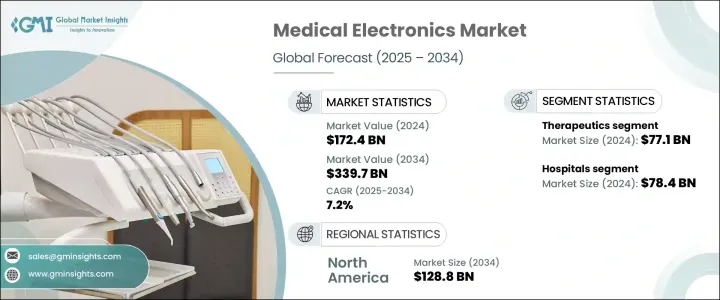

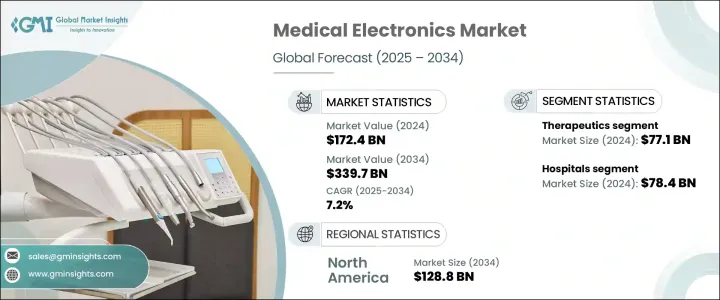

세계의 의료용 일렉트로닉스 시장 규모는 2024년에 1,724억 달러로 평가되었고, CAGR 7.2%로 성장할 전망이며, 2034년에는 3,397억 달러에 이를 것으로 예측됩니다.

이 성장의 원동력은 진단, 치료, 예방, 환자 모니터링을 지원하기 위해 건강 관리 분야 전반에 걸쳐 전자 시스템과 장치의 사용이 확대되고 있다는 점입니다. 헬스케어의 디지털화가 진행됨에 따라, 정세는 임상의가 어떻게 케어를 제공하는지에 변화를 가져오고 있습니다. 화상 진단 툴이나 웨어러블 모니터로부터, 로봇 수술 시스템이나 커넥티드 세라퓨틱스에 이르기까지, 이러한 디바이스는 환자의 경험이나 임상 결과를 재구축하고 있습니다. AI, IoT, 클라우드 컴퓨팅과 같은 스마트 기술의 통합은 업무 효율을 재정의하고 보다 신속한 진단을 가능하게 하며 데이터 정확도를 향상시키고 인적 오류를 줄이고 있습니다. 병원, 진료소, 그리고 재택 의료 환경까지도 워크플로우 합리화, 만성질환 관리, 환자 인게이지먼트 강화를 위해 상호 연결된 의료용 일렉트로닉스에 의존하고 있습니다. 세계의 고령화와 비전염성 질환의 증가로 인해 기술 주도의 헬스케어 솔루션으로의 전환은 분명합니다. 소비자는 개인화된, 접근하기 쉬운, 실시간 헬스케어 서비스를 요구하고 있으며, 기업은 보다 신속한 기술 혁신과 보다 직관적이고 신뢰성 높은 의료용 일렉트로닉스의 도입을 추진하고 있습니다.

심혈관질환, 암, 호흡기질환 등의 만성질환과 감염증의 지속적인 증가가 첨단 의료용 일렉트로닉스에 대한 수요의 급증에 크게 기여하고 있습니다. 질병의 조기 발견 및 예방 의료에 대한 사회적 의식이 높아지고 있어 진단 기술의 보급을 뒷받침하고 있습니다. 동시에 저침습 수술 수기의 진보로 고정밀 전자 도구에 대한 요구가 가속화되고 있습니다. 이러한 기술 혁신은, 실시간 처치 정밀도 향상, 회복 시간 단축, 환자의 임상 전귀의 향상에 도움이 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 1,724억 달러 |

| 예측 금액 | 3,397억 달러 |

| CAGR | 7.2% |

이 시장은 의료용 로봇, 원격 모니터링, 웨어러블 진단 등의 분야에서 진행 중인 기술 혁신에 의해서도 강력한 기세를 보이고 있습니다. 소비자들이 보다 스마트하고 커넥티드한 헬스케어 툴에 경도되는 가운데 의료용 애플리케이션으로의 전자 통합은 계속해서 견인차 역할을 하고 있습니다. 세계 헬스케어 지출의 증가는, 특히 복잡한 처치 및 장기 케어를 관리하기 위해 설계된 고도의 일렉트로닉스 채용을 한층 더 뒷받침하고 있습니다. 이 동향은 실시간 데이터, 강화된 이미지 처리, 정밀한 제어에 대한 수요가 여전히 중요한 특수 의료 분야에서 특히 두드러집니다.

2024년, 치료 분야에서는 만성적인 증상을 관리하기 위한 이식형 및 외장 장치의 사용이 증가하고 있는 것이 원동력이 되어, 771억 달러가 창출되었습니다. 이러한 치료 기술은 고도의 전자 기능을 조합함으로써 안전성, 전달 정확도, 개별화 치료를 향상시킵니다. 페이스 메이커, 신경 자극 장치, 수액 펌프 등의 장치는 삶의 질을 높이고 통원을 줄이기 위해 널리 채택되고 있습니다.

2024년에는 병원이 최종 사용자 채용을 선도하고 784억 달러를 창출해 시장 점유율의 45.5%를 차지했습니다. 이러한 시설에서는 외래 환자나 입원 환자의 치료를 효율적으로 관리하기 위해 진단용 및 치료용 일렉트로닉스 모두에 크게 의존하고 있습니다. 임상 워크플로우를 최적화하고 치료 지연을 최소화하는 데 중점을 둔 병원들은 더 나은 치료 결과를 가져오기 위해 차세대 모니터링 기기, 수술 기술, 영상 처리 시스템에 대한 투자를 지속하고 있습니다.

미국의 의료용 일렉트로닉스 시장은 심혈관질환, 당뇨병, 암, 신경질환 등의 만성질환 부담 증가에 힘입어 2023년 574억 달러를 창출하였습니다. 지속적인 모니터링과 치료를 필요로 하는 환자의 증가에 따라 고도의 의료용 일렉트로닉스에 대한 수요는 계속 높습니다. 미국은 또한 강력한 연구 개발 인프라 및 조기 기술 도입의 혜택을 받고 있으며 의료 기술 혁신의 리더십을 유지하고 있습니다.

세계 의료용 일렉트로닉스 시장의 주요 기업인 Olympus, Shenzhen Mindray Bio-Medical Electronics, Siemens Healthineers, Lepu Medical Technology, Boston Scientific, Toshiba Medical Systems, FUJIFILM Holdings, GE HealthCare, Abbott Laboratories, MicroPort Scientific, Samsung Electronics, Medtronic, Carestream Health, Koninklijke Philips, 및 Esaote 등은 시장에서의 존재감을 높이기 위해 중요한 전략을 실시했습니다. 여기에는 혁신을 빠르게 진행하기 위한 R&D 투자 강화, 실시간 피드백을 얻기 위한 의료 제공자와의 연계, 신흥 시장 진출, AI와 IoT를 활용한 지능형 진단 및 원격 케어 플랫폼 출시 등이 포함됩니다.

The Global Medical Electronics Market was valued at USD 172.4 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 339.7 billion through 2034. This growth is driven by the expanding use of electronic systems and devices across healthcare sectors to support diagnosis, treatment, prevention, and patient monitoring. As the healthcare landscape becomes increasingly digitized, medical electronics are transforming how clinicians deliver care. From diagnostic imaging tools and wearable monitors to robotic surgery systems and connected therapeutics, these devices are reshaping patient experiences and clinical outcomes. The integration of smart technologies like AI, IoT, and cloud computing is redefining operational efficiency, enabling faster diagnostics, improving data accuracy, and reducing human error. Hospitals, clinics, and even home care environments now rely on interconnected medical electronics to streamline workflows, manage chronic diseases, and enhance patient engagement. With an aging global population and the rising incidence of non-communicable diseases, there's a clear shift toward tech-driven healthcare solutions. Consumers are demanding personalized, accessible, and real-time healthcare services, pushing companies to innovate faster and introduce more intuitive, reliable medical electronic devices.

The continuous rise in chronic and infectious diseases-including cardiovascular conditions, cancer, and respiratory disorders-is contributing heavily to the surging demand for advanced medical electronics. There's growing public awareness around early disease detection and preventive care, which is encouraging the widespread use of diagnostic technologies. At the same time, advancements in minimally invasive surgical techniques are accelerating the need for high-precision electronic tools. These innovations are helping improve real-time procedural accuracy, reduce recovery times, and enhance clinical outcomes for patients globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $172.4 Billion |

| Forecast Value | $339.7 Billion |

| CAGR | 7.2% |

The market is also seeing robust momentum from ongoing technological innovation in areas like medical robotics, remote monitoring, and wearable diagnostics. As consumers lean toward smarter, more connected healthcare tools, the integration of electronics in medical applications continues to gain traction. Rising global healthcare expenditures further support the adoption of sophisticated electronic devices, especially those designed to manage complex procedures and long-term care. This trend is particularly evident in specialized medical fields where demand for real-time data, enhanced imaging, and precision control remains critical.

In 2024, the therapeutics segment generated USD 77.1 billion, driven by the increasing use of implantable and external devices to manage chronic conditions. These therapeutic technologies combine advanced electronic features to improve safety, delivery accuracy, and personalized care-especially in cardiovascular, neurological, and respiratory treatment. Devices such as pacemakers, neurostimulators, and infusion pumps are being widely adopted to boost quality of life and reduce hospital visits.

Hospitals led end-user adoption in 2024, generating USD 78.4 billion and accounting for 45.5% of the market share. These institutions depend heavily on both diagnostic and therapeutic electronics to manage outpatient and inpatient care efficiently. With a focus on optimizing clinical workflows and minimizing treatment delays, hospitals continue to invest in next-generation monitoring equipment, surgical technologies, and imaging systems to drive better outcomes.

The U.S. Medical Electronics Market generated USD 57.4 billion in 2023, fueled by the growing burden of chronic diseases such as cardiovascular disorders, diabetes, cancer, and neurological conditions. With more patients requiring continuous monitoring and treatment, the demand for advanced electronic medical devices remains high. The U.S. also benefits from strong R&D infrastructure and early tech adoption, helping sustain its leadership in medical innovation.

Leading players in the Global Medical Electronics Market-including Olympus, Shenzhen Mindray Bio-Medical Electronics, Siemens Healthineers, Lepu Medical Technology, Boston Scientific, Toshiba Medical Systems, FUJIFILM Holdings, GE HealthCare, Abbott Laboratories, MicroPort Scientific, Samsung Electronics, Medtronic, Carestream Health, Koninklijke Philips, and Esaote-are implementing key strategies to strengthen their market presence. These include boosting R&D investments to fast-track innovation, collaborating with healthcare providers for real-time feedback, expanding into emerging markets, and leveraging AI and IoT to launch intelligent diagnostic and remote care platforms.