석유 및 가스용 클라우드 컴퓨팅 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Cloud Computing in Oil and Gas Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1665232

리서치사:Global Market Insights Inc.

발행일:2024년 12월

페이지 정보:영문 165 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

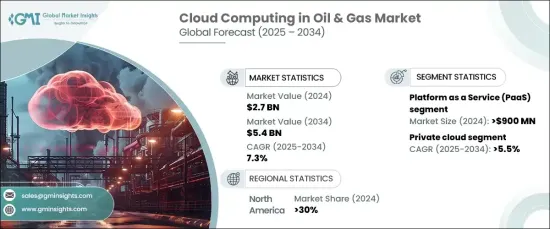

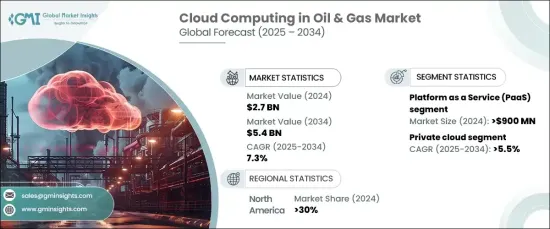

세계의 석유 및 가스용 클라우드 컴퓨팅 시장 규모는 2024년 27억 달러였고, 2025-2034년까지 CAGR 7.3%로 강력한 성장이 전망되고 있습니다.

이러한 성장의 배경에는 비즈니스 민첩성, 워크플로우 최적화, 데이터 액세스 강화에 대한 요구가 커지고 있습니다. 석유 및 가스 기업이 업무의 근대화에 노력하는 가운데 클라우드 기술을 통합함으로써 유연성이 향상되어 시장 변동에 신속하게 대응하고 보다 효율적인 자원 관리가 가능해집니다.

2024년 시장은 IaaS(Infrastructure-as-a-Service), PaaS(Platform-as-a-Service), SaaS(Software-as-a-Service)로 구분됩니다. 이 중 PaaS 시장 점유율은 9억 달러로 돌출하고 있습니다. 이 부문은 애플리케이션 개발 및 관리를 단순화하고 기본 인프라를 유지하는 복잡성을 없앨 수 있기 때문에 급속히 확대되고 있습니다. PaaS 솔루션을 채택함으로써 석유 및 가스 기업은 개발을 효율화하고 시장 개척까지의 시간을 단축하며 수요에 따라 자원을 쉽게 확장할 수 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

27억 달러

예측 금액

54억 달러

CAGR

7.3%

석유 및 가스용 클라우드 컴퓨팅은 퍼블릭, 프라이빗, 하이브리드 클라우드 솔루션과 같은 배포 모드에 따라 구분됩니다. 프라이빗 클라우드 부문은 2025-2034년까지 CAGR 5.5%로 안정적인 성장이 예상되고 있습니다. 이러한 성장을 이끌어내는 것은 민감한 데이터를 처리하는 기업에게 중요한 보안 기능을 강화한 프라이빗 클라우드 솔루션의 채택이 증가하고 있다는 것입니다. 프라이빗 클라우드의 도입으로 석유 및 가스 기업은 클라우드 기술의 확장성과 유연성의 혜택을 누리면서 데이터 프라이버시 관리를 강화할 수 있습니다. 이는 엄격한 규제 기준을 준수할 수 없는 산업에서 특히 중요합니다.

미국의 석유 및 가스용 클라우드 컴퓨팅 시장은 2024년에 30%의 점유율을 획득했습니다. 이 지역 전반에 걸쳐 클라우드 기술이 널리 채택되어 비즈니스 효율성이 크게 향상되고 비용이 절감됩니다. 미국의 주요 석유 및 가스 기업은 디지털 전환 전략의 일환으로 클라우드 인프라에 많은 투자를 하고 있습니다. 또한 지역의 강력한 규제 프레임 워크와 첨단 데이터 분석 솔루션에 대한 수요가 증가함에 따라 탐사에서 유통에 이르기까지 광범위한 석유 및 가스의 클라우드 컴퓨팅 통합이 가속화되고 있습니다.

목차

제1장 조사 방법과 조사 범위

조사 디자인

조사 접근

데이터 수집 방법

기본 추정과 계산

기준연도의 산출

시장 추정의 주요 동향

예측 모델

1차 조사와 검증

1차 정보

데이터 마이닝 소스

시장 범위와 정의

제2장 주요 요약

제3장 산업 인사이트

생태계 분석

공급자의 상황

소프트웨어 제공업체

서비스 제공업체

석유 및 가스 사업자

유통업체

최종 사용자

이익률 분석

기술 혁신의 상황

특허 분석

규제 상황

이용 사례

이용 사례 1

장점

투자수익률

이용 사례 2

이익

투자이익률

이용 사례

이용 사례 1

소비자명

과제

해결책

임팩트

이용 사례 2

소비자명

과제

해결책

임팩트

영향요인

성장 촉진요인

실시간 데이터 분석 및 모니터링에 대한 수요 증가

데이터 통찰에 의한 지속가능성의 향상과 환경 부하의 저감으로의 시프트

클라우드 기반 솔루션으로 업무 효율 향상

석유 및 가스 섹터용 디지털 전환에 대한 대처의 주목 고조

산업의 잠재적 리스크 및 과제

레거시 시스템과의 통합의 과제

데이터 프라이버시와 사이버 보안 위협에 대한 우려

성장 가능성 분석

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

소개

기업 점유율 분석

경쟁 포지셔닝 매트릭스

전략 전망 매트릭스

제5장 시장 추정·예측 : 서비스별, 2021-2034년

주요 동향

IaaS(Infrastructure-as-a-Servic)

PaaS(Platform-as-a-Service)

SaaS(Software-as-a-Service)

제6장 시장 추정·예측 : 전개 모드별, 2021-2034년

주요 동향

퍼블릭 클라우드

프라이빗 클라우드

하이브리드 클라우드

제7장 시장 추정·예측 : 운용별, 2021-2034년

주요 동향

업스트림

미드스트림

다운스트림

제8장 시장 추정·예측 : 용도별, 2021-2034년

주요 동향

데이터 보관 및 관리

자산 관리

콜라보레이션 커뮤니케이션 툴

원격 모니터링 및 제어

시뮬레이션과 모델링

기타

제9장 시장 추정·예측 : 최종 용도별, 2021-2034년

주요 동향

국영석유회사(NOC)

독립계 석유회사(IOC)

제10장 시장 추정·예측 : 지역별, 2021-2034년

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

러시아

북유럽

아시아태평양

중국

인도

일본

호주

한국

동남아시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

아랍에미리트(UAE)

남아프리카

사우디아라비아

제11장 기업 프로파일

ABB

Accenture

Amazon Web Services(AWS)

AVEVA

Baker Hughes

Cisco

Dassault Systemes

General Electric

Halliburton

Honeywell

IBM

Intel

Microsoft

Oracle

Rockwell Automation

SAP

Schlumberger

Siemens Energy

Tata Consultancy Services(TCS)

Yokogawa

JHS

영문 목차

영문목차

The Global Cloud Computing In Oil And Gas Market was valued at USD 2.7 billion in 2024 and is expected to experience robust growth at a CAGR of 7.3% from 2025 to 2034. This growth is fueled by the increasing need for operational agility, optimized workflows, and enhanced data access. As oil and gas companies strive to modernize their operations, integrating cloud technologies offers increased flexibility, enabling faster responses to market fluctuations and more efficient resource management.

In 2024, the market was divided into several key service offerings: Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS). Among these, the PaaS segment commanded a substantial market share, valued at USD 900 million. This segment is expanding rapidly due to its ability to simplify application development and management, eliminating the complexities of maintaining underlying infrastructure. By adopting PaaS solutions, oil and gas companies can streamline development, reduce time to market, and easily scale their resources according to demand.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$2.7 Billion

Forecast Value

$5.4 Billion

CAGR

7.3%

Cloud computing in the oil and gas sector is also segmented by deployment mode, including public, private, and hybrid cloud solutions. The private cloud segment is expected to grow steadily at a CAGR of 5.5% from 2025 to 2034. This growth is driven by the rising adoption of private cloud solutions, which offer enhanced security features crucial for companies handling sensitive data. With private cloud deployments, oil and gas firms can enjoy greater control over data privacy while benefiting from the scalability and flexibility of cloud technologies. This is particularly important in an industry where compliance with stringent regulatory standards is non-negotiable.

In the U.S., the cloud computing market for oil and gas captured a 30% share in 2024. The widespread adoption of cloud technologies across the region is significantly boosting operational efficiency and reducing costs. Major oil and gas companies in the U.S. are investing heavily in cloud infrastructure as part of their digital transformation strategies. Furthermore, the region's strong regulatory framework and increasing demand for advanced data analytics solutions are accelerating the integration of cloud computing across a wide range of oil and gas operations, from exploration to distribution.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Research design

1.1.1 Research approach

1.1.2 Data collection methods

1.2 Base estimates & calculations

1.2.1 Base year calculation

1.2.2 Key trends for market estimation

1.3 Forecast model

1.4 Primary research and validation

1.4.1 Primary sources

1.4.2 Data mining sources

1.5 Market scope & definition

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Supplier landscape

3.2.1 Software providers

3.2.2 Service providers

3.2.3 Oil & gas operators

3.2.4 Distributors

3.2.5 End users

3.3 Profit margin analysis

3.4 Technology & innovation landscape

3.5 Patent analysis

3.6 Regulatory landscape

3.7 Used cases

3.7.1 Used case 1

3.7.1.1 Benefits

3.7.1.2 ROI

3.7.2 Used case 2

3.7.2.1 Benefits

3.7.2.2 ROI

3.8 Case study

3.8.1 Case study 1

3.8.1.1 Consumer name

3.8.1.2 Challenge

3.8.1.3 Solution

3.8.1.4 Impact

3.8.2 Case study 2

3.8.2.1 Consumer name

3.8.2.2 Challenge

3.8.2.3 Solution

3.8.2.4 Impact

3.9 Impact forces

3.9.1 Growth drivers

3.9.1.1 Increasing demand for real-time data analytics and monitoring

3.9.1.2 Shift towards improving sustainability and reducing environmental impact through data insights

3.9.1.3 Enhanced operational efficiency through cloud-based solutions

3.9.1.4 Growing focus on digital transformation initiatives in the oil and gas sector

3.9.2 Industry pitfalls & challenges

3.9.2.1 Integration challenges with legacy systems

3.9.2.2 Concerns regarding data privacy and cybersecurity threats