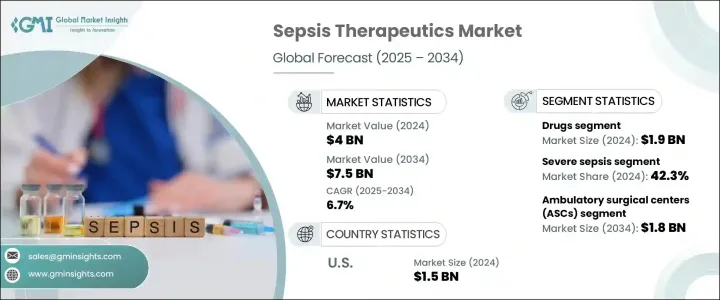

세계의 패혈증 치료제 시장은 2024년에는 40억 달러로 평가되었고 2034년에는 75억 달러에 이를 것으로 예측되며, CAGR 6.7%로 성장할 전망입니다.

신체 방어 시스템이 통제 불능 상태로 악화되면 건강한 조직을 손상시키고 심각한 장기 기능 장애를 초래할 수 있습니다. 병원 내 감염의 전 세계적 부담 증가와 고령화 인구로 인해 차세대 치료법 개발이 시급합니다.

세계의 의료 시스템은 적시적이고 정확한 패혈증 치료 제공의 필요성에 직면하며, 차세대 치료 옵션 개발 압력이 강화되고 있습니다. 패혈증 발생률이 계속 증가함에 따라 제약 및 바이오테크 기업들은 혁신적인 치료법 개발을 위해 연구 개발 투자를 확대하고 있습니다. 이 혁신의 급증은 면역 반응을 조절하고 환자 생존율을 개선하는 것을 목표로 하는 생물학적 제제 및 면역요법 파이프라인의 성장에서 특히 두드러집니다. 전통적인 항생제가 항생제 내성으로 인해 한계에 직면함에 따라 새로운 약물 클래스와 정밀 기반 치료법에 대한 수요는 그 어느 때보다 높습니다. 임상적 이해의 진전과 지원적인 규제 환경은 패혈증 치료 전략의 진화를 더욱 가속화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 40억 달러 |

| 예측 금액 | 75억 달러 |

| CAGR | 6.7% |

2024년에 약물 부문은 19억 달러의 매출을 올렸습니다. 항생제, 항바이러스제, 항진균제, 혈관 수축제 및 면역 조절제는 계속해서 패혈증 관리의 기초를 이루고 있습니다. 광범위 항생제의 신속한 투여는 치료 초기 단계에서 병원체를 억제하는 데 필수적입니다. 코르티코스테로이드와 혈관수축제 등 지원 치료는 환자의 상태를 안정화시키고 전신 염증을 감소시킵니다. 약물 내성으로 인해 패혈증 사례가 복잡해지면서 제약 개발업체들은 더 나은 임상 결과를 제공할 수 있는 표적 치료제에 집중하고 있습니다.

2024년에는 중증 패혈증 부문이 42.3%의 점유율을 차지했습니다. 많은 사례가 광범위한 염증과 장기 부전을 특징으로 하는 이 중증 단계로 빠르게 진행됩니다. 특히 약물 내성 감염의 위협이 커지는 가운데 이러한 임상 증상의 복잡성이 증가함에 따라, 더 강력하고 다중 표적 치료 솔루션의 필요성이 강조되고 있습니다. 의료 서비스 제공자들은 증상의 악화를 방지하고 환자의 치료 결과를 개선하기 위해 초기 진단과 개인 맞춤형 치료를 강조하고 있습니다.

미국의 패혈증 치료제 시장은 2024년에 15억 달러를 달성했습니다. 고령 인구 증가, 병원 감염률 증가, 의료 서비스의 지속적인 개선 등 여러 요인이 이러한 견고한 성과에 기여했습니다. 패혈증 진단에 AI와 기계 학습을 통합하는 것이 주목을 받고 있으며, 이를 통해 위험에 처한 환자를 더 빠르고 정확하게 식별할 수 있게 되었습니다. 또한, 적극적인 R&D 프로그램과 제품 파이프라인 확장에 대한 집중적인 투자는 이 분야의 미국 리더십을 더욱 강화하고 있습니다. 이러한 발전은 정밀하고 기술 기반의 치료가 패혈증 관리에 중심적인 역할을 하는 미래를 만들어가고 있습니다.

세계의 패혈증 치료제 시장에서 기업들은 혁신, 임상 파트너십, 파이프라인 확장에 초점을 맞춘 전략을 채택해 시장 지위를 공고히 하고 있습니다. 북미와 유럽의 기업들은 고급 생물학적 제제, 차세대 항생제, 면역요법 개발을 위해 연구 협력 관계를 강조하고 있습니다. Pfizer, F. Hoffmann-La Roche, Cipla 등 기업은 패혈증 진단 및 개입을 가속화하기 위해 새로운 약물 전달 시스템과 AI 통합 진단 플랫폼에 투자하고 있습니다. 많은 기업들이 특히 아시아태평양 시장에서 신흥 수요를 활용하기 위해 Phase II 및 III 임상 시험을 진행 중입니다. 라이선스 계약, 합병, 지역 제조 역량은 중동 및 아프리카와 같은 시장에서 패혈증 치료 격차가 여전히 큰 지역에서 주목받고 있습니다.

The Global Sepsis Therapeutics Market was valued at USD 4 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 7.5 billion by 2034, driven by a life-threatening condition triggered by an unregulated immune reaction to infection, which requires immediate and targeted medical attention. When the body's defense system spirals out of control, it can damage healthy tissues and lead to severe organ failure. With the rising global burden of hospital-acquired infections and an aging population, there is an urgent need for next-generation therapies.

Healthcare systems worldwide are increasingly strained by the need to deliver timely and precise sepsis care, intensifying the push for next-generation treatment options. As the incidence of sepsis continues to rise, pharmaceutical and biotech companies are stepping up investments in research and development to discover breakthrough therapies. This surge in innovation is especially apparent in the growing pipeline of biologics and immunotherapies that aim to modulate the body's immune response and improve patient survival rates. With traditional antibiotics facing limitations due to antimicrobial resistance, the demand for novel drug classes and precision-based therapies has never been higher. Advancements in clinical understanding, combined with supportive regulatory environments, are further accelerating the evolution of sepsis treatment strategies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4 Billion |

| Forecast Value | $7.5 Billion |

| CAGR | 6.7% |

In 2024, the drug segment generated USD 1.9 billion. Antibiotics, antivirals, antifungals, vasoconstrictors, and immunomodulators continue to be the foundation of sepsis management. Prompt administration of broad-spectrum antibiotics is essential to combat pathogens early in treatment. Supportive therapies, including corticosteroids and vasopressors, stabilize patients and reduce systemic inflammation. With sepsis cases becoming more complex due to drug resistance, pharmaceutical developers are focusing on more targeted therapies that can offer greater clinical outcomes.

In 2024, the severe sepsis segment held a 42.3% share. Many cases progress rapidly to this critical stage, characterized by extensive inflammation and organ failure. The increasing complexity of these clinical presentations, especially amid the growing threat of drug-resistant infections, underscores the need for more potent, multi-targeted therapeutic solutions. Healthcare providers emphasize early-stage diagnostics and personalized medicine to prevent escalation and improve patient outcomes.

United States Sepsis Therapeutics Market generated USD 1.5 billion in 2024. Several factors contribute to this robust performance, including a rising elderly population, a high rate of hospital-acquired infections, and continuous improvements in healthcare delivery. Integrating AI and machine learning in sepsis diagnostics is gaining traction, allowing for faster, more accurate identification of at-risk patients. Additionally, active R&D programs and a strong focus on expanding product pipelines reinforce the country's leadership in the field. These developments are shaping a future where precision-driven, technology-enabled care plays a central role in sepsis management.

In the Global Sepsis Therapeutics Market companies are adopting strategies focused on innovation, clinical partnerships, and pipeline expansion to solidify their position. Players in North America and Europe emphasize research alliances to develop advanced biologics, next-gen antibiotics, and immunotherapies. Firms such as Pfizer, F. Hoffmann-La Roche, and Cipla are investing in novel drug delivery systems and AI-integrated diagnostic platforms to speed up sepsis detection and intervention. Many companies are progressing through Phase II and III clinical trials, especially in the Asia Pacific market, to tap into emerging demand. Licensing agreements, mergers, and regional manufacturing capabilities are also gaining traction in markets like Latin America and the Middle East & Africa, where the sepsis treatment gap remains wide.