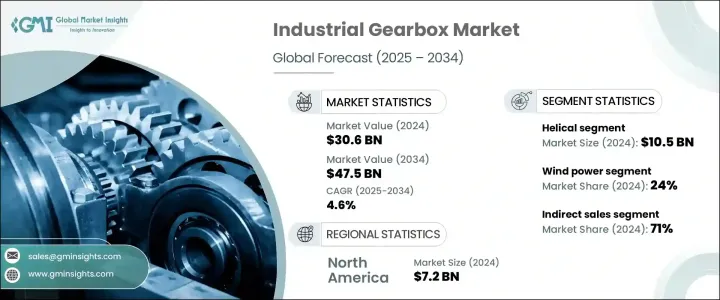

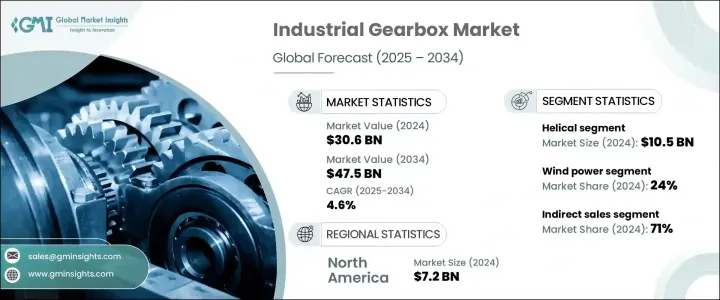

세계의 산업용 기어박스 시장은 2024년에 306억 달러에 이르렀으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 4.6%를 나타낼 것으로 예측됩니다.

이러한 성장은 다양한 부문에서 산업 자동화의 채용이 증가하고 있으며, 기어박스 기술의 지속적인 진보가 원동력이 되고 있습니다. Abox가 필요합니다. 산업계 전체의 대형 기계 수요가 증가함에 따라 시장 확대가 더욱 가속화되고 있습니다. 산업용 기어박스 드라이브에 대한 수요를 촉진하고 있습니다.

2024년 산업용 기어박스 시장의 헬리컬 부문은 105억 달러를 차지했습니다. 내구성, 고부하에 대한 대응 능력으로 알려져 자동차, 항공우주, 산업기계, 로봇 등의 산업에서 널리 이용되고 있습니다. 그리고, 헬리컬 기어의 중요한 수요원이 되고 있습니다.항공우주산업도, 가혹한 조건하에서도 효과적으로 기능하는 헬리컬 기어에 의존하고 있어, 비행, 드론, 우주 용도에서의 사용에 이상적입니다. 엔드와 같은 국가들이 주요 공급업체가 되고 있어 자동차 제조의 기반이 견고한 점에서 헬리컬 기어 수요를 선도하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 306억 달러 |

| 예측 금액 | 475억 달러 |

| CAGR | 4.6% |

풍력발전 분야는 깨끗하고 재생가능한 에너지원에 대한 수요 증가에 견인되어 2024년에는 산업용 기어박스 시장의 약 24%를 차지했습니다. 산업에 있어서 자동화의 채용은 컨베이어 시스템이나 자동 기계에 있어서의 안전하고 효율적인 기어박스 수요를 한층 더 밀어 올리고 있습니다. 전기자동차의 인기 증가도 기어박스 수요를 변화시키고 있어, EV는 고토크에 대응해, 에너지를 효율적으로 전달하는 특수한 기어박스를 필요로 하고 있습니다.

2024년에는 간접판매가 대부분의 유통채널을 차지하고 시장 점유율의 71% 이상을 차지했습니다. 중소기업은 다양한 브랜드의 다양한 기어박스를 보유하고 있는 산업기기 판매자로부터 구입을 선호합니다.

북미에서는 미국이 2024년 산업용 기어박스 시장을 선도해 지역별 시장 점유율의 약 80%를 차지했고 추정 72억 달러의 수익을 올렸습니다. 자동화의 진전이 효율적인 기어박스 수요를 촉진해, 재생 가능 에너지, 특히 풍력 발전에 대한 투자가 시장 성장의 기회를 낳고 있습니다.

The Global Industrial Gearbox Market reached USD 30.6 billion in 2024 and is projected to grow at a CAGR of 4.6% from 2025 to 2034. This growth is driven by the increasing adoption of industrial automation across diverse sectors and the continuous advancement in gearbox technology. Industrial gearboxes play a crucial role in automated applications such as CNC machines, robots, conveyor systems, and assembly lines. These systems require gearboxes that deliver high torque while maintaining compact designs to ensure accurate power transmission. The rising demand for heavy-duty machinery across industries further accelerates market expansion. The growing need for infrastructure, public works, and construction globally has also fueled the demand for industrial gearbox drives in construction machinery. Gearboxes are essential in cranes, lifts, hoists, and material-handling equipment, providing high reliability and durability in demanding applications.

In 2024, the helical segment of the industrial gearbox market accounted for USD 10.5 billion. The planetary segment is anticipated to grow at a CAGR of approximately 5% from 2025 to 2034. Helical gears, known for their smooth operation, durability, and capacity to handle high loads, are widely utilized in industries such as automotive, aerospace, industrial machinery, and robotics. The automotive industry, particularly with the growing production of automatic transmission vehicles and the increasing shift toward electric vehicles (EVs), is a significant source of demand for helical gears. The aerospace industry also relies on helical gears for their ability to function effectively in harsh conditions, making them ideal for use in flights, drones, and space applications. Asia Pacific leads the demand for helical gears, driven by its strong automobile manufacturing base, with countries like China, Japan, and India serving as major suppliers. Europe also plays a pivotal role due to its focus on alternative power and advanced automotive technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $30.6 Billion |

| Forecast Value | $47.5 Billion |

| CAGR | 4.6% |

The wind power segment accounted for approximately 24% of the industrial gearbox market in 2024, driven by increasing demand for clean and renewable energy sources. Offshore wind farms, which require high-capacity and efficient gearboxes capable of withstanding harsh environmental conditions, have fueled this growth. The adoption of automation in industries such as warehousing and logistics has further boosted the demand for secure and effective gearboxes in conveyor systems and automated machinery. The growing popularity of electric cars has also transformed gearbox demand, as EVs require specialized gearboxes that support high torque and transmit energy efficiently.

In 2024, indirect sales dominated the distribution channel, accounting for over 71% of the market share. Companies typically prefer direct distribution channels for large-scale industrial applications where customization and bulk purchases are essential. Meanwhile, small and medium-sized enterprises prefer purchasing from industrial equipment distributors who stock a wide variety of gearboxes from different brands. Some companies source gearboxes from OEMs when specialized gearboxes are needed for equipment or machinery.

In North America, the United States led the industrial gearbox market in 2024, holding around 80% of the regional market share and generating an estimated USD 7.2 billion in revenue. The US market's expansion is fueled by advancements in gearbox technology, rising demand from multiple industries, and growing interest in specialized gearboxes. Increasing automation in industries like manufacturing and energy has driven demand for efficient gearboxes, while investments in renewable energy, particularly wind power, continue to create opportunities for market growth. The rise of EVs in the automotive sector further contributes to the increasing need for compact, high-torque gearboxes in driveline and steering systems.