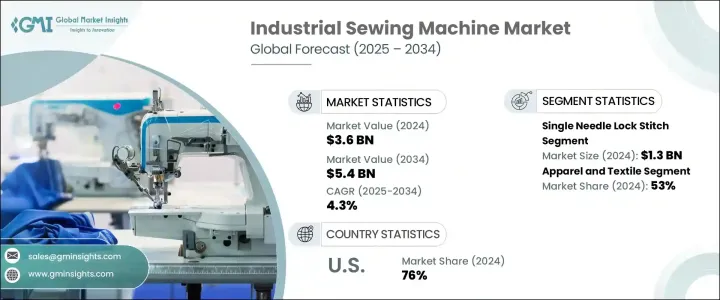

산업용 재봉틀 세계 시장 규모는 2024년에 36억 달러에 달했고, CAGR 4.3%로, 2034년에는 54억 달러에 이를 것으로 추정됩니다.

이 시장 확대는 인구 증가, 도시화, 소비자의 기호의 진화에 추진된 의류와 섬유 제품에 대한 세계 수요 증가가 주요 요인입니다. 산업용 재봉틀은 대량의 섬유 및 의류 생산을 지원하는 데 중요한 역할을 하므로 속도, 정밀도, 효율성을 목표로 하는 제조업체에 필수적입니다. 산업화를 추진하는 가운데, 보다 세련된 봉제 시스템에 대한 수요는 계속 확대되고 있습니다. 산업용 재봉틀은 현재 기본 기능에 그치지 않고 생산의 합리화, 다운타임의 삭감, 솔기의 균일성 향상을 지원하는 지능형 시스템을 탑재하도록 개발되고 있으며, 궁극적으로는 세계의 제조업자의 수익성을 높이고 있습니다.

시장 내에서는 다양한 용도에 대응하기 위해서, 재봉틀의 유형도 다양합니다. CAGR은 2034년까지 약 4.8%를 나타낼 전망입니다. 자동 스레드, 고급 모터 기능, 디지털 장력 제어와 같은 기능이 포함되어 작업을 간소화하고 작업자의 피로를 줄이면서 스티치 균일성을 보장합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 36억 달러 |

| 예측 금액 | 54억 달러 |

| CAGR | 4.3% |

산업용도의 관점에서 시장은 의류 섬유, 자동차, 가구, 의자, 가죽 제품, 기타 산업 분야로 나뉘어져 있습니다. 의류 및 섬유 부문은 2024년 전체 시장 점유율의 53% 이상을 차지하며 지배적인 위치를 차지했습니다. 이 부문은 속도와 정밀도로 여러 기능을 수행할 수 있는 고출력 기계에 대한 수요가 증가함에 따라 계속 성장하고 있습니다.

판매 채널의 경우 시장은 직접 판매와 간접 판매로 나뉘어져 있습니다. 장기적인 거래 관계를 구축하고, 반복 주문을 확보하고, 고객의 요구 사항을 보다 깊이 이해하는 데 도움이 되기 때문입니다.

그럼에도 불구하고 간접 판매 채널은 특히 중소 기업에 대한 접근 방식에서 시장 확대에 여전히 중요합니다. 온라인 플랫폼은 편리함, 가격 경쟁력, 다양한 기기에 쉽게 접근할 수 있는 편리함을 제공하며 유통 믹스의 중요한 부분이 되었습니다.

지역별로는 북미가 세계 시장 역학에서 중요한 역할을 하고 있으며, 2024년에는 미국이 이 지역시장의 약 76%를 차지해 7억 6,000만 달러에 육박하는 매출을 올립니다. 생산 요구가 증가함에 따라 이러한 우위에 기여하고 있습니다. 미국의 섬유 산업은 생산 재조달과 지속 가능한 관행의 도입에 주력하여 부활을 이루고 있습니다.

시장 경쟁은 완만하게 집중되어 있으며 주요 기업의 시장 점유율은 15-20%입니다.

The Global Industrial Sewing Machine Market was valued at USD 3.6 billion in 2024 and is estimated to grow at a CAGR of 4.3% to reach USD 5.4 billion by 2034. This expansion is largely driven by increasing global demand for apparel and textiles, propelled by population growth, urbanization, and evolving consumer preferences. Industrial sewing machines play a critical role in supporting high-volume textile and garment production, making them essential for manufacturers aiming for speed, precision, and efficiency. The integration of advanced technologies like robotics, IoT connectivity, and automation has significantly enhanced operational output, reduced labor dependency, and improved quality control in manufacturing environments. As businesses across emerging economies continue to industrialize, the demand for more sophisticated sewing systems continues to grow. Rapid shifts in fashion trends, the rise of fast fashion, and the need for scalable production have further intensified the need for advanced sewing equipment. Industrial sewing machines now go beyond basic functions and are developed to include intelligent systems that help streamline production, reduce downtime, and improve stitching consistency, ultimately boosting profitability for manufacturers globally.

Within the market, machine types vary to serve diverse applications. Key categories include double needle lock stitch, zigzag stitching, single needle lock stitch, overlock sewing, flatlock sewing, and other specialized systems. Among these, the single needle lock stitch segment led the category in 2024, contributing over USD 1.3 billion in revenue. Forecasts suggest this segment will witness a CAGR of around 4.8% through 2034. This machine type is particularly valued in garment manufacturing for its reliability and simplicity in performing straight-line stitching on lightweight and standard fabrics. Innovations in this segment now include features like automatic threading, advanced motor functions, and digital tension control, which simplify tasks and reduce fatigue for operators while ensuring stitch uniformity.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.6 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 4.3% |

From an industry application perspective, the market is divided into apparel and textiles, automotive, furniture and upholstery, leather goods, and other industrial sectors. The apparel and textile category held the dominant position in 2024, accounting for more than 53% of the total market share. This segment continues to grow as demand rises for high-output machines that can perform multiple functions with speed and precision. Enhanced features such as automatic thread trimming, programmable stitch patterns, and sensor-based adjustments are increasingly incorporated into machines serving this industry, leading to higher productivity and lower error margins.

Regarding sales channels, the market is split into direct and indirect sales. In 2024, direct sales led the distribution landscape, fueled by the growing need for tailor-made solutions and comprehensive after-sales services. Manufacturers prefer this channel as it helps in forging long-lasting business relationships, ensuring repeat orders, and enabling a deeper understanding of client requirements. Through direct engagement, companies can also offer training, maintenance, and installation support-factors critical for large-scale industrial clients.

Nevertheless, indirect sales channels remain crucial for market expansion, particularly in reaching small to mid-sized enterprises. Distributors play a key role in delivering complete product ranges, inventory solutions, and localized technical assistance. Online platforms have also become an important part of the distribution mix, offering convenience, price competitiveness, and easy access to a wider selection of machines. This shift has notably impacted purchasing decisions for small businesses seeking flexible, budget-friendly options.

Regionally, North America plays a prominent role in global market dynamics, with the United States commanding approximately 76% of the region's market in 2024 and generating close to USD 760 million in revenue. Factors such as strong technological infrastructure, rising e-commerce activities, and growing production needs in the automotive and furniture sectors have contributed to this dominance. The U.S. textile industry is also witnessing a revival driven by a focus on reshoring production and adopting sustainable practices. These developments are fueling investments in advanced industrial sewing solutions.

Market competition remains moderately concentrated, with leading companies collectively holding a market share between 15% and 20%. These key players continue to expand through strategic acquisitions, collaborations, and facility upgrades to diversify their offerings, access new customer segments, and maintain competitive advantage.