궤도 형상 측정 시스템 시장 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)

Track Geometry Measurement System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1716492

리서치사:Global Market Insights Inc.

발행일:2025년 03월

페이지 정보:영문 190 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

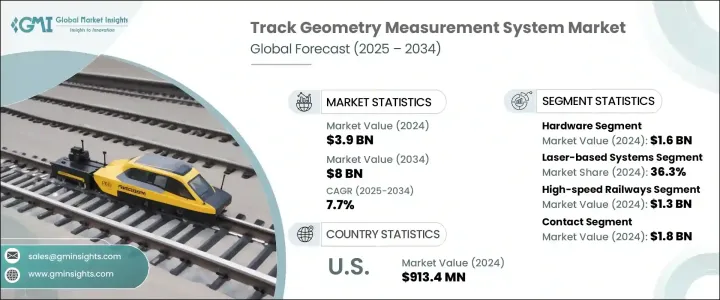

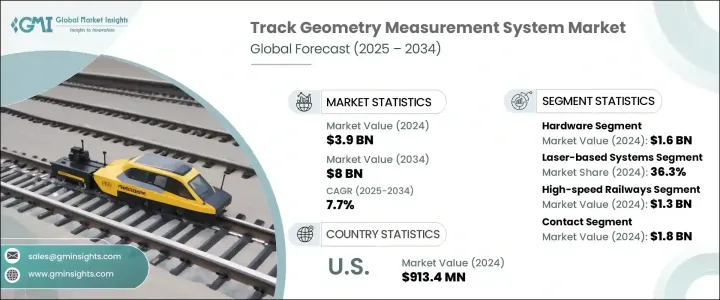

세계의 궤도 형상 측정 시스템 시장은 2024년에 39억 달러로 평가되었으며, 2025년부터 2034년에 걸쳐 CAGR 7.7%로 성장할 것으로 예측됩니다.

시장 확대의 원동력이 되고 있는 것은 수송 효율과 안전성의 향상을 목적으로 한 철도 인프라에 대한 투자 증가입니다. 노선, 화물통로를 포함한 현대적인 철도망에 대한 수요를 견인하고 있습니다.

철도 보수 비용 절감, 다운타임 최소화, 승객의 안전 확보에 점점 주목받고 있으며, 궤도 형상 측정 시스템의 채용이 더욱 가속화되고 있습니다. 인텔리전스(AI)와 머신러닝(ML)의 통합을 통해 이러한 시스템은 더욱 현명해지고, 잠재적인 궤도 장애를 예측하고, 예방 유지보수를 가능하게 하고, 시장 성장에 더욱 기여하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

39억 달러

예측 금액

80억 달러

CAGR

7.7%

궤도 형상 측정 시스템 시장은 하드웨어, 소프트웨어, 서비스 등의 구성요소로 구분됩니다. 시스템의 정확성과 신뢰성이 향상됩니다. 철도 사업자는 LiDAR 및 GNSS를 탑재한 자율주행 검사 차량과 하이레일드론 등의 선진 기술에 대한 투자를 늘리고 있어 보다 정확하고 효율적인 궤도 감시를 가능하게 하고 있습니다.

이 시장은 또한 레이저 기반 시스템, 관성 기반 시스템, GNSS, 음향 기반 시스템 등 기술 유형에 따라 세분화되어 있습니다.

이 시스템들은 레이저 스캐닝 장치를 사용하여 정렬 및 게이지와 같은 중요한 매개변수를 모니터링하고 신뢰할 수 있는 궤도 품질을 확보합니다.고속 철도 네트워크에 대한 수요의 증가는 보다 엄격한 안전 규제와 함께, 레이저 기반의 TGMS 솔루션의 인기를 견인해 가고 있습니다.

미국의 궤도 형상 측정 시스템 시장은 철도 근대화에 대한 상당액의 투자와 연방 철도 관리국(FRA) 등 당국에 의한 엄격한 규제에 의해 2024년에는 9억 1,340만 달러에 이르렀습니다. 시장의 주요 기업은 AI와 LiDAR 기반 솔루션을 통합하여 시스템의 정확성과 규제 준수를 향상시키는 데 중점을 둡니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

밸류체인에 영향을 주는 요인

이익률 분석

혁신

장래의 전망

제조업체

유통업체

공급자의 상황

이익률 분석

주요 뉴스와 대처

규제 상황

영향요인

성장 촉진요인

철도 인프라 개발과 현대화에 대한 투자 증가

정기적인 궤도 검사를 의무화하는 엄격한 정부 규제

궤도 감시 강화를 위한 AI, LiDAR, IoT의 진보

세계의 고속철도 프로젝트 확대

철도 네트워크에 있어서의 예지 보전 전략의 채용 증가

업계의 잠재적 위험 및 과제

높은 초기 투자 비용으로 소규모 사업자의 도입 제한

신 시스템과 종래의 철도 인프라와의 통합 곤란

성장 가능성 분석

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

소개

기업 점유율 분석

경쟁 포지셔닝 매트릭스

전략 전망 매트릭스

제5장 시장 추정 및 예측 : 컴포넌트별, 2021년-2034년

주요 동향

하드웨어

계측기기

데이터 처리 유닛

센서

기타

소프트웨어

데이터 분석 소프트웨어

보고 도구

통합 소프트웨어

서비스

제6장 시장 추정 및 예측 : 테크놀로지 유형별, 2021년-2034년

주요 동향

레이저 기반 시스템

관성 기반 시스템

전 지구 항법 위성 시스템(GNSS)

음향 기반 시스템

기타

제7장 시장 추정 및 예측 : 철도 유형별, 2021년-2034년

주요 동향

고속철도

대량 수송 철도

중궤조 철도

경편 철도

제8장 시장 추정 및 예측 : 운행별, 2021년-2034년

주요 동향

접촉

비접촉

관성 베이스

코드베이스

제9장 시장 추정 및 예측 : 용도별, 2021년-2034년

주요 동향

트럭 유지보수

자산 관리

궤도 검사

계획 및 설계

기타

제10장 시장 추정 및 예측 : 최종 이용 산업별, 2021년-2034년

주요 동향

철도 수송

지하철

기타

제11장 시장 추정 및 예측 : 지역별, 2021년-2034년

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

러시아

아시아태평양

중국

인도

일본

한국

호주

라틴아메리카

브라질

멕시코

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제12장 기업 프로파일

Amberg Technologies AG

Balfour Beatty plc

Bance &Co.

Deutzer Technische Kohle GmbH

ENSCO, Inc.

Fugro NV

Geismar Group

Goldschmidt Thermit Group

KZV

MER MEC SpA

Plasser &Theurer

R. Bance &Co., Ltd.

Siemens Mobility

Trimble Inc.

Vossloh AG

SHW

영문 목차

영문목차

The Global Track Geometry Measurement System Market was valued at USD 3.9 billion in 2024 and is projected to grow at a CAGR of 7.7% between 2025 and 2034. The market expansion is fueled by increasing investments in railway infrastructure aimed at enhancing transport efficiency and safety. As urbanization accelerates, population growth and heightened economic activity drive the demand for modern railway networks, including high-speed rail systems, metro lines, and freight corridors. To meet these demands, rail operators and governments worldwide are adopting advanced technologies to monitor and maintain track geometry with greater precision.

The increasing focus on reducing railway maintenance costs, minimizing downtime, and ensuring passenger safety further accelerates the adoption of track geometry measurement systems. Additionally, the need to comply with stringent safety regulations and improve the overall operational efficiency of railway systems is pushing the demand for automated and data-driven solutions in this space. With the integration of artificial intelligence (AI) and machine learning (ML), these systems are becoming smarter, capable of predicting potential track failures and enabling preventive maintenance, further contributing to the market's growth.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$3.9 Billion

Forecast Value

$8 Billion

CAGR

7.7%

The market is segmented based on components, which include hardware, software, and services. The hardware segment generated USD 1.6 billion in 2024 and remains a primary driver of growth in the TGMS market. Incorporating sophisticated sensors, laser measurement systems, and inertial devices into hardware enhances the accuracy and reliability of track monitoring systems. Rail operators are increasingly investing in advanced technologies such as self-driving inspection vehicles and hi-rail drones equipped with LiDAR and GNSS, allowing for more precise and efficient track monitoring. These technologies not only streamline maintenance processes but also reduce operational downtime and improve safety.

The market is also segmented based on technology type, including laser-based systems, inertial-based systems, GNSS, acoustic-based systems, and others. Laser-based systems accounted for a 36.3% share in 2024, owing to their superior ability to measure minute changes in track geometry with high accuracy. These systems utilize laser scanning devices to monitor critical parameters such as alignment and gauge, ensuring reliable track quality. The growing demand for high-speed rail networks, combined with stricter safety regulations, continues to drive the popularity of laser-based TGMS solutions. Inertial-based systems and GNSS technologies are also gaining traction, offering cost-effective solutions for real-time monitoring and enhancing the overall effectiveness of track geometry measurement processes.

The U.S. Track Geometry Measurement System Market reached USD 913.4 million in 2024, driven by significant investments in railway modernization and stringent regulations from authorities such as the Federal Railroad Administration (FRA). The ongoing expansion of high-speed rail projects and the extensive freight rail network have further heightened the demand for automated track inspection systems. Major players in the market are focusing on improving system accuracy and regulatory compliance by integrating AI and LiDAR-based solutions. These innovations not only optimize track monitoring processes but also enhance data accuracy, ensuring the safety and longevity of railway infrastructure.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope & definitions

1.2 Base estimates & calculations

1.3 Forecast calculations

1.4 Data sources

1.4.1 Primary

1.4.2 Secondary

1.4.2.1 Paid sources

1.4.2.2 Public sources

Chapter 2 Executive Summary

2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Factor affecting the value chain

3.1.2 Profit margin analysis

3.1.3 Disruptions

3.1.4 Future outlook

3.1.5 Manufacturers

3.1.6 Distributors

3.2 Supplier landscape

3.3 Profit margin analysis

3.4 Key news & initiatives

3.5 Regulatory landscape

3.6 Impact forces

3.6.1 Growth drivers

3.6.1.1 Increasing investments in railway infrastructure development and modernization

3.6.1.2 Strict government regulations mandating regular track inspections

3.6.1.3 Advancements in AI, LiDAR, and IoT for enhanced track monitoring

3.6.1.4 Expansion of high-speed rail projects worldwide

3.6.1.5 Rising adoption of predictive maintenance strategies in rail networks

3.6.2 Industry pitfalls & challenges

3.6.2.1 High initial investment costs limiting adoption for smaller operators

3.6.2.2 Difficulty in integrating new systems with legacy railway infrastructure