자동차 프런트 및 리어 피지탈 쉴드 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Automotive Front and Rear Phygital Shield Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1665034

리서치사:Global Market Insights Inc.

발행일:2024년 12월

페이지 정보:영문 180 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

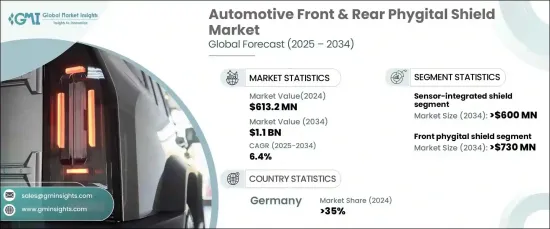

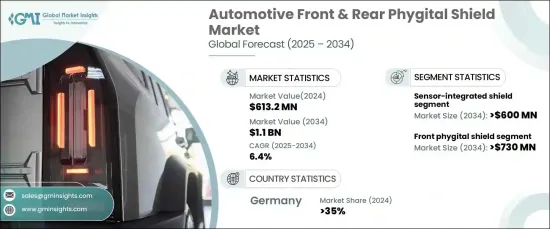

세계의 자동차 프런트 및 리어 피지탈 쉴드 시장은 2024년 6억 1,320만 달러로 평가되었으며, 2025년부터 2034년까지 6.4%의 연평균 복합 성장률(CAGR)로 견조하게 성장할 것으로 예측됩니다.

피지탈 쉴드는 LiDAR, 레이더, 카메라와 같은 최첨단 센서 시스템을 통합하는 데 중요한 구성 요소로 떠오르고 있으며, 자율 주행 차량과 커넥티드 자동차의 네비게이션, 통신 및 안전에 매우 중요합니다. 이 쉴드는 차량의 미관을 유지하면서 이러한 첨단 기술을 통합하기 위해 철저하게 설계되었으며 기능적 및 스타일적 요구 사항을 충족합니다.

시장은 제품 유형별로 프런트 피지탈 쉴드와 리어 피지탈 쉴드로 분류됩니다. 2024년에는 프런트 피지탈 쉴드가 시장의 65%를 차지했습니다. 이 분야는 2034년 전기차와 고급차에서 LED 및 디스플레이 대응 프런트 쉴드의 채용 확대로 7억 3,000만 달러에 달할 것으로 예측되고 있습니다. 이러한 첨단 쉴드는 적응형 조명 시스템 및 디지털 디스플레이와 같은 기능을 통합하여 동적 브랜딩, 시그널링, 커뮤니케이션 기능의 강화 등을 실현합니다.

시장 범위

시작년

2024년

예측연도

2025-2034년

시작금액

6억 1,320만 달러

예측 금액

11억 달러

CAGR

6.4%

기술 측면에서 시장은 센서 일체형 쉴드, LED/디스플레이 쉴드, 에어로다이나믹 쉴드로 분류됩니다. 센서 일체형 쉴드는 2034년까지 6억 달러를 창출할 것으로 예상되며 스마트 쉴드 기술의 급속한 진보를 보여줍니다. 이러한 쉴드에는 현재 차량의 중앙 시스템에 도달하기 전에 센서 데이터를 처리하는 전처리 기능이 있습니다. 분산 처리를 가능하게 함으로써, 대기 시간을 대폭 단축하고, 자율 주행 기능의 실시간 의사 결정을 강화합니다. 게다가 OTA(Over-the-Air) 업데이트를 지원하는 기능은 에지 컴퓨팅의 중시의 고조에 따르는 것으로, 자동차 제조업체가 센서 알고리즘을 원격으로 개량해, 지속적인 성능 향상을 확보할 수 있게 합니다.

독일은 2024년 세계 수요의 35%를 차지했습니다. 자동차 기술 혁신의 주요 거점인 독일은 수많은 고급 자동차 제조업체의 본거지이며, 첨단 피지탈 쉴드의 채용을 촉진하고 있습니다. 이러한 쉴드는 차선 유지 지원, 충돌 회피, 보행자 감지 등의 기능을 제공하는 ADAS(첨단 운전 지원 시스템)에 필수적인 센서나 카메라를 탑재하는데 있어서 필수적인 역할을 하고 있습니다. 자동차 부문에서 자동차의 안전성과 자율성에 대한 관심 증가는 이러한 기술적으로 정교한 쉴드 수요에 계속 박차를 가하고 있습니다.

보고서 내용

제1장 조사 방법과 조사 범위

조사 디자인

조사 접근

데이터 수집 방법

기본 추정과 계산

기준연도의 산출

시장추계의 주요 동향

예측 모델

1차 조사와 검증

1차 정보

데이터 마이닝 소스

시장 정의

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

부품 제조업체

Tier 1 공급업체

자동차 OEM

테크놀로지 인테그레이터

최종 사용자

이익률 분석

기술차별화 요인

센서 통합

LED 조명 및 디스플레이 시스템

공력 설계의 강화

기타

주요 뉴스와 대처

특허 분석

규제 상황

영향요인

성장 촉진요인

전기자동차의 보급

자율주행차와 커넥티드카의 성장

자동차 개인화에 대한 소비자 수요 증가

차체의 에어로 다이내믹스에 대한 주목의 고조

업계의 잠재적 위험 및 과제

높은 개발 비용

복잡한 제조 공정

성장 가능성 분석

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

소개

기업 점유율 분석

경쟁 포지셔닝 매트릭스

전략 전망 매트릭스

제5장 시장 추계·예측 : 제품별, 2021-2034년

주요 동향

프런트 피지탈 쉴드

리어 피지탈 쉴드

제6장 시장 추계·예측 : 차량별, 2021-2034년

주요 동향

승용차

해치백

세단

SUV

상용차

소형 상용차(LCV)

대형 상용차(HCV)

제7장 시장 추계·예측 : 기술별, 2021-2032년

주요 동향

센서 일체형 쉴드

LED/디스플레이

에어로다이나믹

제8장 시장 추계·예측 : 재료별, 2021-2032년

주요 동향

플라스틱/폴리머 베이스

금속 베이스

합성

제9장 시장 추계·예측 : 판매 채널별, 2021-2032년

주요 동향

OEM

애프터마켓

제10장 시장 추계·예측 : 지역별, 2021-2032년

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

스페인

이탈리아

러시아

북유럽

아시아태평양

중국

인도

일본

한국

뉴질랜드

동남아시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

UAE

남아프리카

사우디아라비아

제11장 기업 프로파일

Covestro

Forvia Hella

Harman

Hyundai Mobis

Infineon

Intops

Kia

Magna

Marelli

Motherson

Niebling

Plastic Omnium

Prolim

Texas Instruments

Valeo

JHS

영문 목차

영문목차

The Global Automotive Front And Rear Phygital Shield Market was valued at USD 613.2 million in 2024 and is projected to grow at a robust CAGR of 6.4% from 2025 to 2034. Phygital shields have emerged as a critical component in the integration of cutting-edge sensor systems such as LiDAR, radar, and cameras, which are pivotal for the navigation, communication, and safety of autonomous and connected vehicles. These shields are meticulously designed to incorporate these advanced technologies while maintaining the vehicle's aesthetic appeal, meeting both functional and stylistic demands.

The market is segmented by product type into front phygital shields and rear phygital shields. In 2024, front phygital shields held the lion's share, accounting for 65% of the market. This segment is anticipated to reach USD 730 million by 2034, driven by the growing adoption of LED and display-enabled front shields in electric and luxury vehicles. These advanced shields incorporate features such as adaptive lighting systems and digital displays, which provide dynamic branding, signaling, and enhanced communication capabilities-key differentiators in modern automotive design.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$613.2 Million

Forecast Value

$1.1 Billion

CAGR

6.4%

On the technology front, the market is categorized into sensor-integrated shields, LED/display shields, and aerodynamic shields. Sensor-integrated shields are forecasted to generate USD 600 million by 2034, showcasing rapid advancements in smart shield technology. These shields now feature preprocessing capabilities that handle sensor data before it reaches the vehicle's central systems. By enabling distributed processing, they significantly reduce latency and enhance real-time decision-making for autonomous driving features. Furthermore, the ability to support over-the-air (OTA) updates aligns with the growing emphasis on edge computing, enabling automakers to refine sensor algorithms remotely and ensure continuous performance enhancements.

Germany represented a significant share of the market in 2024, accounting for 35% of the global demand. As a leading hub for automotive innovation, the country is home to numerous premium automotive manufacturers driving the adoption of advanced phygital shields. These shields play an integral role in housing sensors and cameras essential for Advanced Driver Assistance Systems (ADAS), which power features like lane-keeping assistance, collision avoidance, and pedestrian detection. The rising focus on vehicle safety and autonomy in the automotive sector continues to fuel the demand for these technologically sophisticated shields.

Report Content

Chapter 1 Methodology & Scope

1.1 Research design

1.1.1 Research approach

1.1.2 Data collection methods

1.2 Base estimates and calculations

1.2.1 Base year calculation

1.2.2 Key trends for market estimates

1.3 Forecast model

1.4 Primary research & validation

1.4.1 Primary sources

1.4.2 Data mining sources

1.5 Market definitions

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2032

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Supplier landscape

3.2.1 Component manufacturers

3.2.2 Tier-1 suppliers

3.2.3 Automotive OEM

3.2.4 Technology integrators

3.2.5 End users

3.3 Profit margin analysis

3.4 Technology differentiators

3.4.1 Sensor integration

3.4.2 LED lighting and display systems

3.4.3 Aerodynamic design enhancements

3.4.4 Others

3.5 Key news & initiatives

3.6 Patent analysis

3.7 Regulatory landscape

3.8 Impact forces

3.8.1 Growth drivers

3.8.1.1 Rise in electric vehicle adoption

3.8.1.2 Growth of autonomous and connected vehicles

3.8.1.3 Growing consumer demand for vehicle personalization

3.8.1.4 Growing focus on aerodynamics of vehicle body