세계의 항공기 유압 시스템 시장은 2024년에는 122억 달러로 평가되었으며, 2034년에는 360억 달러에 이를 것으로 추정되며, CAGR 11.5%로 성장할 전망입니다.

이러한 성장은 항공 여행에 대한 전 세계적인 수요 증가와 상업용, 군용, 무인 항공기 플랫폼 전반에 걸친 유압 시스템의 통합 증가에 힘입은 바가 큽니다. 항공사가 항공기를 업그레이드하고 정부가 방위 역량을 강화함에 따라 유압 시스템은 운영 효율성, 신뢰성 및 안전성을 보장하는 데 매우 중요해졌습니다. 전 세계 항공 여객 수송량이 지속적으로 증가함에 따라 항공우주 기업들은 더욱 정교한 항공기에 투자해야 한다는 압박을 받고 있으며, 이에 따라 첨단 유압 작동 시스템의 필요성이 커지고 있습니다. 이러한 시스템은 기동, 비행 제어, 제동, 랜딩 기어 작동 등 다양한 항공기 기능에 필수적입니다.

최근 몇 년간 관세 도입을 비롯한 지정학적 무역 긴장으로 인해 특히 해외에서 조달하는 항공우주 부품의 공급망에 상당한 혼란이 발생했습니다. 이러한 변화로 인해 제조업체와 공급업체는 다각화된 소싱 전략, 현지 생산, 조달 모델의 재평가를 통해 비용 변동과 지연을 완화하기 위해 적응해야 했습니다. 그 결과, 현지화되고 탄력적인 공급망으로의 전환이 시장 환경을 형성하는 중요한 트렌드가 되고 있습니다. 기술 측면에서는 마이크로 및 전자 유압 시스템의 사용 증가로 인해 시장이 강력한 모멘텀을 경험하고 있습니다. 이러한 혁신은 드론, 자율 항공기, 도심 항공 모빌리티 차량과 같은 새로운 용도에서 컴팩트하고 에너지 효율적인 솔루션에 대한 수요 증가에 부응하고 있습니다. 또한 스텔스, 무기 취급, 향상된 제어 메커니즘과 같은 첨단 항공기 기능을 지원하는 고성능 유압 시스템에 대한 국방 투자로 인해 수요가 계속 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 122억 달러 |

| 예측 금액 | 360억 달러 |

| CAGR | 11.5% |

플랫폼 측면에서 시장은 회전익, 고정익, 무인 항공기(UAV)로 세분화됩니다. 고정익 카테고리는 2024년 72억 달러의 가치로 시장을 주도했습니다. 이 부문의 성장은 차세대 상업용 및 방위용 항공기의 조달 증가와 기존 항공기의 지속적인 업그레이드에 힘입은 것입니다. 항공 교통량이 증가하고 군 예산이 확대되면서 비행 제어, 제동 및 기어 배치와 같은 작업을 위해 복잡한 유압 하위 시스템이 필요한 기술적으로 진보된 제트기의 도입이 촉진되고 있습니다.

컴포넌트별로 시장은 저장소, 펌프, 어큐뮬레이터, 액추에이터, 유압 퓨즈, 밸브 등으로 나뉩니다. 액추에이터는 2024년에 35억 달러의 수익을 창출하며 가장 실적이 좋은 부문으로 부상했습니다. 비행 제어 시스템의 정확성과 신뢰성에 대한 요구가 높아짐에 따라 작고 연료 효율적이며 고성능 출력이 가능한 차세대 액추에이터에 대한 수요가 증가하고 있습니다. 최신 항공기가 무게 감소와 제어 응답성 향상에 중점을 두면서 제조업체는 진화하는 요구 사항을 충족하기 위해 전자 유압식 액추에이터 기술에 점점 더 많은 투자를 하고 있습니다.

용도별로 시장은 비행 제어 시스템, 추력 반전 시스템, 착륙 및 제동 시스템 및 기타 기능으로 나뉩니다. 착륙 및 제동 시스템 부문은 2024년 52억 달러로 가장 높은 기여를 할 것으로 예상됩니다. 이러한 시스템은 특히 항공기의 이착륙이 잦은 지역에서 항공기의 안전한 운항에 필수적입니다. 미끄럼 방지 기능, 향상된 압력 관리, 내장형 리던던시 등의 기능을 갖춘 고급 유압 부품을 요구하는 엄격한 안전 규정이 수요를 더욱 뒷받침하고 있습니다.

지역별로는 미국이 항공기 유압 시스템 시장에서 가장 큰 점유율을 차지하고 있으며(2024년)에는 38억 달러를 차지했습니다. 미국 시장의 우위는 방위 프로그램, 상업용 항공 업그레이드, 항공우주 기술 전반에 걸친 R&D 노력에 대한 투자 증가에 기인합니다. 또한 미국은 유압 시스템 기술을 지속적으로 발전시키고 있는 주요 항공우주 제조업체 및 공급업체의 존재로 인해 이점을 누리고 있습니다. 이러한 기업들은 경량 구조, 전기-유압 통합, 전기 항공기(MEA) 노력에 부합하는 시스템에 중점을 두고 있습니다.

시장 경쟁은 여전히 치열하며, 기존 다국적 기업과 혁신적인 스타트업 모두 점유율을 놓고 경쟁하고 있습니다. 주요 업체들은 스마트 유압 기술, 통합 진단, 전기 및 하이브리드 플랫폼용으로 설계된 솔루션에 적극적으로 집중하고 있습니다. 연료 효율성과 환경 성능을 향상시키면서 FAA, EASA, AS9100과 같은 글로벌 안전 표준을 충족하는 유압 시스템 개발로 눈에 띄는 전환이 이루어지고 있습니다.

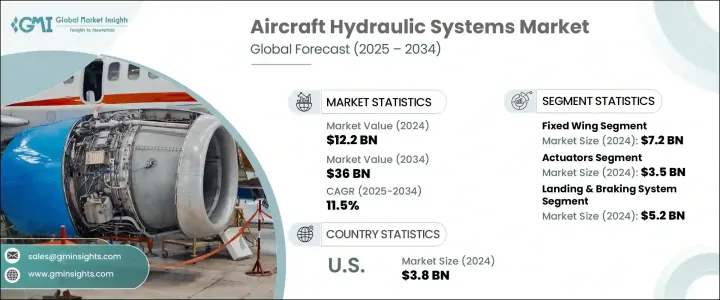

The Global Aircraft Hydraulic Systems Market was valued at USD 12.2 billion in 2024 and is estimated to grow at a CAGR of 11.5% to reach USD 36 billion by 2034. This growth is largely driven by the increasing global demand for air travel and the rising integration of hydraulic systems across commercial, military, and unmanned aerial vehicle platforms. As airlines upgrade fleets and governments ramp up defense capabilities, hydraulic systems have become critical for ensuring operational efficiency, reliability, and safety. The continued rise in global air passenger traffic is putting pressure on aerospace companies to invest in more sophisticated aircraft, which in turn is driving the need for advanced hydraulic actuation systems. These systems are essential for various aircraft functions, including maneuvering, flight control, braking, and landing gear operation.

Geopolitical trade tensions in recent years, including the introduction of tariffs, have caused significant disruption in the supply chain, particularly for aerospace components sourced from overseas. These changes forced manufacturers and suppliers to adapt through diversified sourcing strategies, local production, and reevaluation of procurement models to mitigate cost fluctuations and delays. As a result, the shift toward localized and resilient supply chains is becoming a crucial trend shaping the market landscape. On the technology front, the market is experiencing strong momentum due to the rising use of micro and electro-hydraulic systems. These innovations cater to the growing need for compact and energy-efficient solutions in emerging applications such as drones, autonomous aircraft, and urban air mobility vehicles. Moreover, defense investments continue to boost the demand for high-performance hydraulic systems that support advanced aircraft functionalities like stealth, weapons handling, and enhanced control mechanisms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.2 Billion |

| Forecast Value | $36 Billion |

| CAGR | 11.5% |

In terms of platform, the market is segmented into rotary wing, fixed wing, and unmanned aerial vehicles (UAVs). The fixed wing category led the market in 2024 with a valuation of USD 7.2 billion. The growth of this segment is fueled by an increase in procurement of new-generation commercial and defense aircraft as well as ongoing upgrades to existing fleets. Rising air traffic and expanded military budgets are encouraging the adoption of technologically advanced jets that require complex hydraulic subsystems for tasks such as flight control, braking, and gear deployment.

By component, the market is divided into reservoirs, pumps, accumulators, actuators, hydraulic fuses, valves, and others. Actuators emerged as the top-performing segment in 2024, generating USD 3.5 billion in revenue. The heightened need for accuracy and reliability in flight control systems is spurring demand for next-generation actuators that are compact, fuel-efficient, and capable of high-performance output. As modern aircraft focus on weight reduction and improved control responsiveness, manufacturers are increasingly investing in electro-hydraulic actuator technologies to meet evolving requirements.

On the basis of application, the market includes flight control systems, thrust reversal systems, landing and braking systems, and other functions. The landing and braking systems segment was the highest contributor in 2024, valued at USD 5.2 billion. These systems are essential for the safe operation of aircraft, especially in regions where aircraft perform frequent takeoffs and landings. Demand is further supported by stricter safety regulations, which require more advanced hydraulic components with features like anti-skid capabilities, improved pressure management, and built-in redundancies.

Regionally, the United States held the largest share of the aircraft hydraulic systems market, accounting for USD 3.8 billion in 2024. The dominance of the US market can be attributed to rising investments in defense programs, commercial aviation upgrades, and R&D efforts across aerospace technologies. The country also benefits from the presence of major aerospace manufacturers and suppliers who are consistently advancing hydraulic system technologies. These companies are placing emphasis on lightweight construction, electro-hydraulic integrations, and systems that align with More Electric Aircraft (MEA) initiatives.

Market competition remains intense, with both established multinational companies and innovative startups competing for share. Leading players are actively focusing on smart hydraulic technologies, integrated diagnostics, and solutions designed for electric and hybrid platforms. There is a noticeable shift toward developing hydraulic systems that offer enhanced fuel efficiency and environmental performance while meeting global safety standards such as FAA, EASA, and AS9100.