사파이어 코팅 광학 장비 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Sapphire-coated optics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1740856

리서치사:Global Market Insights Inc.

발행일:2025년 04월

페이지 정보:영문 220 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

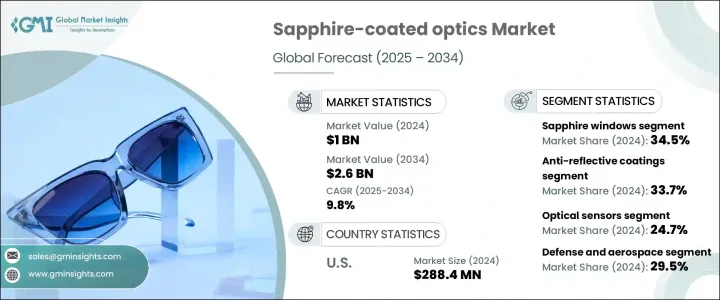

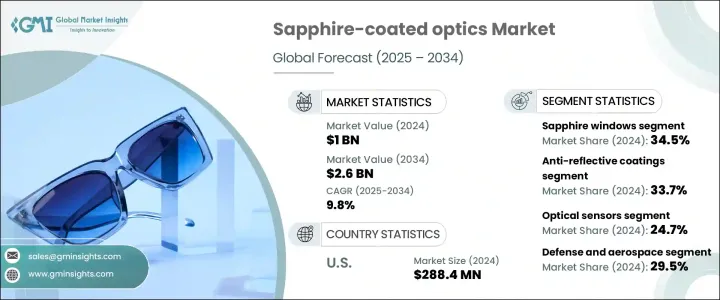

세계의 사파이어 코팅 광학 장비 시장 규모는 2024년 10억 달러였고, CAGR 9.8%로 성장하여 2034년까지 26억 달러에 이를 것으로 예측되고 있습니다. 이 시장은 항공우주, 방위, 의료기기, 산업기계, 일렉트로닉스 등의 용도가 확대되고 있기 때문에 기세가 늘고 있습니다. 특히 가혹한 환경에서 고성능 광학 솔루션에 대한 요구가 증가함에 따라 사파이어 코팅 수요에 박차를 가하고 있습니다. 각 분야의 장치가 더욱 발전함에 따라 제조업체는 탁월한 내구성, 열 안정성 및 투명성을 갖춘 사파이어 코팅 광학에 주목하고 있습니다. 차세대 기술의 채택과 스마트 장치의 보급은 신뢰할 수 있는 광학 부품의 필요성을 증가시키고 있습니다. 이러한 코팅은 내상성과 기계적 강도가 특히 요구되며 정확성과 신뢰성이 중요한 응용 분야에 이상적입니다.

스마트폰의 세계 출하 대수가 급증하고 2024년에는 12억 4,000만대에 이르기 때문에 내구성이 높고, 고클라리티의 광학 부품에 대한 수요가 대폭 증가하고 있습니다. 모바일 장치의 카메라 시스템이 진화함에 따라 제조업체는 뛰어난 화질과 성능 요구를 충족시키기 위해 사파이어 코팅 광학을 채택하고 있습니다. 한편, 의료기기 및 산업기기로의 고선명도 광학 통합은 시장 전망을 더욱 강화하고 있습니다. 사파이어 코팅은 광학 성능을 향상시키고 높은 스트레스 조건을 견딜 수 있기 때문에 다양한 산업 분야에서 중요한 용도로 선정되었습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

10억 달러

예측 금액

26억 달러

CAGR

9.8%

제품 유형별로 보면, 시장은 사파이어 윈도우, 렌즈, 볼 렌즈, 프리즘, 파장판, 기타로 분류됩니다. 사파이어 렌즈와 볼 렌즈는 정밀 이미지 프로세싱과 레이저 시스템에서 사용되며, 파장 판과 프리즘은 여러 분야에서 고급 광학 어셈블리에 채택되었습니다.

코팅 유형에 따라 시장은 높은 반사율 코팅, 반사 방지 코팅, 특수 코팅 부품, 필터 코팅으로 구분됩니다. 고반사율 코팅은 주로 레이저 용도로 사용되어 필터 코팅은 바이오메디컬 이미징이나 센서 베이스 시스템의 요구에 대응하고 있습니다. 광학 기능의 복잡화에 의해 독자적인 운용 요건에 맞춘 특수 코팅의 성장이 촉진되고 있습니다.

시장은 더욱 용도별로 분류되어 광 센서, 이미징 시스템, 적외 광학, 분광, 레이저 시스템 등이 포함되어 있습니다. 사파이어 코팅된 부품은 가혹한 조건 하에서도 확실하게 동작하기 때문에 이러한 수요가 높은 용도에서는 불가결해지고 있습니다.

최종 용도별로는 방위 및 항공우주, 의료 및 헬스케어, 공업제조, 반도체 및 일렉트로닉스, 컨슈머 일렉트로닉스, 석유 및 가스, 연구개발, 기타가 포함됩니다. 이러한 광학 장비는 극한 상태에서 동작하는 미션 크리티컬한 장치에 필요한 구조적 무결성과 성능을 제공합니다. 석유 및 가스 산업은 산업용 제조업과 함께, 가혹한 환경하에서 신뢰성이 높은 성능을 발휘하는 사파이어 코팅 광학의 가치를 인정하고 있습니다.

미국은 세계 시장에서 압도적인 지위를 차지하고 85% 이상의 점유율을 획득했으며, 2024년에는 2억 8,840만 달러에 이르렀습니다. 혁신에 대한 일관된 투자에 힘입어 정부의 지원 이니셔티브는 사파이어 광학의 확대를 지원하고 있으며, 국가 전체에서 대규모 생산과 지속적인 기술 개발을 장려하고 있습니다.

사파이어 코팅 광학 장비 시장에서 사업을 전개하는 주요 기업은 Coherent, COE Optics, Newport, Meller Optics, Knight Optical 등이 포함되어 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

밸류체인 분석

원재료 공급자

크리스탈 제조업체

광학부품 제조업자

코팅 서비스 제공업체

시스템 통합자

최종 용도

가격 분석과 비용 구조

제품 유형별 가격 분석

지역별 가격 분석

가격 동향, 2020-2025년

가격 예측, 2025-2033년

가격에 영향을 미치는 요인

원재료비

제조의 복잡성

코팅 기술

품질 요건

비용 구조 분석

원재료비

인건비

제조 간접비

연구개발비

유통 및 마케팅 비용

이익률 분석

트럼프 정권의 관세 영향 - 구조화된 개요

무역에 미치는 영향

무역량의 혼란

보복 조치

업계에 미치는 영향

공급측의 영향(원재료)

주요 원재료의 가격 변동

공급망 재구성

생산 비용에 미치는 영향

수요측의 영향(판매가격)

최종 시장에의 가격 전달

시장 점유율 동향

소비자의 반응 패턴

영향을 받는 주요 기업

전략적인 업계 대응

공급망 재구성

가격 설정 및 제품 전략

정책관여

전망과 향후 검토 사항

무역 통계(HS코드)

주요 수출국

주요 수입국

참고: 위의 무역 통계는 주요 국가에 대해서만 제공됩니다.

이익률 분석

주요 뉴스와 대처

규제 상황

시장 역학

시장 성장 촉진요인

내구성이 있는 광학 부품 수요 증가

가혹한 환경에서의 용도 증가

방위 및 항공우주 분야에서의 채용 증가

코팅 기술의 기술적 진보

시장 성장 억제요인

높은 생산 비용

복잡한 제조 공정

대체 재료와의 경쟁

시장 기회

의료기기에서 새로운 용도

가전제품 수요 증가

신흥 경제 국가의 확대

코팅에서 나노기술 진보

시장의 과제

대형 부품의 생산 규모 확대

코팅에 의한 광학 성능 유지

공급망의 취약성

성장 가능성 분석

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

제5장 재료 특성과 특징

사파이어의 물리적 특성

열특성

광전송 범위

내약품성

대체 재료와의 비교

사파이어 vs. 유리

사파이어 vs. 퓨즈드 실리카

사파이어 vs. 다른 결정 재료의 비교

결정 방위와 성능에 대한 영향

C플레인

R플레인

A플레인

M플레인

품질 파라미터 및 기준

제6장 코팅 기술과 공정

반사 방지(AR) 코팅

단층 코팅

다층 코팅

광대역 AR 코팅

고반사 코팅

필터 코팅

특수 코팅

소수성 코팅

흠집 방지 코팅

전도성 코팅

코팅 증착 기술

물리 증착(PVD)

화학 증착(CVD)

이온 어시스트 퇴적

플라즈마 강화 증착

마그네트론 스퍼터링

품질관리 및 시험방법

제7장 제조 공정과 밸류체인 분석

사파이어 결정의 성장 방법

초크랄스키(CZ)법

열교환기 방식(HEM)

키로플러스(KY)법

엣지 정의 필름 공급 성장(EFG)

가공 및 제조

절단 및 성형

연삭 및 랩핑

연마 기술

표면 품질 요건

코팅 도포 공정

품질 보증 및 테스트

제8장 기술 혁신과 연구개발 활동

최근 기술의 진보

고급 코팅 기술

나노층 코팅

제조 공정 개선

특허 분석

특허출원 동향

주요 특허 보유자

신흥기술

R&D 투자 분석

산학 제휴

기술 로드맵

제9장 규제 프레임워크과 기준

광학부품의 국제규격

품질인증 요건

업계 고유의 규제

방위 및 항공우주 규격

의료기기 규제

소비자용 전자기기의 규격

수출관리와 무역규제

제조업에 영향을 주는 환경규제

컴플라이언스 문제와 해결책

제10장 미래 동향과 새로운 용도

기술 동향

초박형 사파이어 코팅

다기능 코팅

셀프 클리닝 표면

새로운 용도

증강현실(AR) 및 가상현실(VR)

자율주행차

고급 의료 이미지

양자 컴퓨팅

우주 탐사

시장의 혼란과 게임 체인저

장기적인 시장 전망-2033년 이후

제11장 시장 추계 및 예측 : 제품 유형별, 2021-2034년

주요 동향

사파이어 창

사파이어 렌즈

사파이어 볼 렌즈

사파이어 파장판

사파이어 프리즘

기타

제12장 시장 추계 및 예측 : 코팅 유형별, 2021-2034년

주요 동향

반사 방지 코팅

고반사 코팅

필터 코팅

특수 코팅

미코팅 부품

제13장 시장 추계 및 예측 : 용도별, 2021-2034년

주요 동향

광학 센서

레이저 시스템

이미지 시스템

분광법

적외선 광학

기타

제14장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

주요 동향

방위 및 항공우주

군사 광학 기기

감시 시스템

항공기 및 우주선 부품

의료 및 헬스케어

수술용 레이저

진단 기기

내시경 검사

공업제조업

고출력 레이저

프로세스 모니터링

품질 관리 시스템

반도체 및 일렉트로닉스

리소그래피

검사 시스템

웨이퍼 처리

소비자 일렉트로닉스

스마트폰 부품

카메라 렌즈

웨어러블 디바이스

석유 및 가스

연구개발

기타

제15장 시장 추계 및 예측 : 지역별, 2021-2034년

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

인도

일본

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

제16장 기업 프로파일

Asphera, Inc.

COE Optics

Coherent

Creator Optics

Esco Optics, Inc.

Firebird Optics

Gavish

Guild Optical Associates.

Hyperion Optics

Knight Optical

Kyocera Corporation

Meller Optics

Newport

Noni Custom Optics

Precision Glass & Optics(PG&O)

Saint-Gobain

Shanghai Optics

UQG Optics

JHS

영문 목차

영문목차

The Global Sapphire-coated Optics Market was valued at USD 1 billion in 2024 and is projected to grow at a CAGR of 9.8% to reach USD 2.6 billion by 2034. The market is gaining momentum due to its expanding applications across aerospace, defense, medical devices, industrial machinery, and electronics. The increasing need for high-performance optical solutions, especially in harsh environments, is fueling the demand for sapphire coatings. As devices across sectors become more advanced, manufacturers are turning to sapphire-coated optics for their unmatched durability, thermal stability, and clarity. The growing adoption of next-generation technologies and the proliferation of smart devices continue to elevate the need for reliable optical components. These coatings are particularly sought-after for their scratch resistance and mechanical strength, making them ideal for applications where precision and reliability are critical.

The surge in global smartphone shipments, which reached 1.24 billion units in 2024, has driven a significant increase in the demand for durable, high-clarity optics. As camera systems in mobile devices evolve, manufacturers are embracing sapphire-coated optics to meet the need for superior image quality and performance. Meanwhile, the integration of high-clarity optics into medical and industrial equipment has further strengthened market prospects. The ability of sapphire coatings to enhance optical performance and withstand high-stress conditions makes them a favored choice for critical applications in diverse industries.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$1 Billion

Forecast Value

$2.6 Billion

CAGR

9.8%

In terms of product type, the market is categorized into sapphire windows, lenses, ball lenses, prisms, waveplates, and others. Among these, sapphire windows held the largest share at 34.5% in 2024, due to their exceptional resistance to scratches and their high mechanical and thermal performance. These windows are used extensively in mission-critical systems requiring long-term durability and stable optical transmission. Sapphire lenses and ball lenses are also gaining traction for use in precision imaging and laser systems, while waveplates and prisms are being adopted in advanced optical assemblies across several sectors. The overall product diversification reflects the rising customization and functionality demanded by end users.

By coating type, the market is segmented into high-reflectivity coatings, anti-reflective coatings, specialized coatings, uncoated components, and filter coatings. Anti-reflective coatings led the segment with a 33.7% share in 2024. These coatings enhance light transmission and reduce glare, making them essential in optical systems where high clarity is required. Their widespread usage in high-resolution imaging and advanced electronic systems continues to drive this segment forward. High-reflectivity coatings are primarily used in laser applications, while filter coatings serve the needs of biomedical imaging and sensor-based systems. The increasing complexity of optical functions is promoting the growth of specialized coatings tailored for unique operational requirements.

The market is further segmented by application, including optical sensors, imaging systems, infrared optics, spectroscopy, laser systems, and others. Optical sensors accounted for the largest portion, with a 24.7% share in 2024. These sensors rely on sapphire coatings for their robustness and precision, particularly in industrial automation, environmental monitoring, and diagnostics. The ability of sapphire-coated components to perform reliably under extreme conditions has made them essential in these high-demand applications. Other growing applications include spectroscopy and imaging systems, where the anti-abrasive and chemically resistant nature of sapphire is crucial. The laser systems and infrared optics segments are also expanding due to rising technological requirements in both commercial and military systems.

By end-use, the sapphire-coated optics market includes defense and aerospace, medical and healthcare, industrial manufacturing, semiconductor and electronics, consumer electronics, oil and gas, research and development, and others. Defense and aerospace dominated the market with a 29.5% share in 2024. The need for scratch-resistant, thermally stable optical components in defense and space missions is driving continuous demand. These optics offer the structural integrity and performance required for mission-critical equipment operating in extreme conditions. The medical sector is increasingly deploying sapphire optics in diagnostic and surgical equipment, while the semiconductor and electronics industries benefit from sapphire's precision in wafer inspection tools. The oil and gas industry, along with industrial manufacturing, is recognizing the value of sapphire-coated optics for reliable performance in rugged environments.

The United States held the dominant position in the global market, capturing over 85% share and reaching USD 288.4 million in 2024. This leadership is backed by advanced optical manufacturing infrastructure and consistent investment in defense and aerospace innovation. Government-backed initiatives continue to support the expansion of sapphire optics, encouraging large-scale production and sustained technological development across the country.

Key players operating in the sapphire-coated optics market include Coherent, COE Optics, Newport, Meller Optics, and Knight Optical. These companies are recognized for offering high-precision sapphire optics tailored for demanding industrial and scientific applications. Their innovations and product development strategies are instrumental in shaping the future of this fast-evolving market.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope & definition

1.2 Base estimates & calculations

1.3 Forecast calculation

1.4 Data sources

1.4.1 Primary

1.4.2 Secondary

1.4.2.1 Paid sources

1.4.2.2 Public sources

1.5 Primary research and validation

1.5.1 Primary sources

1.5.2 Data mining sources

Chapter 2 Executive Summary

2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

3.1 Value chain analysis

3.1.1 Raw material suppliers

3.1.2 Crystal manufacturers

3.1.3 Optical component fabricators

3.1.4 Coating service providers

3.1.5 System integrators

3.1.6 End use

3.2 Pricing analysis and cost structure

3.2.1 Price point analysis by product type

3.2.2 Price point analysis by region

3.2.3 Price trends 2020 - 2025)

3.2.4 Price forecast 2025 - 2033

3.2.5 Factors affecting pricing

3.2.5.1 Raw material costs

3.2.5.2 Manufacturing complexity

3.2.5.3 Coating technology

3.2.5.4 Quality requirements

3.2.6 Cost structure analysis

3.2.6.1 Raw material cost

3.2.6.2 Labor cost

3.2.6.3 Manufacturing overhead

3.2.6.4 R&D expenses

3.2.6.5 Distribution and marketing costs

3.2.7 Profit margin analysis

3.3 Impact of trump administration tariffs – structured overview

3.3.1 Impact on trade

3.3.1.1 Trade volume disruptions

3.3.1.2 Retaliatory measures

3.3.2 Impact on the industry

3.3.2.1.1 Supply-side impact (raw materials)

3.3.2.1.2 Price volatility in key materials

3.3.2.1.3 Supply chain restructuring

3.3.2.1.4 Production cost implications

3.3.2.2 Demand-side impact (selling price)

3.3.2.2.1 Price transmission to end markets

3.3.2.2.2 Market share dynamics

3.3.2.2.3 Consumer response patterns

3.3.3 Key companies impacted

3.3.4 Strategic industry responses

3.3.4.1 Supply chain reconfiguration

3.3.4.2 Pricing and product strategies

3.3.4.3 Policy engagement

3.3.5 Outlook and future considerations

3.4 Trade statistics (HS code)

3.4.1 Major exporting countries

3.4.2 Major importing countries

Note: the above trade statistics will be provided for key countries only.

3.5 Profit margin analysis

3.6 Key news & initiatives

3.7 Regulatory landscape

3.8 Market dynamics

3.8.1 Market drivers

3.8.1.1 Growing demand for durable optical components

3.8.1.2 Increasing applications in harsh environments

3.8.1.3 Rising adoption in defense and aerospace

3.8.1.4 Technological advancements in coating techniques

3.8.2 Market restraints

3.8.2.1 High production costs

3.8.2.2 Complex manufacturing process

3.8.2.3 Competition from alternative materials

3.8.3 Market opportunities

3.8.3.1 Emerging applications in medical devices

3.8.3.2 Growing demand in consumer electronics

3.8.3.3 Expansion in developing economies

3.8.3.4 Advancements in nanotechnology for coatings

3.8.4 Market challenges

3.8.4.1 Scaling production for large components

3.8.4.2 Maintaining optical performance with coatings

3.8.4.3 Supply chain vulnerabilities

3.9 Growth potential analysis

3.10 Porter's analysis

3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.3 Competitive positioning matrix

4.4 Strategic outlook matrix

Chapter 5 Material Properties and Characteristics

5.1 Physical properties of sapphire

5.1.1 Thermal properties

5.1.2 Optical transmission range

5.1.3 Chemical resistance

5.2 Comparison with alternative materials

5.2.1 Sapphire vs. Glass

5.2.2 Sapphire vs. Fused silica

5.2.3 Sapphire vs. Other crystalline materials

5.3 Crystal orientation and its impact on performance

5.3.1 C-Plane

5.3.2 R-Plane

5.3.3 A-Plane

5.3.4 M-Plane

5.4 Quality parameters and standards

Chapter 6 Coating Technologies and Processes

6.1 Anti-reflective (AR) coatings

6.1.1 Single-layer coatings

6.1.2 Multi-layer coatings

6.1.3 Broadband AR coatings

6.2 High-reflectivity coatings

6.3 Filter coatings

6.4 Specialized coatings

6.4.1 Hydrophobic coatings

6.4.2 Scratch-resistant coatings

6.4.3 Conductive coatings

6.5 Coating deposition techniques

6.5.1 Physical vapor deposition (PVD)

6.5.2 Chemical vapor deposition (CVD)

6.5.3 Ion-assisted deposition

6.5.4 Plasma-enhanced deposition

6.5.5 Magnetron sputtering

6.6 Quality control and testing methods

Chapter 7 Manufacturing Processes and Value Chain Analysis

7.1 Sapphire crystal growth methods

7.1.1 Czochralski (CZ) method

7.1.2 Heat exchanger method (HEM)

7.1.3 Kyropoulos (KY) method

7.1.4 Edge-defined film-fed growth (EFG)

7.2 Processing and fabrication

7.2.1 Cutting and shaping

7.2.2 Grinding and lapping

7.2.3 Polishing techniques

7.2.4 Surface quality requirements

7.3 Coating application process

7.4 Quality assurance and testing

Chapter 8 Technological Innovations and R&D Activities

8.1 Recent technological advancements

8.1.1 Advanced coating techniques

8.1.2 Nanolayer coatings

8.1.3 Improved manufacturing processes

8.2 Patent analysis

8.2.1 Patent filing trends

8.2.2 Key patent holders

8.2.3 Emerging technologies

8.3 R&D investment analysis

8.4 Industry-academia collaborations

8.5 Technology roadmap

Chapter 9 Regulatory Framework and Standards

9.1 International standards for optical components