Refrigeration System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2024 - 2032

상품코드:1664877

리서치사:Global Market Insights Inc.

발행일:2024년 12월

페이지 정보:영문 220 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

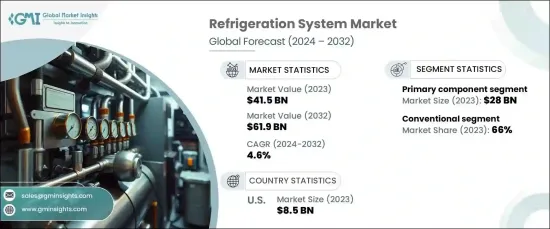

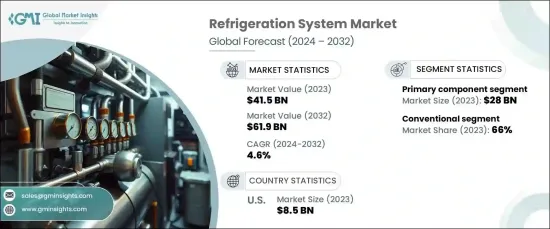

세계의 냉동 시스템 시장은 2023년에 415억 달러로 평가되었고, 2024년부터 2032년에 걸쳐 4.6%의 안정된 CAGR로 성장할 것으로 예측되고 있습니다.

이 성장의 원동력이 되고 있는 것은 식품 및 음료, 의약품, 화학 등, 신뢰성이 높은 냉동이 제품 보존이나 규제 준수에 중요한 역할을 하는 주요 산업에 있어서 수요 증가입니다. 최첨단 기술의 발전과 에너지 효율적인 냉동 솔루션으로의 전환은 시장을 더욱 발전시키고 있습니다.

냉동 시스템 시장은 1차 부품과 보조 부품으로 구분됩니다. 2023년 1차 부품 부문은 280억 달러를 차지했으며 2032년까지 연평균 복합 성장률(CAGR) 4.7%로 성장할 것으로 예측됩니다. 이 부문의 주도적 위치는 효율적인 냉동 사이클을 보장하기 위해 압축기, 증발기 및 응축기가 필수적인 역할을 하기 때문입니다. 모든 냉동 시스템의 심장부인 컴프레서는 에너지 소비의 대부분을 차지하고 있으며, 성능 향상과 에너지 비용 절감을 위한 지속적인 기술 혁신에 박차를 가하고 있습니다. 한편, 증발기와 콘덴서는 열전달에서 매우 중요한 역할을 하며 일관된 온도 제어와 신뢰성 있는 시스템 성능을 보장합니다.

시장 범위

시작 연도

2023년

예측 연도

2024-2032년

시작 금액

415억 달러

예측 금액

619억 달러

CAGR

4.6%

냉장 유형에 따라 시장은 기존 시스템과 스마트 시스템으로 분류됩니다. 전통적인 냉동 시스템은 2023년에 66% 시장 점유율을 차지했으며, 2032년에는 404억 달러에 이를 것으로 예측됩니다. 보급의 원동력은 합리적인 가격과 낮은 유지 보수 요구 사항이며, 특히 비용에 민감한 시장에서 중소기업에게 선호되는 선택입니다. 다른 혜택으로 기존 시스템에는 확립된 공급망과 기술적 전문 지식이 있어 원활한 배포가 가능합니다. 기술 인프라가 개발되지 않은 지역에서는 스마트 냉동 기술이 아직 널리 보급되지 않을 수 있는 고급 프레임워크를 필요로 하기 때문에 이러한 시스템에 크게 의존합니다.

북미의 냉동 시스템 시장은 미국이 선도하고 있고, 2023년의 평가액은 85억 달러였으며, 2032년까지의 CAGR은 4.6%로 예상되고 있습니다. 미국 시장의 우위성은 제품의 품질과 엄격한 규제에 대응하기 위해 냉장을 우선하는 강력한 산업·상업 부문에 지지되고 있습니다. 이 나라의 확립된 콜드체인 네트워크, 엄격한 식품 안전 기준, 의약품 보관은 추가 성장 촉진요인입니다.

목차

제1장 조사 방법과 조사 범위

시장 범위와 정의

기본 추정과 계산

예측 계산

데이터 소스

1차

2차

유료 소스

공개 소스

제2장 주요 요약

제3장 업계 인사이트

업계 생태계 분석

밸류체인에 영향을 주는 요인

이익률 분석

방해

향후 전망

제조업체

유통업체

공급자의 상황

이익률 분석

주요 뉴스와 대처

규제 상황

영향요인

성장 촉진요인

높아지는 환경 규제와 지속가능성에의 대처

기술의 진보와 저GWP 냉매로의 시프트 증가

콜드체인 물류에 대한 수요 증가

업계의 잠재적 리스크·과제

높은 초기 투자 및 운영 비용

기술적 장애물과 안전성에 대한 배려

기술 개요

성장 가능성 분석

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

경쟁 포지셔닝 매트릭스

전략 전망 매트릭스

제5장 시장 추계·예측 : 구성 요소별(2021-2032년), 10억 달러

주요 동향

주요 부품

컴프레서

왕복동 컴프레서

스크류 컴프레서

원심식 컴프레서

스크롤 컴프레서

콘덴서

공랭식 콘덴서

수랭식 콘덴서

증발식 콘덴서

증발기

플레이트 증발기

튜브 증발기

핀형 증발기

제어 시스템

보조 구성 요소

솔레노이드 밸브

압력 조절기

고압 조절기

저압 조절기

필터

열교환기

판형 열교환기

쉘&튜브 열교환기

핀형 열교환기

팽창 밸브

기타

제6장 시장 추계·예측 : 냉동 카테고리별(2021-2032년), 10억 달러

주요 동향

스마트

기존

제7장 시장 추계·예측 : 용도별(2021-2032년), 10억 달러

주요 동향

상업

하이퍼마켓 및 슈퍼마켓/식품 소매업

접객

의료시설

기타(엔터테인먼트·레저, 꽃집 등)

산업

식품 및 음료 가공

화학제품 및 석유화학제품

제약

전자 및 기타 제조업

냉장 창고

에너지·유틸리티

기타(야금, 반도체 등)

운수

트럭 냉장

컨테이너 운송

해상선박

기타(항공우주 시스템, 철도 운송 등)

제8장 시장 추계·예측 : 사용자별(2021-2032년), 10억 달러

주요 동향

OEM

건설업자

유통업체

제9장 시장 추계·예측 : 유통 채널별(2021-2032년), 10억 달러

주요 동향

직접 판매

간접 판매

제10장 시장 추계·예측 : 지역별(2021-2032년), 10억 달러

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

네덜란드

폴란드

포르투갈

러시아

덴마크

스웨덴

헝가리

기타 유럽

아시아태평양

중국

일본

인도

한국

호주

인도네시아

기타 아시아태평양

라틴아메리카

브라질

멕시코

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

아랍에미리트(UAE)

남아프리카

기타 중동 및 아프리카

제11장 기업 프로파일

BITZER Kühlmaschinenbau GmbH

Carrier Global Corporation

Daikin Industries Ltd.

Danfoss A/S

Dorin

Embraco(Nidec Corporation)

Emerson Electric Co.

Frick India Limited

GEA

Grundfos

Hitachi

Hussmann Corporation

Ingersoll-Rand, Plc.

Johnson Controls

Lennox International

Tecumseh Products Company

KTH

영문 목차

영문목차

The Global Refrigeration System Market was valued at USD 41.5 billion in 2023 and is projected to grow at a steady CAGR of 4.6% from 2024 to 2032. This growth is fueled by increasing demand across key industries such as food and beverage, pharmaceuticals, and chemicals, where reliable refrigeration plays a critical role in product preservation and regulatory compliance. Advancements in cutting-edge technologies and the shift toward energy-efficient refrigeration solutions are further driving the market forward.

The refrigeration system market is segmented into primary and auxiliary components. In 2023, the primary component segment accounted for USD 28 billion and is forecasted to grow at a CAGR of 4.7% through 2032. This segment's leading position is attributed to the indispensable roles of compressors, evaporators, and condensers in ensuring efficient refrigeration cycles. Compressors, the heart of any refrigeration system, dominate energy consumption, spurring ongoing innovations to boost performance and reduce energy costs. Meanwhile, evaporators and condensers play a pivotal role in heat transfer, ensuring consistent temperature control and reliable system performance.

Market Scope

Start Year

2023

Forecast Year

2024-2032

Start Value

$41.5 Billion

Forecast Value

$61.9 Billion

CAGR

4.6%

Based on refrigeration type, the market is categorized into conventional and smart systems. Conventional refrigeration systems held a 66% market share in 2023 and are projected to reach USD 40.4 billion by 2032. Their widespread adoption is driven by affordability and low maintenance requirements, making them a preferred option for small and medium-sized enterprises, especially in cost-sensitive markets. Additionally, conventional systems benefit from established supply chains and technical expertise, enabling seamless implementation. Regions with underdeveloped technological infrastructure often rely heavily on these systems, as smart refrigeration technologies require advanced frameworks that may not yet be widely accessible.

The United States leads the refrigeration system market in North America, with a valuation of USD 8.5 billion in 2023 and an anticipated CAGR of 4.6% through 2032. The dominance of the U.S. market is underpinned by its strong industrial and commercial sectors, which prioritize refrigeration for product quality and compliance with stringent regulations. The country's well-established cold chain network, strict food safety standards, and pharmaceutical storage are additional growth drivers.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope & definitions

1.2 Base estimates & calculations

1.3 Forecast calculations

1.4 Data sources

1.4.1 Primary

1.4.2 Secondary

1.4.2.1 Paid sources

1.4.2.2 Public sources

Chapter 2 Executive Summary

2.1 Industry synopsis, 2021-2032

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Factor affecting the value chain

3.1.2 Profit margin analysis

3.1.3 Disruptions

3.1.4 Future outlook

3.1.5 Manufacturers

3.1.6 Distributors

3.2 Supplier landscape

3.3 Profit margin analysis

3.4 Key news & initiatives

3.5 Regulatory landscape

3.6 Impact forces

3.6.1 Growth drivers

3.6.1.1 Growing environmental regulations and sustainability initiatives

3.6.1.2 Technological progress and increasing shift towards low-GWP refrigerants

3.6.1.3 Rising demand for cold chain logistics

3.6.2 Industry pitfalls & challenges

3.6.2.1 High initial investment and operational costs

3.6.2.2 Technical hurdles and safety considerations