자동차용 브레이크 부스터 및 마스터 실린더 시장 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)

Automotive Brake Booster and Master Cylinder Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1665025

리서치사:Global Market Insights Inc.

발행일:2024년 12월

페이지 정보:영문 180 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

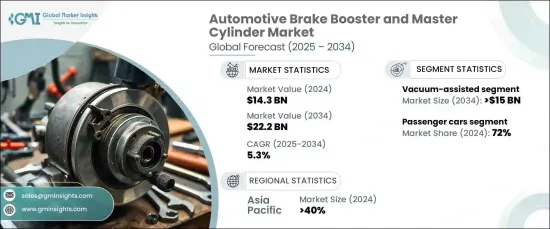

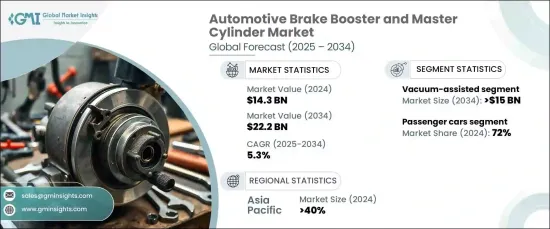

자동차용 브레이크 부스터 및 마스터 실린더 세계 시장은 2024년에 143억 달러로 평가되었으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 5.3%를 나타낼 것으로 예상됩니다.

이 시장 성장은 첨단 브레이크 시스템을 필요로 하는 전기자동차와 자율주행차의 채용이 증가하고 있는 것이 큰 요인이 되고 있습니다. 전기자동차(EV)는 전기 브레이크 부스터 수요 급증에 기여하고 있습니다. 기존의 브레이크 시스템은 엔진의 진공에 의존하지만 EV에는 이 기능이 없기 때문입니다.

동시에 세계 각국의 정부가 안전 규제를 강화하고 있기 때문에 고급 브레이크 솔루션에 대한 수요가 더욱 높아지고 있습니다. 이러한 규제는 안전성을 높이고 사고를 줄이고 사망자를 최소화하기 위해 신차와 개장 모델 모두에 고급 브레이크 시스템을 통합하는 것을 뒷받침합니다. 북미, 유럽, 아시아태평양의 일부 등 주요 지역에서 규제 준수가 중시되고 있는 것이 이러한 기술의 채용을 촉진하는 주요 요인이 되어 시장의 성장을 뒷받침하고 있습니다.

시장 범위

시작연도

2024

예측연도

2025-2034

시작금액

143억 달러

예측 금액

222억 달러

CAGR

5.3%

브레이크 부스터 시장은 진공 어시스트, 유압 어시스트, 전자 브레이크의 세 가지 주요 기술로 분류됩니다. 진공 어시스트 브레이크 부스터는 2024년 최대 점유율을 차지하며 시장의 65%를 차지했습니다. 이 기술은 2034년까지 150억 달러에 달할 것으로 예상됩니다. 진공 보조 부스터는 비용 효율성과 효율성으로 인해 승용차와 소형 상용차에 선호됩니다. 엔진의 진공을 이용하여 제동력을 높이는 것으로, 이러한 부스터는 신뢰성과 내연 엔진과의 호환성을 제공해, 종래의 차종에 이상적인 선택이 되고 있습니다.

차종별로는 승용차가 자동차용 브레이크 부스터와 마스터 실린더 시장을 독점하고 있으며, 2024년 시장 점유율 전체의 72%를 차지했습니다. 이 리더십은 세계적으로 승용차의 생산 및 판매 대수가 많은 것에 기인하고 있습니다. 승용차 부문에는 세단, SUV, 해치백 등 광범위한 승용차가 포함되어 있으며, 이들 모두 시장 전체의 성장에 중요한 역할을 합니다.

아시아태평양은 2024년 시장 점유율의 40%를 차지했으며, 2034년까지 95억 달러를 창출할 것으로 예상됩니다. 이 지역의 주요 국가인 중국은 2034년까지 40억 달러 규모의 시장 공헌이 예상됩니다. 승용차와 상용차의 엄청난 생산과 소비로 중국은 세계 자동차 산업에서 지배적인 역할을 하고 있으며, 첨단 브레이크 기술에 대한 큰 수요를 계속 견인하고 있습니다. 중국과 아시아태평양의 자동차 시장이 확대됨에 따라 고품질의 효율적인 브레이크 시스템에 대한 요구가 점점 커지고 있습니다.

목차

제1장 조사 방법과 조사 범위

조사 디자인

조사 접근

데이터 수집 방법

기본 추정과 계산

기준연도의 산출

시장추계의 주요 동향

예측 모델

1차 조사와 검증

1차 정보

데이터 마이닝 소스

시장 정의

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

원재료 공급자

부품 제조업체

브레이크 부스터 및 마스터 실린더 제조업체

자동차 부품 공급업체

오리지널 제품 제조업체(OEM)

이익률 분석

코스트 내역 분석

기술 혁신의 전망

주요 뉴스 및 이니셔티브

규제 상황

영향요인

성장 촉진요인

EV와 자율주행차의 보급 확대

교통안전에 대한 의식의 고조와 선진 브레이크 시스템에 대한 규제의 의무화

전동 브레이크 부스터 등의 기술 혁신의 진전

신흥 시장에서의 자동차 생산 증가

업계의 잠재적 위험 및 과제

첨단 기술의 고비용

신흥 경제 국가 시장 포화

성장 가능성 분석

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

소개

기업 점유율 분석

경쟁 포지셔닝 매트릭스

전략 전망 매트릭스

제5장 시장 추정 및 예측 : 컴포넌트별, 2021-2034년

주요 동향

브레이크 부스터

진공 브레이크 부스터

유압식 브레이크 부스터

마스터 실린더

탠덤 마스터 실린더

싱글 마스터 실린더

제6장 시장 추정 및 예측 : 추진력별, 2021-2034년

주요 동향

ICE

전기자동차

배터리 전기자동차(BEV)

플러그인 하이브리드 자동차(PHEV)

하이브리드 전기자동차(HEV)

제7장 시장 추정 및 예측 : 2021-2034년, 차량별

주요 동향

승용차

해치백

세단

SUV

상용차

소형 상용차(LCV)

대형 상용차(HCV)

제8장 시장 추정 및 예측 : 기술별, 2021-2034년

주요 동향

진공 어시스트

유압 어시스트

전자식 브레이크 부스터

제9장 시장 추정 및 예측 : 판매 채널별, 2021-2034년

주요 동향

OEM

애프터마켓

제10장 시장 추정 및 예측 : 지역별, 2021-2034년

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

스페인

이탈리아

러시아

북유럽

아시아태평양

중국

인도

일본

한국

뉴질랜드

동남아시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

UAE

남아프리카

사우디아라비아

제11장 기업 프로파일

ADVICS Co.

Aisin

Akebono Brake Industry

Brembo

Cardone Industries

Continental

DENSO

Federal-Mogul Holdings Corporation

Haldex

Hitachi Astemo

현대모비스

Knorr-Bremse

KYB

Magneti Marelli

Mando

Nissin Kogyo

Robert Bosch

Tenneco

TRW Automotive

ZF Friedrichshafen

SHW

영문 목차

영문목차

The Global Automotive Brake Booster And Master Cylinder Market was valued at USD 14.3 billion in 2024 and is expected to experience significant growth, projected to expand at a CAGR of 5.3% from 2025 to 2034. This market growth is largely driven by the increasing adoption of electric and autonomous vehicles, which require advanced braking systems. Electric vehicles (EVs) are contributing to a surge in demand for electric brake boosters, as traditional braking systems rely on engine vacuum-a feature that EVs do not have.

At the same time, governments worldwide are tightening safety regulations, which is further boosting the demand for sophisticated braking solutions. These regulations are pushing the integration of advanced braking systems in both new vehicles and retrofitted models to enhance safety, reduce accidents, and minimize fatalities. The emphasis on regulatory compliance in key regions such as North America, Europe, and parts of Asia-Pacific is a major factor driving the adoption of these technologies, thereby fueling market growth.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$14.3 Billion

Forecast Value

$22.2 Billion

CAGR

5.3%

The market is divided into three primary brake booster technologies: vacuum-assisted, hydraulic-assisted, and electronic brake boosters. Vacuum-assisted brake boosters held the largest share in 2024, accounting for 65% of the market. This technology is expected to reach USD 15 billion by 2034. Vacuum-assisted boosters are the preferred choice for passenger and light commercial vehicles due to their cost-effectiveness and efficiency. By utilizing the engine's vacuum to enhance braking force, these boosters offer reliability and compatibility with internal combustion engines, making them an ideal option for traditional vehicle models.

In terms of vehicle type, passenger cars dominate the automotive brake booster and master cylinder market, representing 72% of the total market share in 2024. This leadership is attributed to the high production and sales volumes of passenger vehicles globally. The passenger car segment includes a wide range of personal vehicles, including sedans, SUVs, and hatchbacks, all of which play a vital role in the market's overall growth.

The Asia-Pacific region accounted for 40% of the market share in 2024 and is expected to generate USD 9.5 billion by 2034. China, as the leading country in this region, is forecast to contribute USD 4 billion to the market by 2034. China's dominant role in the global automotive industry, with its vast production and consumption of both passenger and commercial vehicles, continues to drive substantial demand for advanced braking technologies. As the automotive market in China and the Asia-Pacific region expands, the need for high-quality, efficient braking systems will only continue to grow.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Research design

1.1.1 Research approach

1.1.2 Data collection methods

1.2 Base estimates and calculations

1.2.1 Base year calculation

1.2.2 Key trends for market estimates

1.3 Forecast model

1.4 Primary research & validation

1.4.1 Primary sources

1.4.2 Data mining sources

1.5 Market definitions

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Supplier landscape

3.2.1 Raw material suppliers

3.2.2 Component manufacturers

3.2.3 Brake booster and master cylinder manufacturers

3.2.4 Tier-1 automotive suppliers

3.2.5 Original equipment manufacturers (OEMs)

3.3 Profit margin analysis

3.4 Cost breakdown analysis

3.5 Technology & innovation landscape

3.6 Key news & initiatives

3.7 Regulatory landscape

3.8 Impact forces

3.8.1 Growth drivers

3.8.1.1 The rising adoption of EVs and autonomous vehicles

3.8.1.2 Growing awareness about road safety and regulatory mandates for advanced braking systems

3.8.1.3 Technological advancements in innovations such as electric brake boosters

3.8.1.4 Growing vehicle production in emerging markets