슬래그 시멘트(GGBFS) 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

Slag Cement (GGBFS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1750344

리서치사:Global Market Insights Inc.

발행일:2025년 05월

페이지 정보:영문 220 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

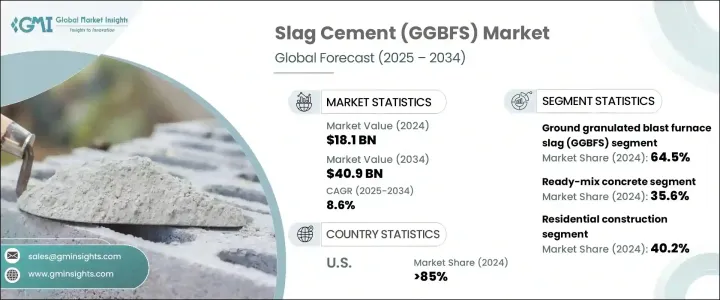

세계의 슬래그 시멘트 시장은 2024년 181억 달러로 평가되었고, 인프라 투자 증가, 지속 가능한 건축자재 수요 증가, 저탄소 실적 대체물 규제 지원에 견인되어 CAGR 8.6%로 성장할 전망이며, 2034년 409억 달러에 이를 것으로 추정됩니다.

슬래그 시멘트, 특히 고로 수쇄 슬래그(GGBFS)는 뛰어난 성능 특성으로 현대 건설에서 점점 선호되고 있습니다. GGBFS는 압축 강도의 향상과 투수성의 저감을 실현할 뿐만 아니라, 내약품성도 대폭 향상시키기 때문에, 가혹한 환경 조건에 최적입니다. 이러한 특성은 인프라의 수명 연장에 기여하고 장기간에 걸친 보수의 빈도와 비용을 줄입니다. 또한 GGBFS는 수화열을 저하시키기 때문에 대규모 콘크리트 타설에서의 열 균열을 방지하고 구조물의 무결성을 높이는 데 도움이 됩니다. 또한 GGBFS를 콘크리트 혼합물에 사용함으로써 작업성과 마감 품질이 향상되어 건설 공정과 마감 모두에 혜택을 가져다 줍니다. 지속 가능성이 건축 관행의 우선 사항이 됨에 따라 슬래그 시멘트의 저탄소 풋프린트는 주택 및 대규모 인프라 프로젝트의 가치를 더욱 높이고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

181억 달러

예측 금액

409억 달러

CAGR

8.6%

2024년 시장 점유율은 GGBFS 분야가 64.5%를 차지했습니다. 뛰어난 강도, 투수성 저하, 내구성 향상으로 교량, 터널, 해양 구조물 등 중요한 인프라 프로젝트에 이상적입니다. 또한 GGBFS는 콘크리트의 이산화탄소 배출량을 줄이는 데 기여하고 지속 가능한 건축 관행에서의 사용을 촉진합니다.

주택 건설 부문은 2024년 40.2% 시장 점유율을 차지했습니다. 주택 수요가 증가함에 따라 내구성이 있고 오래 지속되는 건축자재가 필요합니다. 슬래그 시멘트는 그 뛰어난 강도, 수축률의 저감, 내화성에 의해 주택 프로젝트에서 인기를 끌고 있으며, 지속 가능한 주택을 목표로 하는 동향에 합치하고 있습니다.

북미의 슬래그 시멘트 시장은 85%의 점유율을 차지했으며, 2024년 시장 규모는 180만 달러였습니다. 인프라 투자 및 고용촉진법(IIJA)과 같은 정책이 슬래그 시멘트와 같은 고성능 건축자재에 대한 수요를 높이고 있습니다. 또한 탄소 삭감을 추진하는 건설 업계가 슬래그 시멘트의 채용을 가속화하고 있어, 콘크리트 마무리의 전체적인 카본 풋 프린트를 삭감하고 있습니다.

세계의 슬래그 시멘트 시장의 주요 기업은 JSW Cement, CEMEX SAB de CV, Ecocem Materials, Holcim Group, Heidelberg Materials 등입니다. 이러한 기업은 시장에서의 존재감을 높이기 위해 다양한 전략을 채용하고 있습니다. 이러한 기업은, 내구성의 향상이나 생산 비용의 삭감 등, 슬래그 시멘트의 성능 특성을 개선하기 위한 연구 개발에 투자하고 있습니다. 또한 신흥 시장에서의 수요 증가에 대응하기 위해 생산 능력을 확대하고 있습니다. 또, 신시장에 대한 참가 및 현지의 전문 지식을 활용하기 위해서, 전략적 파트너십이나 제휴도 진행하고 있습니다. 게다가 이러한 기업은 지속 가능성에의 대처에 중점을 두어 환경 규제나 환경 친화적인 제품에 대한 소비자의 기호에 맞춘 사업 운영을 실시하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

원재료 공급자

제조업자

리셀러

최종 용도

이익률 분석

COVID-19에 의한 밸류체인의 혼란

트럼프 정권의 관세 영향 : 구조화된 개요

무역에 미치는 영향

무역량의 혼란

보복 조치

업계에 미치는 영향

공급측의 영향(원재료)

주요 원재료의 가격 변동

공급망 재구성

생산 비용에 미치는 영향

수요측의 영향(판매가격)

최종 시장에 대한 가격 전달

시장 점유율 동향

소비자의 반응 패턴

영향을 받는 주요 기업

전략적인 업계 대응

공급망 재구성

가격 설정 및 제품 전략

정책관여

전망 및 향후 검토 사항

무역 통계(HS 코드) 참고 : 위의 무역 통계는 주요 국가에 대해서만 제공됩니다

주요 수출국

주요 수입국

이익률 분석

주요 뉴스 및 대처

기술의 상황

전통적인 제조 기술

첨단 제조 기술

신흥 기술

특허 분석

규제 상황

시장 역학

시장 성장 촉진요인

환경규제 및 지속가능성에 대한 노력

인프라 개발 확대

종래의 시멘트에 비해 비용면에서 유리

뛰어난 기술적 특성 및 성능상의 이점

시장 성장 억제요인

고품질 고로 슬래그의 한정된 공급

탈탄소화의 노력에 의한 고로 가동의 감소

특정 용도의 기술적 제한

인식 및 기술적 지식의 부족

시장 기회

친환경 건축재료에 대한 주목 고조

내구성 있는 인프라에 대한 수요 증가

슬래그 처리에서 기술적 진보

지속가능한 건설에 대한 정부의 인센티브

시장의 과제

다른 보조 시멘트 재료와의 경쟁

공급망의 혼란

지역 가용성 제약

표준화 및 품질관리 문제

규제 틀 분석

국제 규격(ASTM c989/c989m, EN 197-1)

지역의 규제 및 기준

환경 컴플라이언스 요건

품질인증시스템

기술의 상황

현재의 기술 동향

슬래그 시멘트 제조에 있어서의 신기술

디지털화와 인더스트리 4.0의 영향

연구개발 이니셔티브와 혁신 파이프라인

가격 분석

가격 동향 분석

비용 구조 분석

가격에 영향을 미치는 요인

지역별 가격 차이

PESTEL 분석

제4장 경쟁 구도

시장 점유율 분석

전략적 대시보드

주요 이해관계자 및 시장 포지셔닝

경쟁 벤치마킹

경쟁 포지셔닝 매트릭스

경쟁 전략

신제품 개발

합병 및 인수

파트너십 및 협업

능력 확장

제5장 시장 추계 및 예측 : 유형별(2021-2034년)

주요 동향

분쇄 고로 슬래그(GGBFS)

학년 80

학년 100

학년 120

포틀랜드 슬러그 시멘트(PSC)

낮은 슬래그 함유량(25-35%)

중간 정도의 슬래그 함유량(36-50%)

높은 슬래그 함유량(51-65%)

과황산 시멘트

기타 슬래그계 시멘트

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

생 콘크리트

프리캐스트 콘크리트

고성능 콘크리트

매스 콘크리트의 용도

분출 콘크리트

콘크리트 블록과 포장재

박격포와 그라우트

토양 안정화

기타

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

주요 동향

주택 건설

단독주택

집합 주택

상업 건설

오피스 빌딩

소매업 및 접객

교육기관

의료시설

인프라 개발

도로 및 고속도로

다리 및 터널

댐 및 수력 발전 프로젝트

철도 및 교통 시스템

공항

항만 및 해양구조물

산업 건설

제조 시설

발전소

석유 및 가스 시설

수처리장 및 폐수처리장

기타

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제9장 기업 프로파일

Ambuja Cements Ltd

Boral Limited

Buzzi Unicem

CEMEX SAB de CV

Ecocem Materials

Heidelberg Materials

Holcim Group

JFE Mineral &Alloy

JSW Cement

Lafarge

Nippon Steel Corporation

Royal White Cement

Tarmac(CRH)

Texas Lehigh Cement Company LP

Titan America

UltraTech Cement Ltd

AJY

영문 목차

영문목차

The Global Slag Cement Market was valued at USD 18.1 billion in 2024 and is estimated to grow at a CAGR of 8.6% to reach USD 40.9 billion by 2034, driven by increasing investments in infrastructure, a growing demand for sustainable construction materials, and regulatory support for alternatives with a low carbon footprint.

Slag cement, especially ground granulated blast furnace slag (GGBFS), is increasingly preferred in modern construction due to its exceptional performance characteristics. It not only delivers enhanced compressive strength and reduced permeability but also significantly improves resistance to chemical attacks, making it ideal for aggressive environmental conditions. These attributes contribute to longer-lasting infrastructure, reducing the frequency and expense of repairs over time. Additionally, GGBFS reduces the heat of hydration, which helps prevent thermal cracking in large concrete pours, thereby increasing structural integrity. Its use in concrete mixtures also improves workability and finish quality, benefiting both the construction process and the result. As sustainability becomes a priority in building practices, the low-carbon footprint of slag cement further amplifies its value in residential and large-scale infrastructure projects.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$18.1 Billion

Forecast Value

$40.9 Billion

CAGR

8.6%

The GGBFS segment accounted for 64.5% of the market share in 2024. Its superior strength, decreased permeability, and increased durability make it ideal for critical infrastructure projects, including bridges, tunnels, and marine structures. Additionally, GGBFS contributes to reducing the carbon footprint of concrete, promoting its use in sustainable building practices.

The residential construction segment held a 40.2% market share in 2024. As demand for housing increases, there is a need for durable, long-lasting building materials. Slag cement is gaining popularity in residential projects due to its superior strength, reduced shrinkage, and fire resistance, aligning with the trend towards sustainable housing.

North America Slag Cement Market held 85% share and was valued at USD 1.8 million in 2024, attributed to expanding infrastructure investments and a strong interest in sustainable construction. Policies like the Infrastructure Investment and Jobs Act (IIJA) have driven high demand for high-performance building materials like slag cement. Furthermore, the construction industry's push for carbon reduction is accelerating the adoption of slag cement, reducing the overall carbon footprint of concrete finishes.

Key players in the Global Slag Cement Market include JSW Cement, CEMEX S.A.B. de C.V., Ecocem Materials, Holcim Group, and Heidelberg Materials. These companies are adopting various strategies to strengthen their market presence. They are investing in research and development to improve the performance characteristics of slag cement, such as enhancing its durability and reducing production costs. Additionally, they are expanding their production capacities to meet the growing demand in emerging markets. Strategic partnerships and collaborations are also being pursued to access new markets and leverage local expertise. Furthermore, these companies focus on sustainability initiatives, aligning their operations with environmental regulations and consumer preferences for eco-friendly products.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Research methodology

1.2 Research objectives

1.3 Market definition and scope

1.4 Market segmentation

1.5 Data sources

1.5.1 Primary research

1.5.2 Secondary research

1.6 Market estimation approach

1.7 Research assumptions and limitations

1.8 Base year and forecast period

Chapter 2 Executive Summary

2.1 Market overview

2.2 Market dynamics snapshot

2.3 Key market trends

2.4 Regional insights

2.5 Competitive landscape snapshot

2.6 Future market outlook

2.7 Investment highlights

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Raw material suppliers

3.1.2 Manufacturers

3.1.3 Distributors

3.1.4 End use

3.1.5 Profit margin analysis

3.1.6 Value chain disruptions due to covid-19

3.2 Impact of trump administration tariffs - structured overview

3.2.1 Impact on trade

3.2.1.1 Trade volume disruptions

3.2.1.2 Retaliatory measures

3.2.2 Impact on the industry

3.2.2.1.1 Supply-side impact (raw materials)

3.2.2.1.2 Price volatility in key materials

3.2.2.1.3 Supply chain restructuring

3.2.2.1.4 Production cost implications

3.2.2.2 Demand-side impact (selling price)

3.2.2.2.1 Price transmission to end markets

3.2.2.2.2 Market share dynamics

3.2.2.2.3 Consumer response patterns

3.2.3 Key companies impacted

3.2.4 Strategic industry responses

3.2.4.1 Supply chain reconfiguration

3.2.4.2 Pricing and product strategies

3.2.4.3 Policy engagement

3.2.5 Outlook and future considerations

3.3 Trade statistics (HS code) Note: the above trade statistics will be provided for key countries only.

3.3.1 Major exporting countries

3.3.2 Major importing countries

3.4 Profit margin analysis

3.5 Key news & initiatives

3.5.1 Technology landscape

3.5.2 Traditional manufacturing technologies

3.5.3 Advanced manufacturing technologies

3.5.4 Emerging technologies

3.5.5 Patent analysis

3.6 Regulatory landscape

3.6.1 North America

3.6.2 Europe

3.6.3 Asia Pacific

3.6.4 Latin America

3.6.5 MEA

3.7 Market dynamics

3.7.1 Market drivers

3.7.1.1 Environmental regulations and sustainability initiatives

3.7.1.2 Growing infrastructure development

3.7.1.3 Cost advantages over traditional cement

3.7.1.4 Superior technical properties and performance benefits

3.7.2 Market restraints

3.7.2.1 Limited availability of high-quality blast furnace slag

3.7.2.2 Declining blast furnace operations due to decarbonization efforts

3.7.2.3 Technical limitations in certain applications

3.7.2.4 Lack of awareness and technical knowledge

3.7.3 Market opportunities

3.7.3.1 Increasing focus on green building materials

3.7.3.2 Rising demand for durable infrastructure

3.7.3.3 Technological advancements in slag processing

3.7.3.4 Government incentives for sustainable construction

3.7.4 Market challenges

3.7.4.1 Competition from other supplementary cementitious materials

3.7.4.2 Supply chain disruptions

3.7.4.3 Regional availability constraints

3.7.4.4 Standardization and quality control issues

3.7.5 Regulatory framework analysis

3.7.5.1 International standards (ASTM c989/c989m, EN 197-1)

3.7.5.2 Regional regulations and standards

3.7.5.3 Environmental compliance requirements

3.7.5.4 Quality certification systems

3.7.6 Technology landscape

3.7.6.1 Current technological trends

3.7.6.2 Emerging technologies in slag cement production

3.7.6.3 Digitalization and industry 4.0 impact

3.7.6.4 R&D initiatives and innovation pipeline

3.7.7 Pricing analysis

3.7.7.1 Price trend analysis

3.7.7.2 Cost structure analysis

3.7.7.3 Factors affecting pricing

3.7.7.4 Regional price variations

3.7.8 Pestle analysis

Chapter 4 Competitive Landscape, 2024

4.1 Market share analysis, 2024

4.2 Strategic dashboard

4.3 Key stakeholders and market positioning

4.4 Competitive benchmarking

4.5 Competitive positioning matrix

4.6 Competitive strategies

4.6.1 New product developments

4.6.2 Mergers and acquisitions

4.6.3 Partnerships and collaborations

4.6.4 Capacity expansions

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion) (Kilo Tons)

5.1 Key trends

5.2 Ground granulated blast furnace slag (GGBFS)

5.2.1 Grade 80

5.2.2 Grade 100

5.2.3 Grade 120

5.3 Portland slag cement (PSC)

5.3.1 Low slag content (25-35%)

5.3.2 Medium slag content (36-50%)

5.3.3 High slag content (51-65%)

5.4 Supersulfated cement

5.5 Other slag-based cements

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

6.1 Key trends

6.2 Ready-mix concrete

6.3 Precast concrete

6.4 High-performance concrete

6.5 Mass concrete applications

6.6 Shotcrete

6.7 Concrete blocks and pavers

6.8 Mortars and grouts

6.9 Soil stabilization

6.10 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Kilo Tons)

7.1 Key trends

7.2 Residential construction

7.2.1 Single-family housing

7.2.2 Multi-family housing

7.3 Commercial construction

7.3.1 Office buildings

7.3.2 Retail and hospitality

7.3.3 Educational institutions

7.3.4 Healthcare facilities

7.4 Infrastructure development

7.4.1 Roads and highways

7.4.2 Bridges and tunnels

7.4.3 Dams and hydroelectric projects

7.4.4 Railways and transit systems

7.4.5 Airports

7.4.6 Ports and marine structures

7.5 Industrial construction

7.5.1 Manufacturing facilities

7.5.2 Power plants

7.5.3 Oil and gas facilities

7.5.4 Water and wastewater treatment plants

7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)