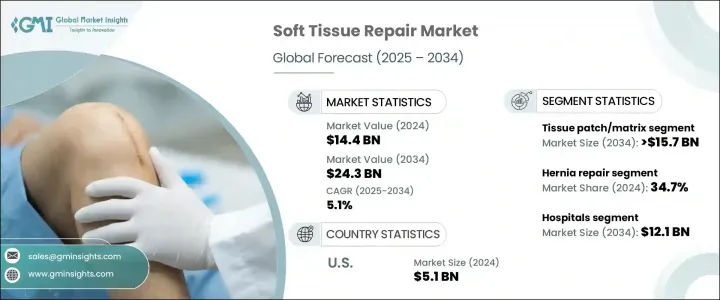

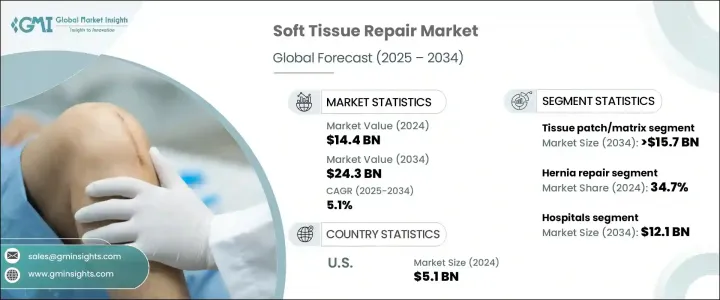

세계 연조직 복구 시장은 2024년 144억 달러에 달했으며, 2025-2034년 연평균 5.1%의 성장률을 보일 것으로 예측됩니다.

스포츠 외상, 외상 사례 증가, 노화에 따른 연조직 손상이 외과적 솔루션에 대한 수요를 촉진하고 있습니다. 노인 인구 증가와 비만율 증가는 탈장 및 기타 연조직 수리가 필요한 질환의 발생률 증가에 기여하고 있습니다. 생체 적합성 제품 및 합성 메쉬 솔루션의 발전은 환자 결과를 개선하고 외과적 개입을 보다 효과적으로 개선하고 있습니다. 영상 진단 기술과 최소 침습 수술의 발전은 회복 시간을 연장하고 수술 후 합병증을 감소시키고 있습니다.

혁신적인 수복 기술에 대한 인식이 높아지고 환자 치료 결과가 개선되면서 시장 성장의 원동력이 되고 있습니다. 스포츠 의학의 확대와 청소년의 스포츠 참여 증가는 부상률 증가로 이어져 수요를 더욱 촉진할 것입니다. 또한, 신흥 시장에서의 헬스케어에 대한 정부 투자는 새로운 성장 기회를 창출하고 있습니다. 다혈소판 혈장(PRP) 치료와 줄기세포 치료를 포함한 재생의료의 발전은 이 분야에 혁명을 가져올 것으로 예상됩니다. 복잡한 수술에 대한 의료비 지출과 보험 적용이 증가함에 따라 고급 수복 방법에 대한 접근성이 향상될 것입니다. 외래수술센터(ASC)의 외래 환자 서비스로의 전환은 비용 효율적이고 편리한 치료의 추세를 강조하며 시장 확대를 촉진할 것입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 144억 달러 |

| 예상 금액 | 243억 달러 |

| CAGR | 5.1% |

연조직 복구에는 근육의 수복, 근막 봉합, 인대, 힘줄, 피부 조직 손상의 치료가 포함됩니다. 여기에는 통증 완화 및 운동 회복을 위한 비수술적 봉합, 생물학적 솔루션, 재생 줄기세포 치료와 같은 수술 전후 개입이 포함됩니다. 시장은 조직 패치/매트릭스 및 조직 고정 기구로 나뉩니다. 조직 패치/매트릭스 분야는 수술 시 효과적인 스캐폴딩 솔루션의 필요성에 힘입어 연평균 4.9%의 성장률을 보이며 2034년 157억 달러 이상에 이를 것으로 예상됩니다. 외상, 탈장, 노화에 따른 조직 변성 등의 사례가 증가함에 따라 수요가 증가하고 있습니다. 재료 과학의 발전, 특히 생체 공학 및 합성 패치는 우수한 생체 적합성과 낮은 거부 반응 위험으로 환자 결과를 향상시킬 수 있습니다.

복강경 수술과 같은 최신 수술 기술은 합병증과 회복 기간을 단축하여 조직 패치의 채택을 지원하고 있습니다. 스포츠 부상 발생률 증가와 고령화 인구 증가로 인해 효율적인 조직 복구 솔루션이 더욱 절실히 요구되고 있습니다. 선천적 조직과 원활하게 통합되는 생체공학 스캐폴딩을 포함한 재생의료의 혁신은 그 용도를 확장하고 있습니다. 헬스케어에 대한 투자 증가와 외과 수술에 대한 보험 적용이 개선되면서 첨단 조직 복구 솔루션의 보급이 촉진되고 있습니다. 외래수술센터(ASC)의 외래 수술에 대한 관심은 비용 효율적이고 회복이 빠른 재료에 대한 수요를 가속화하여 조직 매트릭스와 패치가 외과 의사들 사이에서 선호되는 선택으로 자리 잡고 있습니다.

시장은 용도별로 탈장 복구, 정형외과 수술, 피부 복구, 경막 복구, 기타 치료로 구분됩니다. 탈장수술은 2024년 시장의 34.7%를 차지할 것으로 예상되며, 이는 비만율 증가, 고령화, 좌식 생활습관 등에 기인한 것으로 분석됩니다. 복강경 수술과 개복 수술의 채택이 증가함에 따라 재발을 줄이고 회복 시간을 개선하는 합성 섬유와 생물학적 메쉬를 포함한 첨단 복구 재료에 대한 수요가 증가하고 있습니다. 탈장 치료 솔루션에 대한 환자와 외과의사의 신뢰도가 높아지면서 시장 확대의 원동력이 되고 있습니다.

용도별 부문은 병원, 외래수술센터(ASC), 클리닉을 포함하며, 병원은 2024년 48.3%의 점유율로 시장을 주도할 것으로 예상되며, 2034년에는 121억 달러에 달할 것으로 예상됩니다. 병원은 복잡한 수술 사례, 첨단 의료 인프라, 전문적인 수술 후 관리로 인해 병원이 주요 치료 센터가 되고 있습니다. 고령화와 생활습관병으로 인한 수술 건수 증가는 연조직 복구에서 병원의 우위를 더욱 강화시키고 있습니다.

미국 연조직 복구 시장은 2023년 47억 달러, 2024년 51억 달러로 평가되며 강력한 성장이 예상됩니다. 만성 질환, 스포츠 외상, 노화에 따른 조직 퇴행 등 증가로 인해 고급 수복 솔루션에 대한 수요가 증가하고 있습니다. 생물학적 제제 및 합성 메쉬의 채택 확대는 치료 효과를 높이고 있습니다. 회복 시간을 단축하고 합병증을 줄이는 최소 침습적 복강경 기술이 인기를 끌고 있습니다. 유리한 상환 정책과 높은 의료비 지출로 인해 환자들이 혁신적인 치료법을 더 많이 이용할 수 있게 되었습니다. 신흥국 시장에는 주요 제조업체가 존재하여 지속적인 제품 개발이 이루어지고 시장 개척이 강화되고 있습니다. 외래수술센터(ASC)로의 전환과 첨단 병원 인프라가 보다 광범위한 보급을 뒷받침하고 있습니다.

The Global Soft Tissue Repair Market reached USD 14.4 billion in 2024 and is projected to expand at a CAGR of 5.1% from 2025 to 2034. Rising sports injuries, trauma cases, and age-related soft tissue damage are driving demand for surgical solutions. A growing elderly population and increasing obesity rates contribute to higher incidences of hernias and other conditions requiring soft tissue repair. Advances in biocompatible products and synthetic mesh solutions are improving patient outcomes, making surgical interventions more effective. Progress in imaging techniques and minimally invasive procedures enhances recovery times and reduces post-operative complications.

Greater awareness of innovative repair techniques and improved patient outcomes fuel market growth. The expansion of sports medicine and increased youth participation in sports result in higher injury rates, further driving demand. Additionally, government investments in healthcare in emerging markets are creating new growth opportunities. Future developments in regenerative medicine, including platelet-rich plasma (PRP) therapy and stem cell treatments, are expected to revolutionize the field. Increased healthcare spending and insurance coverage for complex surgeries improve access to advanced repair methods. A shift towards outpatient services in ambulatory surgical centers highlights the trend of cost-effective, convenient care, reinforcing market expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.4 Billion |

| Forecast Value | $24.3 Billion |

| CAGR | 5.1% |

Soft tissue repair encompasses muscle restoration, fascia suturing, and treatment of ligaments, tendons, and skin tissue damage. This includes perioperative and post-operative interventions such as non-surgical sutures, biological solutions, and regenerative stem cell therapies aimed at pain relief and motion recovery. The market is divided into tissue patch/matrix and tissue fixation devices. The tissue patch/matrix segment, driven by the need for effective scaffolding solutions in surgeries, is expected to grow at a CAGR of 4.9%, reaching over USD 15.7 billion by 2034. Increased cases of traumatic injuries, hernias, and age-related tissue degeneration are boosting demand. Advances in materials science, particularly bioengineered and synthetic patches, enhance patient outcomes due to superior biocompatibility and lower rejection risks.

Modern surgical techniques, such as laparoscopic procedures, support the adoption of tissue patches by reducing complications and recovery periods. The rising incidence of sports injuries and a growing aging population further necessitate efficient tissue repair solutions. Innovations in regenerative medicine, including bioengineered scaffolds that integrate seamlessly with native tissues, expand their applications. Increased healthcare investments and improved insurance coverage for surgical procedures facilitate wider adoption of advanced tissue repair solutions. The focus on outpatient procedures in ambulatory surgical centers accelerates the demand for cost-effective and rapid recovery materials, positioning tissue matrices and patches as preferred options among surgeons.

The market is segmented by application into hernia repair, orthopedic procedures, skin repair, dural repair, and other treatments. Hernia repair accounted for 34.7% of the market in 2024, driven by rising obesity rates, an aging population, and sedentary lifestyles. Increased adoption of laparoscopic and open surgical procedures boosts demand for advanced repair materials, including synthetic and biological meshes that reduce recurrence and improve recovery times. Enhanced patient and surgeon confidence in hernia repair solutions continues to drive market expansion.

End-use segmentation includes hospitals, ambulatory surgical centers, and clinics. Hospitals led the market in 2024, holding a 48.3% share and projected to reach USD 12.1 billion by 2034. The high volume of complex surgical cases, advanced medical infrastructure, and specialized post-operative care make hospitals the primary treatment centers. Rising surgical volumes due to aging populations and lifestyle-related conditions further reinforce hospital dominance in soft tissue repair.

The U.S. soft tissue repair market was valued at USD 4.7 billion in 2023 and USD 5.1 billion in 2024, with strong growth projections. Increased cases of chronic diseases, sports injuries, and age-related tissue degeneration drive demand for advanced repair solutions. The growing adoption of biologics and synthetic meshes enhances the effectiveness of treatments. Minimally invasive laparoscopic techniques, which shorten recovery times and reduce complications, are gaining traction. Favorable reimbursement policies and high healthcare spending enable greater patient access to innovative repair methods. The presence of leading manufacturers fosters continuous product development, strengthening market growth. The shift toward outpatient surgical centers and advanced hospital infrastructure supports broader ado