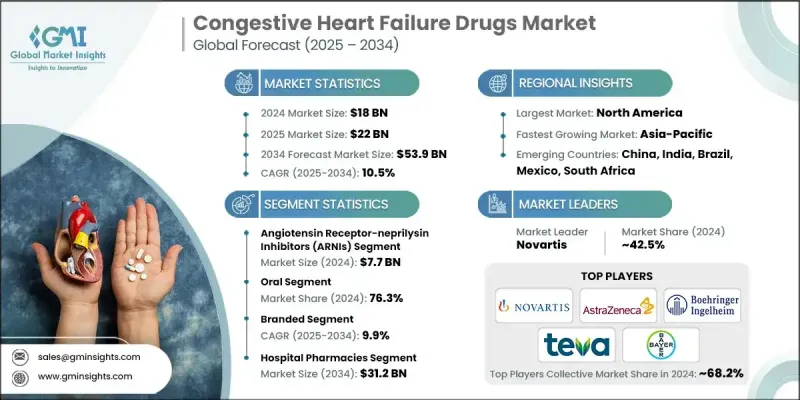

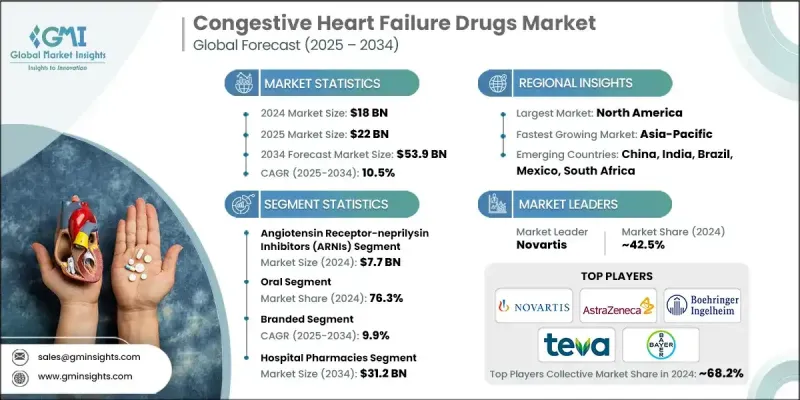

세계의 울혈성 심부전 치료제 시장은 2024년에 180억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 10.5%로 성장하여 539억 달러에 이를 것으로 예측됩니다.

시장 성장은 심부전 유병률 증가, 의약품 개발의 발전, 가이드라인에 기반한 약물 치료의 확대에 의해 주도되고 있습니다. ACE 억제제, 베타차단제, 이뇨제 등 기존 치료제와 더불어 SGLT2 억제제, ARNIs 등 새로운 약제군의 도입 확대로 생존율이 향상되고 입원이 감소하고 있어 대상 환자군이 확대되고 있습니다. 원격 의료와 원격 모니터링의 통합이 진행됨에 따라 조기 개입, 보다 엄격한 치료 최적화, 장기적인 복약 순응도 향상, 급성기 및 만성기 치료 환경 모두에서 약물 사용을 촉진하고 있습니다. 제약사들은 또한 파이프라인 혁신, 병용요법, 광범위한 심부전 표현형에 대한 적응증 확대에 집중하고 있으며, 이는 예측 기간 동안 시장 성장을 더욱 가속화할 것입니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 개시 연도 시장 규모 | 180억 달러 |

| 예측 금액 | 539억 달러 |

| CAGR | 10.5% |

울혈성 심부전 치료제 시장은 주로 투여 경로에 따라 분류되며, 2024년 경구 투여 부문이 76.3%를 차지할 것으로 예측됩니다. 경구용 치료제는 편리성, 자가 투여의 용이성, 낮은 투여 비용, 그리고 만성 심부전의 장기적인 재택 관리 적합성 때문에 선호되고 있습니다. 서방형 제제, 1일 1회 투여 제제, 고정용량 복합제는 복잡한 치료 계획을 간소화하여 여러 동반 질환을 관리하는 환자의 복약 순응도와 치료 결과를 개선합니다. 또한, ACE 억제제, 베타차단제, SGLT2 억제제 등 강력한 경구용 약물의 보급 확대는 외래 진료 및 원격의료 활용 진료 모델 모두에서 이 부문의 우위를 강화하고 있습니다.

유통 채널별로는 급성 심부전 환자의 높은 부담(집중적인 프로토콜에 기반한 치료가 필요한)을 배경으로 2024년 병원 약국 부문은 312억 달러 시장 규모를 창출할 것으로 예측됩니다. 이들 시설에서는 정맥강심제, 이뇨제, ARNIs(아르기닐리신뉴클레오티드분해효소억제제), SGLT2 억제제 등 첨단 치료제를 복합적으로 조합하여 관리함으로써 막대한 약품 소비를 견인하고, 치료 시작과 최적화를 위한 중요한 거점으로서 병원 약국의 위상을 확립하고 있습니다. 하고 있습니다.

북미 울혈성 심부전 치료제 시장은 2024년 53.9%의 점유율을 차지했습니다. 이러한 우위는 많은 진단 환자 수, 혁신적 치료법의 조기 도입, 강력한 상환 제도, 그리고 가이드라인 업데이트와 신물질 도입을 가속화하는 탄탄한 임상 연구 인프라에 의해 뒷받침되고 있습니다.

The Global Congestive Heart Failure Drugs Market was valued at USD 18 billion in 2024 and is estimated to grow at a CAGR of 10.5% to reach USD 53.9 billion by 2034.

Market growth is driven by the rising prevalence of heart failure, advances in drug development, and the expansion of guideline-directed medical therapy. Growing adoption of novel classes such as SGLT2 inhibitors and ARNIs, alongside established therapies like ACE inhibitors, beta-blockers, and diuretics, is improving survival outcomes and reducing hospitalizations, thereby expanding the addressable patient pool. Increasing integration of telemedicine and remote monitoring is enabling earlier intervention, tighter therapy optimization, and better long-term adherence, which in turn is boosting drug utilization across acute and chronic care settings. Pharmaceutical companies are also focusing heavily on pipeline innovation, combination therapies, and label expansions into broader heart failure phenotypes, further accelerating market momentum over the forecast horizon.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18 Billion |

| Forecast Value | $53.9 Billion |

| CAGR | 10.5% |

The Congestive Heart Failure Drugs Market is primarily segmented by route of administration, where the oral segment held 76.3% in 2024. Oral therapies are preferred due to their convenience, ease of self-administration, lower administration costs, and suitability for long-term, home-based management of chronic heart failure. Extended-release, once-daily, and fixed-dose combination formulations simplify complex regimens, improving adherence and outcomes for patients managing multiple comorbidities. In addition, the expanding availability of potent oral agents such as ACE inhibitors, beta-blockers, and SGLT2 inhibitors reinforces the dominance of this segment in both outpatient and telemedicine-enabled care models.

By distribution channel, the hospital pharmacies segment generated USD 31.2 billion in 2024, underpinned by the high burden of acute decompensated heart failure cases requiring intensive, protocol-driven therapy. These settings manage complex combinations of intravenous inotropes, diuretics, and advanced therapies like ARNIs and SGLT2 inhibitors, driving substantial drug consumption and positioning hospital pharmacies as a critical node in treatment initiation and optimization.

North America Congestive Heart Failure Drugs Market held a 53.9% share in 2024. This dominance is supported by a high diagnosed patient base, early adoption of innovative therapies, strong reimbursement frameworks, and robust clinical research infrastructure that accelerates guideline updates and uptake of new molecules.

Key companies operating in the Global Congestive Heart Failure Drugs Market include Novartis, AstraZeneca, Boehringer Ingelheim, Bayer, Teva Pharmaceutical, Pfizer, Sanofi, Johnson & Johnson, GlaxoSmithKline, Merck & Co., Merck KGaA, Lexicon Pharmaceuticals, Zensun Sci & Tech, Amgen, and AdvaCare Pharma, which collectively shape the competitive landscape through extensive portfolios, global commercial footprints, and active R&D strategies. In the Congestive Heart Failure Drugs Market, leading companies are adopting a mix of product innovation, lifecycle management, strategic collaborations, and geographic expansion to strengthen their market foothold. Many players are investing heavily in R&D for novel mechanisms of action, including SGLT2 inhibitors, ARNI-based combinations, vasodilators, and other advanced drug classes, while also pursuing label expansions into broader heart failure populations such as HFpEF and patients with comorbid diabetes or chronic kidney disease.