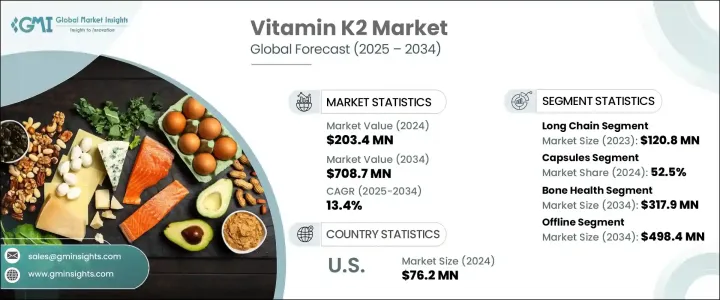

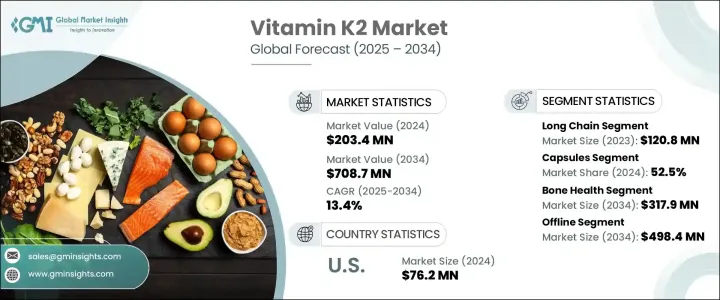

세계의 비타민 K2 시장은 2024년 2억 340만 달러로 평가되었으며, 골다공증, 심장병, 특정 암 등 만성 질환 증가로 13.4%의 연평균 복합 성장률(CAGR)로 성장해 2034년까지 7억 870만 달러에 이를 것으로 추정되고 있습니다.

특히 심혈관과 뼈의 건강 유지에 비타민 K2의 이점에 대한 의식 증가가 모든 연령층에서 보충제 소비 증가에 큰 역할을 담당하고 있습니다. 더 많은 소비자가 영양과 예방 의료에 주목 하는 가운데, 대상이 되는 보충제 수요는 증가의 일도를 따라가고 있습니다.

또한, 신생아의 비타민 K 결핍증, 특히 만성 출혈의 위험을 둘러싼 의학적 우려가 높아짐에 따라 의료 당국은 출생시 보충 섭취의 권장을 강화하고 있습니다. 유아기 영양의 중요성에 대한 보호자와 간병인의 의식이 높아짐에 따라, 유아용으로 조정된 안전하고 효과적이고, 내약성이 높은 비타민 K2 제제에 대한 수요가 확대되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 당초 시장 규모 | 2억 340만 달러 |

| 시장 규모 예측 | 7억870만 달러 |

| CAGR | 13.4% |

긴 사슬형인 MK-7은 뛰어난 흡수성과 체내 반감기의 길이로부터 2024년 제품 카테고리를 지배했습니다. MK-7의 역할을 지지하는 임상 조사 증가는 특히 자연적인 해결책을 요구하는 고령자의 사이에서 그 인기를 한층 더 밀어주고 있습니다. 유기농이며 식물 유래의 보충제에 대한 인식이 높아짐에 따라, 천연 성분 유래의 MK-7에 대한 수요도 증가의 일도를 따르고 있습니다.

제형별로는 캡슐이 시장을 선도했고, 2024년의 점유율은 52.5%였습니다. 소프트젤은 비타민 K2와 같은 지용성 영양소의 생체이용률을 향상시키는 능력이 높게 평가되고 있어, 컴플라이언스 향상과 신속한 작용이 기대되고 있습니다. 또, 보건 당국에 의한 소프트젤 포맷에 대한 규제상의 뒷받침도, 시판 서플리먼트에서의 사용 확대를 뒷받침하고 있습니다.

미국의 비타민 K2 시장은 2024년에는 7,620만 달러로 평가되었으며, 특히 노인들 사이에서 뼈 건강에 대한 관심이 높아지고, 폭넓은 계몽 캠페인이 진행되고 있습니다. 제품이 더 가까워지고 소비자는 광범위한 선택과 편리한 배송 옵션을 얻을 수 있습니다.

Zenith Nutrition, Carlyle Nutritionals, Doctor's Best, Health Veda Organics, Vlado's Himalayan Organics, Amway Nutrilite, NattoPharma, Pharma Cure Laboratories, Kappa Biosciences(Balchem Corporation), WOW Lifesciences, Smarter Vita Organics와 같은 비타민 K2 세계 시장의 주요 기업은 시장에서의 지위를 높이기 위해 전략적 접근법을 채택하고 있습니다. 디지털에서의 프레즌스 확대, 세계적인 리치를 확대하기 위한 유통 파트너십의 형성 등이 포함되어 있습니다.

The Global Vitamin K2 Market was valued at USD 203.4 million in 2024 and is estimated to grow at a CAGR of 13.4% to reach USD 708.7 million by 2034, driven by the rising occurrence of chronic illnesses such as osteoporosis, heart disease, and certain cancers. The growing awareness of vitamin K2's benefits, especially in maintaining cardiovascular and bone health, has played a major role in increasing supplement consumption across all age groups. As more consumers focus on nutrition and preventive care, demand for targeted supplements continues to rise. The increased emphasis on bone density health and the management of conditions like osteoporosis is also accelerating the uptake of vitamin K2 products.

Furthermore, growing medical concern surrounding vitamin K deficiency in newborns, particularly the risk of late-onset bleeding, have prompted healthcare authorities to strengthen recommendations for supplementation at birth. This has led to an uptick in the use of vitamin K2 in pediatric care, opening a rapidly emerging segment focused on infant health. As awareness increases among parents and caregivers about the importance of early-life nutrition, the demand for safe, effective, and well-tolerated vitamin K2 formulations tailored for infants is expanding. Pediatric supplements are now being offered in gentler forms such as drops or oral solutions, which are easy to administer and designed specifically for neonatal needs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $203.4 million |

| Forecast Value | $708.7 million |

| CAGR | 13.4% |

The long-chain form, MK-7, dominated the product category in 2024 due to its superior absorption and extended half-life in the body. MK-7 has gained trust among healthcare professionals who now prefer it for managing bone fragility and reducing cardiovascular risk. Increased clinical research supporting the role of MK-7 in preventing fractures and improving bone mineral density has further propelled its popularity, particularly among aging adults seeking natural solutions. As awareness of organic, plant-based supplements grows, demand for MK-7 sourced from natural ingredients continues to rise.

The capsules segment led the market in terms of dosage form, holding 52.5% share in 2024. The flexibility in formulating capsules, combined with their high absorption rate, has contributed to this growth. Soft gel variants are praised for their ability to improve the bioavailability of fat-soluble nutrients like vitamin K2, resulting in better compliance and faster action. Regulatory backing for soft gel formats from health authorities also supports their expanding use in over-the-counter supplements.

United States Vitamin K2 Market was valued at USD 76.2 million in 2024, driven by the rising interest in bone health, especially among older adults, alongside broader awareness campaigns. The growth of online sales channels has made vitamin K2 products more accessible, offering consumers a wider selection and convenient delivery options. Additionally, efforts to educate the public on the role in preventing bone and heart issues continue to drive market expansion in the country.

Key players in the Global Vitamin K2 Market such as Zenith Nutrition, Carlyle Nutritionals, Doctor's Best, Health Veda Organics, Vlado's Himalayan Organics, Amway Nutrilite, NattoPharma, Pharma Cure Laboratories, Kappa Biosciences (Balchem Corporation), WOW Lifesciences, Smarter Vitamins, Innovix Labs, Phi Naturals, and Mary Ruth Organics are employing strategic approaches to enhance their market position. These include the development of clean-label and organic products, investment in scientific research to validate health claims, expanding their digital presence, and forming distribution partnerships to boost global reach. Many also focus on product differentiation through enhanced bioavailability and unique delivery forms.