Pessary Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1665292

리서치사:Global Market Insights Inc.

발행일:2024년 12월

페이지 정보:영문 130 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

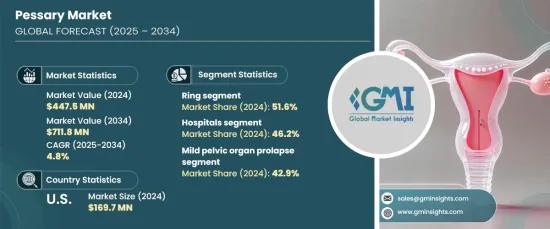

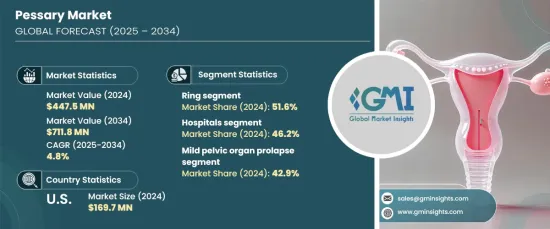

세계의 페서리 시장은 2024년에 4억 4,750만 달러로 평가되었고, 2025년부터 2034년까지 CAGR 4.8%로 안정된 성장을 이룰 것으로 예측되고 있습니다. 이 성장은 주로 골반장기탈(POP)과 요실금 유병률 증가, 시기적절한 진단과 치료의 중요성에 대한 의식 증가, 비침습적인 치료 옵션에 대한 선호도 증가, 여성의 건강 프로그램을 지원하는 정부의 이니셔티브의 강화에 의해 초래됩니다.

시장은 유형별로 구분되며, 링 페서리는 2024년 시장 점유율의 51.6%를 차지하여 선도했습니다. 링 페서리가 우위를 유지하고 있는 이유는 범용성, 사용의 용이성, 경량의 쾌적성에 있어, 경도로부터 중등도의 탈항이나 스트레스성 요실금에 고민하는 사람에게 최적입니다. 그 디자인은 자극을 줄이고 장시간 사용을 가능하게 하기 위해 임상 현장에서 선호되고 널리 받아들여지는 요인이 되고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

4억 4,750만 달러

예측 금액

7억 1,180만 달러

CAGR

4.8%

최종 사용자별로 병원은 주요 부문으로 부상하여 2024년 시장 점유율의 46.2%를 차지했습니다. 병원은 POP 및 스트레스성 요실금과 같은 골반저장애의 진단, 관리, 치료에 매우 중요한 역할을 합니다. 이 의료 기관은 수술적 및 비 수술적 페서리 치료를 모두 제공하며 다양한 중증도의 환자를 수용합니다. 복잡한 사례에 대응하고 필수적인 후속 관리를 제공하는 능력은 페서리 시장에서 우위를 더욱 강화하고 있습니다.

미국의 페서리 시장은 2024년에 1억 6,970만 달러로 평가되었으며, 여전히 강력한 성장 가능성을 보여줍니다. 비만과 같은 생활습관과 관련된 건강상태와 함께 골반장애 증가는 효과적이고 비침습적인 치료 솔루션으로서 페서리 수요 증가를 촉진하고 있습니다. 의료에 대한 접근이 확대되고 골반의 건강 문제에 대한 의식을 높이는 노력이 계속되고 있는 것이, 국내 전역에서 시장의 지속적인 성장에 기여하고 있습니다.

목차

제1장 조사 방법 및 조사 범위

제2장 주요 요약

제3장 산업 인사이트

생태계 분석

산업에 미치는 영향요인

성장 촉진요인

골반장기 탈 및 요실금의 유병률 증가

적시의 진단 및 치료에 대한 의식의 고조

비침습적 치료 옵션의 채용 증가

여성 건강 프로그램에 있어서 정부 지원 증가

산업의 잠재적 리스크 및 과제

사회적 스티그마와 심리적 장벽

장기 사용으로 인한 감염 위험에 대한 우려

성장 가능성 분석

특허 분석

갭 분석

규제 상황

기술적 전망

향후 시장 동향

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

서문

기업 점유율 분석

주요 시장 진출기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략 전망

제5장 시장 추정 및 예측 : 유형별(2021-2034년)

주요 동향

링

도넛

겔혼

기타

제6장 시장 추정 및 예측 : 용도별(2021-2034년)

주요 동향

경도의 골반 장기 탈

스트레스성 요실금

심한 골반장기 탈

기타

제7장 시장 추정 및 예측 : 최종 용도별(2021-2034년)

주요 동향

병원

외래수술센터(ASC)

클리닉

기타

제8장 시장 추정 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제9장 기업 프로파일

Artisan Medical

BIoTeque America

Bliss GVS Pharma

Bray Group(Ethos Partners)

Coloplast Group

Contiform International

CooperSurgical

Dr. Arabin

Integra Lifesciences

MedGyn Products

Novomed group(Gyneas)

Panpac Medical

Personal Medical

Smiths Group

Sugar International

AJY

영문 목차

영문목차

The Global Pessary Market was valued at USD 447.5 million in 2024 and is projected to experience steady growth at a CAGR of 4.8% from 2025 to 2034. This growth is primarily driven by the increasing prevalence of pelvic organ prolapse (POP) and urinary incontinence, heightened awareness about the importance of timely diagnosis and treatment, growing preference for non-invasive therapy options, and strengthened government initiatives supporting women's health programs.

The market is segmented by type, with the ring pessary leading the way, accounting for 51.6% of the market share in 2024. The ring pessary's continued dominance can be attributed to its versatility, ease of use, and lightweight comfort, making it ideal for individuals suffering from mild to moderate prolapse and stress urinary incontinence. Its design reduces irritation and allows for prolonged use, making it a favored choice in clinical settings and contributing to its widespread acceptance.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$447.5 Million

Forecast Value

$711.8 Million

CAGR

4.8%

By end user, hospitals emerged as the leading segment, capturing 46.2% of the market share in 2024. Hospitals play a pivotal role in diagnosing, managing, and treating pelvic floor disorders such as POP and stress urinary incontinence. These institutions offer both surgical and non-surgical pessary treatments, catering to patients with varying levels of severity. Their ability to handle complex cases and provide essential follow-up care further reinforces their dominance in the pessary market.

In the United States, the pessary market was valued at USD 169.7 million in 2024 and continues to show strong growth potential. The rise in pelvic disorders, alongside lifestyle-related health conditions like obesity, is driving the increasing demand for pessaries as effective, non-invasive treatment solutions. The expansion of healthcare access and ongoing efforts to raise awareness about pelvic health issues are contributing to the continued market growth across the country.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definitions

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Base estimates and calculations

1.3.1 Base year calculation

1.3.2 Key trends for market estimation

1.4 Forecast model

1.5 Primary research and validation

1.5.1 Primary sources

1.5.2 Data mining sources

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Increasing prevalence of pelvic organ prolapse and urinary incontinence

3.2.1.2 Growing awareness towards timely diagnosis and treatment

3.2.1.3 Increasing adoption of non-invasive treatment options

3.2.1.4 Growing government support in women health programs

3.2.2 Industry pitfalls and challenges

3.2.2.1 Social stigma and psychological barrier

3.2.2.2 Concerns related to risk of infections due to prolonged use

3.3 Growth potential analysis

3.4 Patent analysis

3.5 Gap analysis

3.6 Regulatory landscape

3.7 Technological landscape

3.8 Future market trends

3.9 Porter’s analysis

3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.3 Competitive analysis of major market players

4.4 Competitive positioning matrix

4.5 Strategy outlook

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

5.1 Key trends

5.2 Ring

5.3 Donut

5.4 Gellhorn

5.5 Other types

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

6.1 Key trends

6.2 Mild pelvic organ prolapse

6.3 Stress urinary incontinence

6.4 Severe pelvic organ prolapse

6.5 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

7.1 Key trends

7.2 Hospitals

7.3 Ambulatory surgical centers

7.4 Clinics

7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)