance while addressing system vulnerabilities. These investments are part of broader strategies aimed at reinforcing national infrastructure and advancing energy independence.

The market landscape for high-temperature superconductors is moderately competitive, with a mix of established corporations and niche innovators. Companies involved in this field often possess vertically integrated operations, advanced research capabilities, and collaborative partnerships to remain competitive. Larger enterprises bring in extensive manufacturing experience and infrastructure, while smaller players contribute through specialized technologies and materials development. Continued innovation, along with strategic alliances between industry, academia, and government, is vital for keeping pace with evolving demands in sectors such as healthcare, energy, and transportation. This ongoing collaboration is expected to shape the next phase of high-temperature superconductivity advancements.