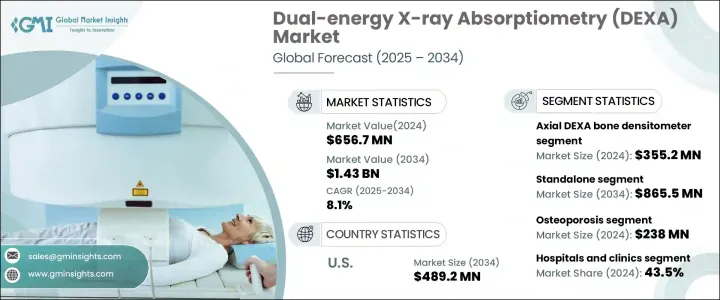

세계의 이중 에너지 X선 흡수 측정 시장은 2024년에 6억 5,670만 달러로 평가되었으며, 2025-2034년 CAGR 8.1%로 확대될 것으로 예측되고 있습니다.

DEXA는 골밀도(BMD)와 신체 조성을 평가하기 위해 설계된 널리 사용되는 의료용 이미지 기술입니다. DEXA의 주요 용도는 골다공증 진단과 뼈 건강 상태의 장기적인 추적입니다. 골다공증 유병률 상승 및 세계 고령화가 이 시스템 수요 증가의 주요 원동력이 되고 있습니다. 고령자에서는 골절 위험이 높고 BMD가 저하되기 때문에 조기 발견과 지속적인 모니터링의 필요성이 높아지고 있습니다. DEXA 시스템은 골절 위험의 평가 및 뼈 건강 상태를 측정하는 높은 정밀도로 병원, 진단 센터, 전문 클리닉에서 보급되고 있습니다. 예방 헬스케어 중시 및 의료 영상 기술의 진보가 시장의 성장을 더욱 가속화시키고 있습니다.

시장은 축방향 DEXA 골밀도계 및 말초 DEXA 골밀도계로 나뉘어져 있습니다. 2024년에는 축방향 DEXA 부문이 시장을 선도하며 3억 5,520만 달러의 수익을 올렸습니다. 이 부문은 골다공증 진단 및 고관절이나 척추와 같은 중요한 골격 부위의 BMD 평가에서 높은 정확도로 지지되고 있습니다. 말초 시스템과 비교하여 축방향 DEXA는 골다공증의 초기 징후를 검출하고 치료 경과를 모니터링하는 데 있어 우수한 정밀도를 제공합니다. 또, 스포츠 의학 및 비만 관리에도 널리 사용됨으로써 시장의 우위성에 기여하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 6억 5,670만 달러 |

| 예측 금액 | 14억 3,000만 달러 |

| CAGR | 8.1% |

시장의 또 다른 세분화는 제품 유형을 기반으로 하며, 이는 독립형 및 휴대용 DEXA 시스템을 포함합니다. 독립형은 2024년 시장 점유율의 59.4%를 차지했으며, 2034년 전망치는 8억 6,550만 달러로 예상됩니다. 이러한 시스템은 주로 병원, 진단 센터 및 연구 기관에 설치되며 골밀도 평가에 있어 높은 화상 강도와 정밀도를 제공하고 있습니다. 정확한 진단을 제공하고 대사 건강 평가를 지원하는 능력으로 의료시설에서 즐겨 사용되고 있습니다. 업계를 리드하는 기업은, 진단 효율을 해치는 일 없이 환자의 안전성을 높이기 위해, 저선량 방사선 기능을 통합하고 있습니다.

용도와 관련하여 DEXA 시장은 골다공증 진단, 신체 조성 분석, 골절 관리, 골밀도 측정 및 기타 의료 용도를 포함합니다. 골다공증 분야는 2024년에 2억 3,800만 달러를 창출하였으며, 유병률 증가로 주도적 지위를 유지하고 있습니다. 뼈 건강에 대한 의식이 높아지면서 조기 발견과 정기적인 평가를 우선시하는 환자나 의료 제공자가 늘고 있습니다.

병원 및 진료소가 최종 용도 분야의 1위에 부상해, 2024년에 시장 점유율의 43.5%를 획득했습니다. 이들 기관은 정확한 골다공증 진단 및 환자 모니터링을 위해 DEXA 스캔을 실시하는 1차 의료 제공자 역할을 하고 있습니다. 이러한 시설에서는 고도의 의료기기와 숙련된 전문가의 조합이, 이러한 시스템의 보급에 기여하고 있습니다.

미국 시장은 상당한 수익 성장을 보이고 있으며, 2023년에는 2억 1,260만 달러에 이르렀으며, 2034년에는 4억 8,920만 달러에 이를 것으로 예측되고 있습니다. 골다공증 유병률의 높은 수준 및 골밀도 검사에 대한 보험 적용이 시장 확대의 주요 요인입니다.

The Global Dual-Energy X-Ray Absorptiometry Market was valued at USD 656.7 million in 2024 and is projected to expand at a CAGR of 8.1% from 2025 to 2034. DEXA is a widely used medical imaging technology designed to assess bone mineral density (BMD) and body composition. Its primary application is in diagnosing osteoporosis and tracking bone health over time. The rising prevalence of osteoporosis and an aging global population are key drivers behind the increasing demand for these systems. With a higher risk of fractures and reduced BMD among older adults, the need for early detection and continuous monitoring is growing. DEXA systems are becoming more prevalent in hospitals, diagnostic centers, and specialty clinics due to their precision in evaluating fracture risks and measuring bone health. The emphasis on preventive healthcare and advancements in medical imaging technologies are further accelerating market growth.

The market is divided into total axial and peripheral DEXA bone densitometers. In 2024, the axial DEXA segment led the market, generating USD 355.2 million in revenue. This segment is favored for its high accuracy in diagnosing osteoporosis and assessing BMD in crucial skeletal regions like the hip and spine. Compared to peripheral systems, axial DEXA provides superior precision in detecting early signs of osteoporosis and monitoring treatment progress. Its extensive use in sports medicine and obesity management also contributes to its market dominance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $656.7 Million |

| Forecast Value | $1.43 Billion |

| CAGR | 8.1% |

Another segmentation of the market is based on product type, which includes standalone and portable DEXA systems. The standalone segment accounted for 59.4% of the market share in 2024, with a projected value of USD 865.5 million by 2034. These systems are primarily installed in hospitals, diagnostic centers, and research institutions, where they offer high imaging strength and accuracy in bone density assessment. Their ability to provide precise diagnostics and support metabolic health evaluations makes them a preferred choice in medical facilities. Leading industry players are integrating low-dose radiation features to enhance patient safety without compromising diagnostic efficiency.

Regarding applications, the DEXA market encompasses osteoporosis diagnosis, body composition analysis, fracture management, bone densitometry, and other medical uses. The osteoporosis segment generated USD 238 million in 2024, maintaining a leading position due to the increasing prevalence of the disease. As bone health awareness grows, more patients and healthcare providers are prioritizing early detection and routine assessments.

Hospitals and clinics emerged as the top end-use segment, capturing 43.5% of the market share in 2024. These institutions serve as primary healthcare providers, conducting DEXA scans for accurate osteoporosis diagnosis and patient monitoring. The combination of advanced medical equipment and skilled professionals in these facilities contributes to the widespread adoption of these systems.

The U.S. market has seen substantial revenue growth, reaching USD 212.6 million in 2023, and is projected to hit USD 489.2 million by 2034. High osteoporosis prevalence and insurance coverage for bone density tests are key factors fueling market expansion.