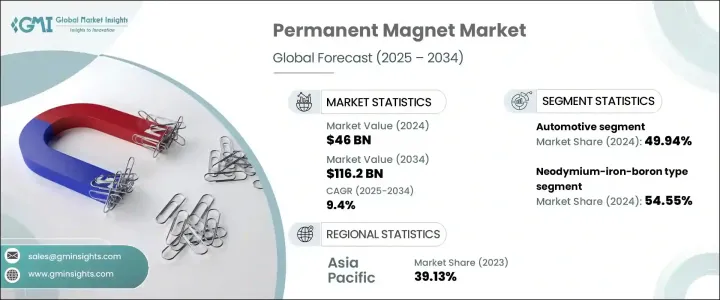

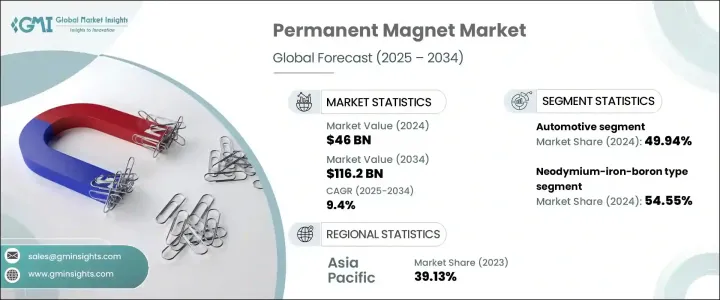

세계의 영구 자석 시장은 2024년에 460억 달러로 평가되었으며, 2025년부터 2034년에 걸쳐 CAGR 9.4%로 성장할 것으로 예측되고 있습니다.

그 주요 요인은 전기자동차(EV)의 보급률의 증가와 산업 전반에 걸친 에너지 효율 기술에 대한 수요 증가입니다. 영구 자석은 현대 엔지니어링에서 없어서는 안 될 필수 요소로, 전기 모터와 풍력 터빈에서 의료 기기 및 가전 제품에 이르기까지 다양한 제품에서 중요한 역할을 담당하고 있습니다. 산업계에서 지속 가능하고 에너지 효율적인 솔루션을 우선시함에 따라 지속적인 에너지 투입 없이도 뛰어난 강도와 신뢰성을 제공하는 고성능 자석의 필요성이 더욱 부각되고 있습니다.

외부 전원 없이도 지속적인 자기장을 유지할 수 있는 영구 자석은 특히 효율성과 공간 절약형 설계가 중요한 다양한 기계 및 전자 용도에서 선호되는 선택입니다. 운송 및 산업 자동화 분야에서 전기화로의 전환이 가속화되고 로봇 공학, 항공우주, 의료 장비의 혁신이 계속되면서 첨단 영구 자석에 대한 수요는 더욱 증가하고 있습니다. 스마트 기술과 IoT 지원 기기가 일상 생활에 빠르게 통합되면서 이러한 자석의 응용 분야가 더욱 넓어지고 있습니다. 또한 풍력 및 태양광 발전과 같은 재생 에너지원을 장려하는 정부 노력은 에너지 생성 및 저장 장비에 필수적인 고성능 자석에 대한 필요성을 간접적으로 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 460억 달러 |

| 예측 금액 | 1,162억 달러 |

| CAGR | 9.4% |

영구자석 시장은 제품 유형별로 페라이트, 네오디뮴-철-붕소(NdFeB), 사마륨-코발트, 알루미늄-니켈-코발트로 분류됩니다. 이 중 네오디뮴-철-붕소(NdFeB) 자석은 뛰어난 자기 특성으로 인해 2024년 54.55%의 점유율로 시장을 지배하고 있습니다. 이 자석은 높은 자기 에너지, 안정적인 성능, 높은 포화 유도율로 선호되며 전기 모터, 발전기, 오디오 시스템 및 다양한 모터 구동 전자 장치에 필수적으로 사용됩니다. 재료 과학과 자석 기술의 지속적인 발전으로 산업 전반에 걸쳐 NdFeB 자석이 광범위하게 채택되면서 기존의 사용 사례를 뛰어넘어 가볍지만 강력한 자석이 중요한 항공우주 및 첨단 로봇 공학 분야에서 새로운 기회를 열어가고 있습니다.

용도 관점에서 볼 때 자동차 부문은 2024년 영구 자석 시장에서 49.94%의 상당한 점유율을 차지했으며 2034년까지 9.5%의 연평균 성장률을 기록할 것으로 예상됩니다. 자동차 산업이 전기 모빌리티로 급격히 전환함에 따라 고효율 모터, 첨단 파워트레인 시스템, 정밀 센서의 통합이 가속화되고 있습니다. 네오디뮴-철-붕소 자석은 크기가 작고 성능이 우수하여 전기자동차(EV) 모터, 회생 제동 시스템 및 기타 핵심 자동차 전자장치의 핵심 부품으로 자리 잡으며 시장 확대를 주도하고 있습니다.

지역적으로 아시아태평양 영구 자석 시장은 2023년에 39.13%의 점유율을 차지할 것으로 예상되며, 중국이 광범위한 희토류 생산 능력을 바탕으로 이 시장을 주도할 것으로 보입니다. 중국은 네오디뮴-철-붕소 및 사마륨-코발트 자석에 필수적인 소재를 포함하여 전 세계 희토류 공급의 상당 부분을 통제하고 있어 가격 경쟁력과 공급망 안정성을 보장합니다. 또한 인도, 일본, 한국과 같은 국가의 산업화 성장과 견고한 수요는 전기차 시장, 재생 에너지 프로젝트, 가전제품 생산 확대에 힘입어 전 세계 영구 자석 산업에서 아시아태평양 지역의 입지를 지속적으로 강화하고 있습니다.

The Global Permanent Magnet Market generated USD 46 billion in 2024 and is projected to expand at a 9.4% CAGR from 2025 to 2034, fueled largely by the increasing penetration of electric vehicles (EVs) and the rising demand for energy-efficient technologies across industries. Permanent magnets are indispensable in modern engineering, playing a vital role in a wide array of products ranging from electric motors and wind turbines to medical devices and consumer electronics. As industries continue to prioritize sustainable and energy-efficient solutions, the need for high-performance magnets that deliver superior strength and reliability without continuous energy input is becoming even more prominent.

Their ability to maintain a persistent magnetic field without external power makes them a preferred choice for various mechanical and electronic applications, especially where efficiency and space-saving designs are critical. The accelerating shift toward electrification in transportation and industrial automation, along with ongoing innovations in robotics, aerospace, and healthcare equipment, further elevates the demand for advanced permanent magnets. The rapid integration of smart technologies and IoT-enabled devices in daily life has also contributed to the broader application landscape of these magnets. Moreover, government initiatives promoting renewable energy sources such as wind and solar power are indirectly bolstering the need for high-performance magnets essential for energy generation and storage equipment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $46 Billion |

| Forecast Value | $116.2 Billion |

| CAGR | 9.4% |

The permanent magnet market is categorized by product type into ferrite, neodymium-iron-boron (NdFeB), samarium-cobalt, and aluminum-nickel-cobalt. Among these, neodymium-iron-boron (NdFeB) magnets dominated the market with a commanding 54.55% share in 2024, primarily due to their exceptional magnetic properties. These magnets are favored for their high magnetic energy, stable performance, and high saturation induction, which make them essential for use in electric motors, generators, audio systems, and various motor-driven electronics. The ongoing advancements in material science and magnet technology have led to broader adoption of NdFeB magnets across industries, surpassing traditional use cases and opening new opportunities in sectors like aerospace and advanced robotics, where lightweight yet powerful magnets are crucial.

From an application standpoint, the automotive segment accounted for a substantial 49.94% share of the permanent magnet market in 2024 and is anticipated to grow at a 9.5% CAGR through 2034. As the automotive industry pivots sharply toward electric mobility, the integration of high-efficiency motors, advanced powertrain systems, and precision sensors is accelerating. Neodymium-iron-boron magnets, given their compact size and superior performance, have become critical components in electric vehicle (EV) motors, regenerative braking systems, and other core automotive electronics, further driving market expansion.

Regionally, the Asia Pacific Permanent Magnet Market held a dominant 39.13% share in 2023, with China spearheading this leadership position due to its extensive rare earth production capabilities. China's control over a large portion of the global rare earth supply, including materials crucial for neodymium-iron-boron and samarium-cobalt magnets, ensures competitive pricing and supply chain stability. Additionally, growing industrialization and robust demand from countries like India, Japan, and South Korea continue to strengthen Asia Pacific's standing in the global permanent magnet industry, supported by expanding EV markets, renewable energy projects, and consumer electronics production.