Metalworking Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1665364

리서치사:Global Market Insights Inc.

발행일:2024년 12월

페이지 정보:영문 225 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

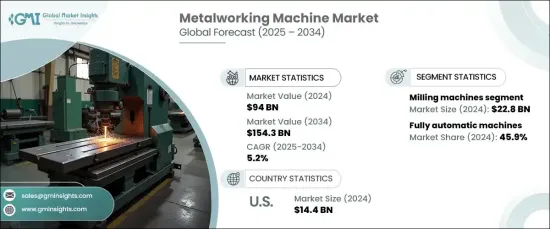

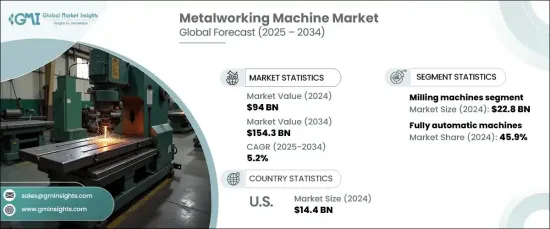

세계의 금속가공기계 시장은 2024년에 940억 달러로 평가되며, 2025-2034년에 CAGR 5.2%로 견고하게 확대할 전망입니다. 이러한 성장의 원동력은 특히 신흥 경제권에서 두드러지게 나타나는 세계 제조업의 급속한 성장에 기인합니다. 이들 지역에서는 증가하는 소비자 수요에 대응하고 생산 능력을 강화하기 위해 인프라와 제조업에 대한 대규모 투자가 이루어지고 있으며, 이는 첨단 금속 가공 기계에 대한 수요를 촉진하고 있습니다.

이 시장의 주요 촉진요인으로는 자동차 산업과 항공우주 산업을 들 수 있습니다. 자동차 산업에서는 전기자동차(EV)와 경량화 소재에 대한 노력이 추진되고 있으며, 알루미늄 및 복합재와 같은 소재를 가공할 수 있는 첨단 기계에 대한 수요가 증가하고 있습니다. 동시에, 항공우주 산업에서는 상업용 및 국방용 고성능 및 내구성 부품에 대한 수요가 까다로운 품질 기준을 충족하는 정밀 금속 가공 기계의 필요성을 강조하고 있습니다.

시장 범위

시작연도

2024년

예측연도

2025-2034년

시작 금액

940억 달러

예상 금액

1,543억 달러

CAGR

5.2%

밀링 머신 부문은 2024년 228억 달러로 평가되었고, 2034년까지 연평균 5.5%의 높은 성장률을 보일 것으로 예상됩니다. 이러한 기계는 자동차, 항공우주, 일반 제조업 등 정밀도와 범용성이 중요한 산업에서 매우 중요한 역할을 담당하고 있습니다. CNC(컴퓨터 수치 제어) 기술의 발전과 함께 경량화 및 복잡하게 설계된 부품에 대한 수요가 증가함에 따라 밀링 머신의 매력이 크게 증가하고 있으며, CNC 시스템이 제공하는 향상된 속도, 정확성 및 자동화로 인해 현대의 제조 환경에서 필수 불가결한 기계가 되었습니다. 필수적인 장비가 되었습니다.

자동화는 시장을 발전시키는 또 다른 중요한 요소입니다. 전자동 금속 가공 기계는 2024년 시장 점유율 45.9%를 차지하며, 2025-2034년 연평균 5.7%의 성장률을 보일 것으로 예상됩니다. 이러한 기계는 사람의 개입을 최소화하고 일관된 품질을 보장하면서 대량 생산에 탁월하며 인적 오류를 줄일 수 있습니다. 운영 비용을 절감하고 복잡하고 정밀한 부품을 생산하기 위해 자동화에 대한 중요성이 강조되면서 이러한 기계의 채택이 가속화되고 있습니다. 또한 이러한 기계를 스마트 팩토리 시스템에 통합함으로써 업무 효율성을 높이고 인건비를 최소화할 수 있으므로 자동차, 항공우주, 전자 등의 산업에서 중요한 자산이 되고 있습니다.

미국의 금속 가공 기계 시장은 2024년 144억 달러 규모로 평가되며, 이 분야의 세계 리더로 자리매김하고 있습니다. 첨단 제조 인프라와 기술 혁신에 대한 강한 집념을 가진 미국은 특히 자동화 및 스마트 제조 분야에서 최첨단 기술을 도입해 왔습니다. 이를 통해 첨단 금속 가공 기계가 널리 채택되어 다양한 부문에서 높은 생산성과 탁월한 정밀도를 실현하고 있습니다.

목차

제1장 조사 방법과 조사 범위

시장 범위와 정의

기본 추정과 계산

예측 파라미터

데이터 소스

1차 데이터

2차 데이터

유료 정보원

공적 정보원

제2장 개요

제3장 산업 인사이트

에코시스템 분석

밸류체인에 영향을 미치는 요인

이익률 분석

변혁

향후 전망

제조업체

유통업체

소매업체

영향요인

촉진요인

산업화와 제조업의 성장

자동차 산업과 항공우주 산업의 성장

공작기계에서 끊임없는 기술 혁신

정도와 품질에 대한 요구

산업의 잠재적 리스크·과제

높은 초기 투자 비용

변동하는 원료 가격

기술 혁신 상황

소비자 구매 행동 분석

인구 동향

구매 결정에 영향을 미치는 요인

소비자의 제품 채택

선호 유통 채널

성장 가능성 분석

규제 상황

가격 분석

Porter의 산업 분석

PESTEL 분석

제4장 경쟁 구도

서론

기업 점유율 분석

경쟁 포지셔닝 매트릭스

전략 전망 매트릭스

제5장 시장 추정·예측 : 제품별, 2021-2034년

주요 동향

선반

밀링 머신

드릴링 머신

보링 머신

기타

제6장 시장 추정·예측 : 자동화 레벨별, 2021-2034년

주요 동향

수동기

반자동기

전자동기

제7장 시장 추정·예측 : 용도별, 2021-2034년

주요 동향

자동차

항공우주·방위

건설

에너지 전력

일렉트로닉스

산업 기기

의료기기

소비재

기타

제8장 시장 추정·예측 : 재료별, 2021-2034년

주요 동향

철강

알루미늄

주철

티타늄

기타

제9장 시장 추정·예측 : 유통 채널별, 2021-2034년

주요 동향

직접

간접

제10장 시장 추정·예측 : 지역별, 2021-2034년

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

아시아태평양

중국

인도

일본

한국

호주

말레이시아

인도네시아

라틴아메리카

브라질

멕시코

중동 및 아프리카

사우디아라비아

아랍에미리트

남아프리카공화국

제11장 기업 개요

Biesse Group

CNC Masters

DMG Mori

Doosan Machine Tools

Emag

FANUC

Haas Automation

Hermle

Makino

Mazak

Mitsubishi Heavy Industries Machine Tool

Okuma Corporation

Schuler Group

Toshiba Machine

Trumpf

KSA

영문 목차

영문목차

The Global Metalworking Machine Market, valued at USD 94 billion in 2024, is set to expand at a robust CAGR of 5.2% between 2025 and 2034. This growth is fueled by the rapid expansion of manufacturing industries worldwide, particularly in emerging economies. These regions are making significant investments in infrastructure and manufacturing to address rising consumer demands and enhance production capacities, driving the demand for advanced metalworking machines.

Key drivers of this market include the automotive and aerospace industries. The automotive sector's push toward electric vehicles (EVs) and lightweight materials has heightened the need for advanced machinery capable of processing materials like aluminum and composites. Simultaneously, the aerospace industry's demand for high-performance, durable components for commercial and defense applications underscores the need for precision metalworking machines that meet stringent quality standards.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$94 Billion

Forecast Value

$154.3 Billion

CAGR

5.2%

The milling machines segment, valued at USD 22.8 billion in 2024, is poised for strong growth at a CAGR of 5.5% through 2034. These machines play a pivotal role in industries such as automotive, aerospace, and general manufacturing, where precision and versatility are crucial. The increasing demand for lightweight and intricately designed components, coupled with advancements in CNC (Computer Numerical Control) technology, has significantly boosted the appeal of milling machines. Enhanced speed, accuracy, and automation offered by CNC systems make these machines indispensable in modern manufacturing environments.

Automation is another critical factor propelling the market forward. Fully automatic metalworking machines accounted for 45.9% of the market share in 2024 and are expected to grow at a CAGR of 5.7% from 2025 to 2034. These machines, requiring minimal human intervention, excel in high-volume production while ensuring consistent quality and reducing human error. The growing emphasis on automation to cut operational costs and produce complex, precision-driven components is spurring their adoption. Moreover, the integration of these machines into smart factory systems enhances operational efficiency and minimizes labor expenses, making them a key asset in industries such as automotive, aerospace, and electronics.

The U.S. metalworking machine market, valued at USD 14.4 billion in 2024, remains a global leader in the industry. With its advanced manufacturing infrastructure and a strong focus on innovation, the U.S. has embraced cutting-edge technologies, particularly in automation and smart manufacturing. This has driven widespread adoption of advanced metalworking machines, enabling higher productivity and unmatched precision across diverse sectors.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope & definition

1.2 Base estimates & calculations

1.3 Forecast parameters

1.4 Data sources

1.4.1 Primary

1.4.2 Secondary

1.4.2.1 Paid sources

1.4.2.2 Public sources

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Factors affecting the value chain

3.1.2 Profit margin analysis

3.1.3 Disruptions

3.1.4 Future outlook

3.1.5 Manufacturers

3.1.6 Distributors

3.1.7 Retailers

3.2 Impact forces

3.2.1 Growth drivers

3.2.1.1 Industrialization and manufacturing growth

3.2.1.2 Growth in the automotive and aerospace industries