헤마토크리트 검사 기기 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Hematocrit Test Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1665279

리서치사:Global Market Insights Inc.

발행일:2024년 12월

페이지 정보:영문 140 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

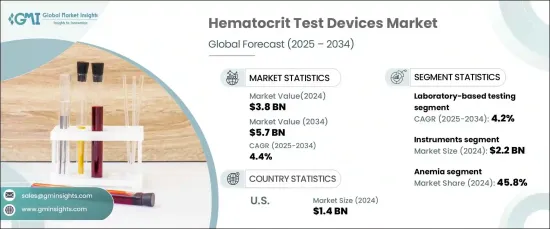

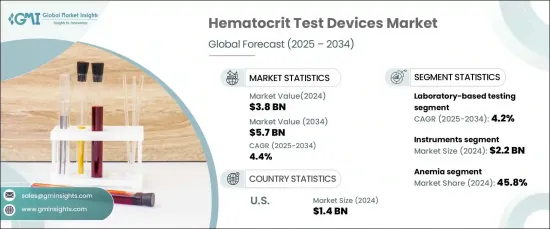

세계의 헤마토크리트 검사 기기 시장은 2024년에 38억 달러로 평가되었고, 2025년부터 2034년까지 CAGR 4.4%로 확대될 것으로 예측됩니다. 이러한 견조한 성장의 배경은 혈액 질환의 유병률 증가, 노인 인구 증가, 포인트 오브 케어 검사 기술의 지속적인 발전이 있습니다. 정확하고 효율적인 진단 도구에 대한 수요가 증가함에 따라, 헤마토크리트 검사 기기는 의료 제공의 중요한 구성 요소로 자리매김하고 있습니다.

시장은 장비, 시약, 소모품으로 구분되며, 헤마토크리트 검사 분석기와 미터를 포함한 장비 카테고리가 주도권을 잡고 있습니다. 2024년에는 이 부문이 22억 달러의 가장 높은 매출을 창출했습니다. 이러한 장비는 혈구 농도를 정기적으로 모니터링하는 데 필수적이며 의료 및 진단 측면 모두에서 필요성을 강조합니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

38억 달러

예측 금액

57억 달러

CAGR

4.4%

또한 시장은 실험실 기반 검사와 POC(Point of Care) 검사를 포함한 검사 유형별로 분류됩니다. 실험실 기반 검사는 지배적인 부문으로 부상했으며 2024년 매출은 25억 달러를 차지했습니다. 2025년부터 2034년까지의 CAGR은 4.2%로 예측되며, 정확하고 신뢰할 수 있는 결과를 제공할 수 있기 때문에 이 부문은 계속 번영하고 있습니다. 실험실 기반 헤마토크리트 검사 기기는 빈혈, 다혈증, 탈수 등 다양한 증상을 진단하는 데 필수적이며 의료 진단에 필수적인 도구입니다.

미국은 여전히 중요한 시장 진출 기업이며, 헤마토크리트 검사 기기는 2024년에 14억 달러의 매출을 올렸습니다. 이 부문은 2025년부터 2034년까지 CAGR 3.9%로 성장할 것으로 예측됩니다. 미국 인구에서의 빈혈, 겸상 적혈구증, 다혈증 등 혈액 질환의 유병률 증가는 신뢰성 있는 헤마토크리트 검사 기기에 대한 수요를 부추기고 있습니다. 이러한 기기의 채용은 임상과 재택치료에 걸쳐 있으며, 환자 모니터링과 관리에서 매우 중요한 역할을 담당합니다.

목차

제1장 조사 방법 및 조사 범위

제2장 주요 요약

제3장 산업 인사이트

생태계 분석

산업에 미치는 영향요인

성장 촉진요인

혈액 질환의 유병률 증가

포인트 오브 케어 검사에 대한 수요 증가

혈액학 검사에 있어서 기술의 진보

산업의 잠재적 리스크 및 과제

첨단 헤마토크리트 검사 기기의 고비용

성장 가능성 분석

규제 상황

기술

Porter's Five Forces 분석

PESTEL 분석

갭 분석

향후 시장 동향

밸류체인 분석

제4장 경쟁 구도

서문

기업 매트릭스 분석

기업 점유율 분석

주요 시장 진출기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략 대시보드

제5장 시장 추정 및 예측 : 제품별(2021-2034년)

주요 동향

기기

헤마토크리트 측정 분석기

헤마토크리트 측정 미터

시약 및 소모품

제6장 시장 추정 및 예측 : 모달리티별(2021-2034년)

주요 동향

실험실 기반 검사

포인트 오브 케어(POC) 검사

제7장 시장 추정 및 예측 : 용도별(2021-2034년)

주요 동향

빈혈

선천성 심장병

진성다혈증

기타

제8장 시장 추정 및 예측 : 최종 용도별(2021-2034년)

주요 동향

병원

진단 실험실

외래수술센터(ASC)

기타

제9장 시장 추정 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제10장 기업 프로파일

MENARINI Group

Abbott

BIO-RAD

Boule

Danaher

Diatron

EKF Diagnostics

Roche

HORIBA Medical

Mindray

NIHON KOHDEN

Nova Biomedical

SENSA CORE

SIEMENS Healthineers

Sysmex

AJY

영문 목차

영문목차

The Global Hematocrit Test Devices Market was valued at USD 3.8 billion in 2024 and is projected to expand at a CAGR of 4.4% from 2025 to 2034. This robust growth is driven by a rising prevalence of blood disorders, a growing aging population, and continuous advancements in point-of-care testing technologies. The increasing demand for precise and efficient diagnostic tools positions hematocrit test devices as a critical component in healthcare delivery.

The market is segmented into instruments, reagents, and consumables, with the instruments category-comprising hematocrit test analyzers and meters-leading the charge. In 2024, this segment generated the highest revenue of USD 2.2 billion. These devices are indispensable for the regular monitoring of blood cell concentrations, underscoring their necessity in both medical and diagnostic settings.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$3.8 Billion

Forecast Value

$5.7 Billion

CAGR

4.4%

Additionally, the market is categorized by testing type, including laboratory-based testing and point-of-care (POC) testing. Laboratory-based testing emerged as the dominant segment, accounting for USD 2.5 billion in revenue in 2024. With a projected CAGR of 4.2% from 2025 to 2034, this segment continues to thrive due to its ability to deliver highly precise and reliable results. Laboratory-based hematocrit testing devices are crucial for diagnosing a range of conditions, such as anemia, polycythemia, and dehydration, making them an essential tool in healthcare diagnostics.

The U.S. remains a significant market player, with hematocrit test devices generating USD 1.4 billion in revenue in 2024. This segment is forecasted to grow at a CAGR of 3.9% between 2025 and 2034. The increasing prevalence of blood disorders, such as anemia, sickle cell disease, and polycythemia, within the U.S. population fuels the demand for reliable hematocrit testing equipment. The adoption of these devices spans clinical and home healthcare settings, ensuring their pivotal role in patient monitoring and care.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definitions

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Base estimates and calculations

1.3.1 Base year calculation

1.3.2 Key trends for market estimation

1.4 Forecast model

1.5 Primary research and validation

1.5.1 Primary sources

1.5.2 Data mining sources

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Increasing prevalence of blood disorders

3.2.1.2 Growing demand for point-of-care testing

3.2.1.3 Technological advancements in hematology testing

3.2.2 Industry pitfalls and challenges

3.2.2.1 High cost of advanced hematocrit devices

3.3 Growth potential analysis

3.4 Regulatory landscape

3.5 Technology landscape

3.6 Porter’s analysis

3.7 PESTEL analysis

3.8 Gap analysis

3.9 Future market trends

3.10 Value chain analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company matrix analysis

4.3 Company market share analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

5.1 Key trends

5.2 Instruments

5.2.1 Hematocrit test analyzer

5.2.2 Hematocrit test meter

5.3 Reagents and consumables

Chapter 6 Market Estimates and Forecast, By Modality, 2021 – 2034 ($ Mn)

6.1 Key trends

6.2 Laboratory-based testing

6.3 Point-of-care (POC) testing

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

7.1 Key trends

7.2 Anemia

7.3 Congenital heart diseases

7.4 Polycythemia vera

7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

8.1 Key trends

8.2 Hospitals

8.3 Diagnostic laboratories

8.4 Ambulatory surgical centers

8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)