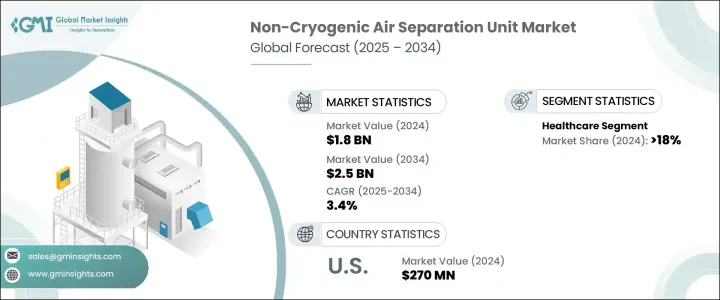

세계의 비냉매 공기분리장치 시장은 2024년에는 18억 달러로 평가되었고, CAGR 3.4%로 성장할 전망이며, 2034년에는 25억 달러에 이를 것으로 예측됩니다.

공공 부문의 이니셔티브 및 유리한 정책 프레임 워크의 지원이 증가함에 따라 산업계 전체의 비냉매 공기분리 시스템에 대한 수요가 부각되고 있습니다. 이러한 시스템은, 환경 컴플라이언스 목표를 달성하기 위해서 뿐만 아니라, 보다 광범위한 지속 가능성 목표 및 CSR 주도의 과제에 따르기 위해서도, 산업 사업자에 의해서 넓게 채용되고 있습니다. 보다 많은 기업이 탈탄소화 및 배출 삭감에 임하는 가운데, 극저온 처리에 의지하지 않고 에너지 효율을 제공하는 공기분리 시스템은, 전적으로 선호되게 되고 있습니다.

세계의 환경 규제 및 저탄소 기술 추진으로 화학, 헬스케어, 철강, 에너지 등의 분야에서 이러한 시스템의 가치가 크게 높아지고 있습니다. 조직은 기존의 극저온 플랜트와 관련된 운용의 복잡성과 비용 부담을 줄이면서 보다 깨끗한 운용을 실현하기 위해 비극저온 기술을 채용하고 있습니다. 국제적인 환경 협정과 지역의 녹색 정책에 뒷받침된 규제의 기세는 신흥 시장과 성숙 시장으로부터의 자발적인 수요를 계속 만들어 내고 있습니다. 소규모 모듈식 유닛에서 고급 PSA 시스템에 이르기까지 비저온 셋업의 유연성은 청정 에너지와 지역화된 공업 생산에 대한 변화하는 수요에 부합합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 18억 달러 |

| 예측 금액 | 25억 달러 |

| CAGR | 3.4% |

가스 유형별로는 질소가 계속해서 비냉매 공기분리장치의 성장을 견인하고 있습니다. 특히 식음료, 전자기기, 의약품 등 다양한 산업에서 널리 사용되고 있기 때문에 생산 및 포장 작업에 필수적입니다. 이 수요의 가장 큰 요인 중 하나는 식품 가공 분야의 가스 치환 포장(MAP)에 대한 의존도가 높아지는 것입니다. 식품 용도 이외에도 산화 제어 및 오염 방지가 중요한 반도체 제조나 의약품 제조 등 섬세한 제조 공정으로 불활성 환경을 만들어 내기 위해서도 질소는 필수입니다.

헬스케어 산업은 2024년에 18%의 점유율을 차지했는데, 이는 현장에서의 산소 제조 기술의 이용 증가를 반영하고 있습니다. 최종 사용자 측면에서는 석유 및 가스, 철강, 화학 등의 분야가 핵심 업무로 산소와 질소에 의존하고 있습니다. 특히 제철에서 산소는 용광로의 성능을 향상시키고 아르곤은 불순물 제거를 확실하게 합니다. 산소 부화 연소를 위한 현장 시스템의 채택은 산업의 탈탄소화 전략과 함께 증가하고 있습니다. 헬스케어에서는 포터블 PSA 유닛을 통해 제조되는 의료 등급의 산소 수요가 특히 원격지나 서비스가 부족한 지역에서 급증하고 있습니다.

미국의 비냉매 공기분리장치 시장은 2024년에 2억 7,000만 달러에 이르렀으며, 규제 강화와 인프라 투자에 의해 지원되고 있습니다. 수소 개발 및 암모니아 생산에 대한 자금 공급이 비저온 산소 및 질소 장치에 대한 왕성한 수요를 낳고 있습니다. 파이프라인의 안전성에 관한 규제 조치도 셰일 지역 전체에서 질소 생성 장치의 설치 대수를 늘리는 요인이 되고 있습니다. 이러한 동향은, 산업 가스 및 인프라의 근대화 노력과 함께, 미국 시장의 장기적 성장을 계속 형성하고 있습니다.

세계의 비냉매 공기분리장치 산업에서 활약하는 주요 기업은 Messer, AIR WATER INC, Enerflex Ltd., Technex, Yingde Gases, Ranch Cryogenics Inc., AMCS Corporation, Taiyo Nippon Sanso Corporation, Air Products and Chemicals Inc., KaiFeng Air Separation Group Co. LTD., CRYOTEC Anlagenbau GmbH, Air Liquide, Universal Industrial Gases Inc., Linde plc, Sichuan Air Separation Plant Group 및 Praxair Technology Inc. 등이 있습니다. 경쟁력을 유지하기 위해 대기업은 IoT 기반 자동화와 디지털 모니터링 솔루션을 통합하면서 모듈형 제품 포트폴리오 확대에 주력하고 있습니다. 각 회사는 에너지, 헬스케어, 산업가스 판매자와 전략적 파트너십을 맺고 지역 발자국을 강화하고 있습니다. 또한 연구개발의 핵심은 시스템 에너지 효율 향상, 가스 순도 수준 개선, 분산형 및 모바일형 이용 사례에 대응하는 PSA 기반 소형 모델의 개발입니다. 이러한 전략은 공급업체가 청정 에너지 전환을 위한 포지셔닝을 취하면서 증가하는 시장 수요에 대응하는 데 도움이 됩니다.

The Global Non-Cryogenic Air Separation Unit Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 3.4% to reach USD 2.5 billion by 2034. Growing support from public sector initiatives and favorable policy frameworks fuel the demand for non-cryogenic air-separation systems across industries. These systems are being widely adopted by industrial operators not only to meet environmental compliance targets but also to align with broader sustainability goals and CSR-driven agendas. As more corporations commit to decarbonization and emission reduction, air separation systems that offer energy efficiency without relying on cryogenic processing are gaining preference across the board.

Environmental regulations and the global push for low-carbon technologies have significantly elevated the value of these systems in sectors such as chemicals, healthcare, steel, and energy. Organizations are embracing non-cryogenic technologies to achieve cleaner operations while reducing operational complexities and cost burdens associated with traditional cryogenic plants. Regulatory momentum driven by international environmental agreements and local green policies continues generating voluntary demand from emerging and mature markets. From smaller-scale modular units to advanced PSA systems, the flexibility of non-cryogenic setups aligns with the shifting demands for clean energy and localized industrial production.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $2.5 Billion |

| CAGR | 3.4% |

Based on gas type, nitrogen continues to be the primary driver for the growth of non-cryogenic air separation units. Its widespread use across multiple industries-especially food and beverage, electronics, and pharmaceuticals-has made it essential in production and packaging operations. One of the most significant contributors to this demand is the increasing reliance on modified atmosphere packaging (MAP) within the food processing sector. Beyond food applications, nitrogen is also crucial for creating inert environments in sensitive manufacturing processes, such as in semiconductor fabrication and pharmaceutical production, where oxidation control and contamination prevention are critical.

The healthcare industry accounted for an 18% share in 2024, reflecting increased usage of on-site oxygen production technologies. On the end-user front, sectors such as oil & gas, iron & steel, and chemicals rely on oxygen and nitrogen in their core operations. Particularly in steelmaking, oxygen improves furnace performance while argon ensures the removal of impurities. The adoption of on-site systems for oxygen-enriched combustion is rising with industrial decarbonization strategies. In healthcare, demand for medical-grade oxygen produced via portable PSA units is surging, especially in remote and underserved areas.

U.S. Non-Cryogenic Air Separation Unit Market reached USD 270 million in 2024, supported by regulatory mandates and infrastructure investments. Funding for hydrogen development and ammonia production is creating robust demand for non-cryogenic oxygen and nitrogen units. Regulatory actions concerning pipeline safety are also contributing to higher installations of nitrogen generation units across shale regions. These trends, along with modernization efforts in industrial gas infrastructure, continue to shape long-term growth in the U.S. market.

Major companies active in the Global Non-Cryogenic Air Separation Unit Industry include Messer, AIR WATER INC, Enerflex Ltd., Technex, Yingde Gases, Ranch Cryogenics, Inc., AMCS Corporation, Taiyo Nippon Sanso Corporation, Air Products and Chemicals, Inc., KaiFeng Air Separation Group Co., LTD., CRYOTEC Anlagenbau GmbH, Air Liquide, Universal Industrial Gases, Inc., Linde plc, Sichuan Air Separation Plant Group, and Praxair Technology, Inc. To remain competitive, leading players focus on expanding their modular product portfolios while integrating IoT-based automation and digital monitoring solutions. Companies are entering strategic partnerships with energy, healthcare, and industrial gas distributors to strengthen their regional footprints. Additionally, R&D is centered on boosting system energy efficiency, improving gas purity levels, and developing compact PSA-based models for decentralized and mobile use cases. These tactics are helping suppliers meet rising market demand while positioning themselves for the clean energy transition.