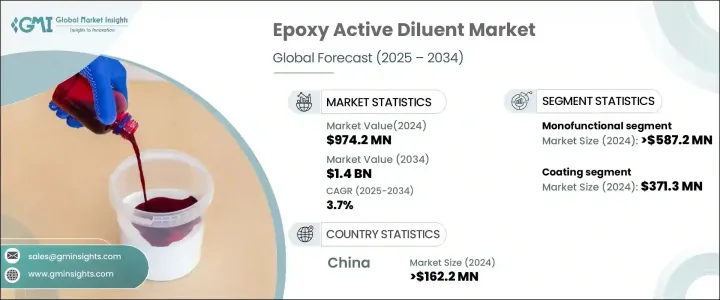

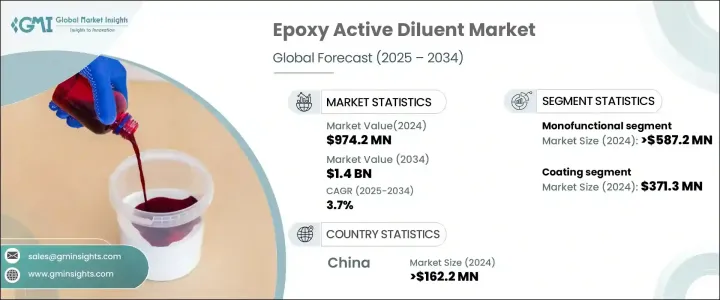

세계의 에폭시 활성 희석제 시장은 2024년 9억 7,420만 달러였고, 2025년부터 2034년까지 CAGR 3.7%를 나타낼 것으로 예측됩니다.

코팅, 접착제, 복합재료에서 에폭시 수지 수요 증가가 이 성장의 원동력이 되고 있습니다. 이러한 희석제는 수지의 점도를 낮추고 가공 및 도포를 용이하게 하는 중요한 역할을 합니다. 내구성과 효율성을 향상시키는 고성능 재료를 요구하는 제조업체에 의해 용도는 다양한 산업에서 확대되고 있습니다. 오래 지속되는 보호 성능과 미관을 겸비한 뛰어난 페인트를 요구하는 움직임은 시장 확대에 더욱 박차를 가하고 있습니다.

친환경 제품으로의 전환이 시장 상황을 형성하고 있습니다. 에폭시 활성 희석제는 기존의 용매보다 휘발성 유기 화합물(VOC)의 배출량이 적기 때문에 기업이 지속가능성을 중시하는 가운데 바람직한 선택이 되고 있습니다. 또한, 바이오 희석제의 진보는 세계 규제에 맞게 친환경적인 대안을 제공합니다. 산업계가 성능과 환경기준을 충족하기 위해 혁신적인 배합을 도입함으로써 시장은 꾸준히 성장할 전망입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 9억 7,420만 달러 |

| 예측 금액 | 14억 달러 |

| CAGR | 3.7% |

단관능성 부문은 2024년 5억 8,720만 달러 이상을 창출했고 2034년까지 연평균 복합 성장률(CAGR) 3.9%로 확대될 것으로 예상됩니다. 그 이점은 산업 응용 분야에서 다용도와 신뢰성 때문입니다. 이러한 희석제는 보다 우수한 경화 특성, 내화학성 및 접착성을 보장하기 때문에 고정밀 용도에 필수적입니다. 단관능성 희석제 수요는 점도 제어와 가공 효율의 향상이 선호되는 산업계에서 계속 견인되고 있습니다. 그 예측 가능한 성능은 특수 코팅 및 배합에 필수적이며 시장에서의 리더십을 강화하고 있습니다.

페인트 분야가 2024년 매출 3억 7,130만 달러로 시장을 선도해 2025년부터 2034년까지 CAGR 3.8%로 성장할 것으로 예상되고 있습니다. 에폭시 기반 코팅의 광범위한 채택은 우수한 접착력, 내구성 및 환경 요인에 대한 내성을 제공하는 능력에 기인합니다. 제품의 수명과 미관을 향상시키기 위해 에폭시계 코팅에 대한 의존도가 높아지고 있습니다. 제조업체가 효율성과 지속가능성을 우선시함에 따라 코팅 수요는 증가의 길을 따라가고 있으며, 주요 용도 분야로서의 입지를 강화하고 있습니다.

중국은 2024년 1억 6,220만 달러를 넘었고 CAGR 3.4%로 성장할 것으로 예상됩니다. 세계 시장에서 중국의 지배적 지위는 강력한 제조거점과 비용 효율적인 고성능 재료에 대한 수요 증가로 이어지고 있습니다. 이 나라에서 진행중인 산업화와 인프라 프로젝트는 에폭시 수지의 상당한 소비에 기여합니다. 게다가 지속가능성을 촉진하는 규제조치는 낮은 VOC로 친환경 솔루션으로의 전환을 가속화하고 있습니다. 중국은 여전히 생산과 소비의 주요 기업이며 세계 시장에서 영향력을 강화하고 있습니다.

The Global Epoxy Active Diluent Market was valued at USD 974.2 million in 2024 and is projected to grow at a CAGR of 3.7% from 2025 to 2034. The increasing demand for epoxy resins in coatings, adhesives, and composites is driving this growth. These diluents play a critical role in reducing resin viscosity, making them easier to process and apply. Their use is expanding across multiple industries as manufacturers seek high-performance materials that enhance durability and efficiency. The push for superior coatings that offer long-lasting protection and aesthetic appeal is further fueling market expansion.

The shift toward environmentally friendly products is shaping the market landscape. Epoxy active diluents emit lower levels of volatile organic compounds (VOCs) than traditional solvents, making them a preferred choice as companies focus on sustainability. Additionally, advancements in bio-based diluents are providing eco-conscious alternatives, aligning with global regulations. The market is poised to grow steadily as industries integrate innovative formulations to meet performance and environmental standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $974.2 million |

| Forecast Value | $1.4 billion |

| CAGR | 3.7% |

The monofunctional segment generated over USD 587.2 million in 2024 and is set to expand at a CAGR of 3.9% through 2034. Its dominance is attributed to versatility and reliability in industrial applications. These diluents ensure better curing properties, chemical resistance, and adhesion, making them essential for high-precision applications. Industries favoring controlled viscosity and improved processing efficiency continue to drive the demand for monofunctional diluents. Their predictable performance makes them indispensable for specialized coatings and formulations, reinforcing their market leadership.

The coatings segment led the market with USD 371.3 million in revenue in 2024 and is expected to grow at a 3.8% CAGR from 2025 to 2034. The widespread adoption of epoxy-based coatings stems from their ability to provide excellent adhesion, durability, and resistance to environmental factors. Industries increasingly rely on these coatings to enhance product longevity and aesthetic value. As manufacturers prioritize efficiency and sustainability, demand for coatings continues to rise, solidifying their position as the leading application segment.

China accounted for over USD 162.2 million in 2024 and is expected to grow at a 3.4% CAGR. Its dominant position in the global market is driven by a strong manufacturing base and rising demand for cost-effective, high-performance materials. The country's ongoing industrialization and infrastructure projects contribute to substantial consumption of epoxy resins. Moreover, regulatory measures promoting sustainability are accelerating the transition toward low-VOC and eco-friendly solutions. China remains a key player in production and consumption, strengthening its influence in the global market.