우주 착륙선 및 로버 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2026-2035년)

Space lander and Rover Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1913420

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 180 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

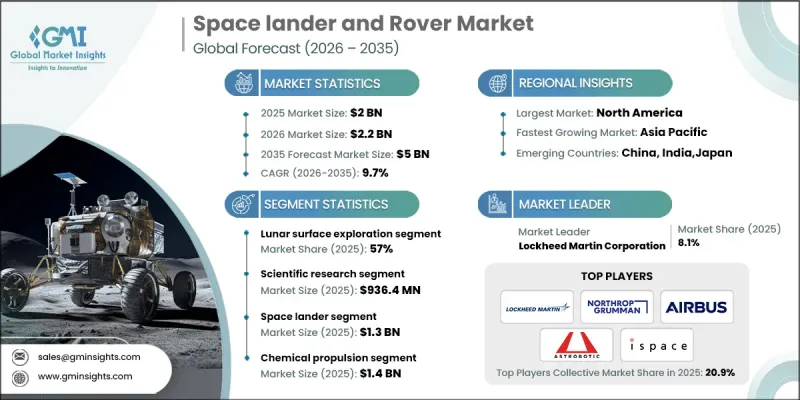

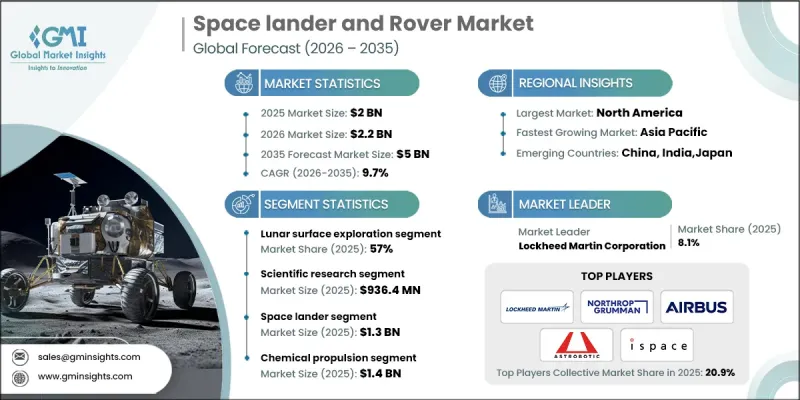

세계의 우주 착륙선 및 로버 시장 규모는 2025년에 20억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 9.7%로 성장할 전망이며, 50억 달러에 이를 것으로 예측됩니다.

이 성장은 행성 탐사 미션에 대한 세계의 관심 증가 및 자율 이동, 항법, 로봇 시스템의 지속적인 진보에 의해 지원되고 있습니다. 정부 및 민간 조직은 지구외 탐사 목표를 향한 장기 자금 제공을 강화하고 있으며, 이것이 선진적인 지표 탐사 플랫폼 수요를 견인하고 있습니다. 민간 부문의 참여 확대는 혁신주기를 가속화하고, 가볍고 고성능이며, 비용 효율적인 착륙선 및 로버 개발을 촉진합니다. 탑재형 지능, 내구성, 에너지 효율에 있어서 기술적 진보가 시장의 기세를 더욱 강화하고 있습니다. 탐사의 야망이 단기 임무를 넘어 확대됨에 따라 가혹한 환경에서 작동할 수 있는 신뢰할 수 있는 시스템에 대한 수요가 증가하고 있습니다. 이 진화하는 상황은 제조업체에게 장기 미션 및 장래의 인프라 개발을 지원하는 적응성이 높은 플랫폼의 개발을 촉구하고 있으며, 세계 시장 전체에서의 꾸준한 성장을 뒷받침하고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 시 금액

20억 달러

예측 금액

50억 달러

CAGR

9.7%

월면 탐사 부문은 2025년에 57%의 점유율을 차지했습니다. 이 부문은 가혹한 지표 환경 하에서 효율적으로 가동할 수 있는 자율 시스템 수요 증가로 이익을 얻고 있습니다. 제조업체 각사는 지속적인 월면 미션을 지원하면서 비용 효율 및 운용 신뢰성을 유지하도록 설계된 선진적인 이동 플랫폼 및 자원 이용 기술을 우선적으로 개발하고 있습니다.

과학 연구 부문은 2025년 9억 3,640만 달러 시장 규모를 창출했습니다. 이 부문의 성장은 탐사 임무에 대한 투자 증가 및 행성 표면으로부터 정확한 과학 데이터에 대한 수요 증가로 인한 것입니다. 제조업체는 진화하는 연구 목표를 충족시키기 위해 고정밀 측정 장비, 견고한 데이터 수집 시스템 및 적응성이 높은 미션 아키텍처 개발에 주력하고 있습니다.

북미의 우주 착륙선 및 로버 시장은 2025년에 48%의 점유율을 차지했습니다. 이 지역 우위는 강력한 공적 자금, 민간 우주 기업과의 연계 강화, 미션 성능 향상 및 운영 비용 절감을 목표로 하는 자율 기술의 급속한 발전에 의해 지원되고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

업계 생태계 분석

공급자의 상황

이익률

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

월면 및 화성 탐사 미션에 대한 세계 관심 고조

자율 항행 및 모빌리티 시스템에 있어서 기술적 진보

민간 부문에 의한 우주 탐사 기술에 대한 투자 및 확대

정부에 의한 장기적인 월면 및 화성 식민 계획에 대한 대처

우주 탐사를 위한 현지 자원 이용(ISRU) 능력 개발

업계의 잠재적 위험 및 과제

높은 개발 비용 및 기술적 복잡성

가혹한 우주 환경에 의한 미션 실패의 위험

시장 기회

지속 가능한 우주 거주 시설 개발

자율형 탐사 기술의 진전

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술 및 혁신 동향

현재 기술 동향

신흥 기술

신흥 비즈니스 모델

컴플라이언스 요건

방위 예산 분석

세계의 방위 지출 동향

지역별 방위 예산 배분

북미

유럽

아시아태평양

중동 및 아프리카

라틴아메리카

주요 방위 근대화 프로그램

예산 예측(2026-2035년)

업계 성장에 미치는 영향

국가별 방위 예산

부문별 방위 예산 배분

인원

운용 및 보수

조달

연구개발 및 시험 평가

인프라 및 건설

기술 및 혁신

공급망 탄력

지정학적 분석

노동력 분석

디지털 전환

합병, 인수 및 전략적 제휴의 동향

위험 평가 및 관리

주요 계약 수여(2022-2025년)

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

시장 집중도 분석

주요 기업의 경쟁 벤치마킹

재무 실적 비교

수익

이익률

연구개발

제품 포트폴리오 비교

제품 라인의 폭

기술

혁신

지리적 존재 비교

세계 전개 분석

서비스 네트워크 커버율

지역별 시장 침투율

경쟁 포지셔닝 매트릭스

리더

챌린저

팔로워

틈새 기업

전략적 전망 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

기술적 진보

사업 확대 및 투자 전략

지속가능성에 대한 노력

디지털 전환의 대처

신흥 및 스타트업 경쟁의 동향

제5장 시장 추계 및 예측 : 미션 유형별(2022-2035년)

월면 탐사

화성 표면 탐사

소행성 및 혜성 탐사

제6장 시장 추계 및 예측 : 차량 유형별(2022-2035년)

스페이스 랜더

스페이스 라로바

제7장 시장 추계 및 예측 : 추진 방식별(2022-2035년)

화학 추진

전기추진 및 이온추진

하이브리드 추진 시스템

제8장 시장 추계 및 예측 : 용도별(2022-2035년)

화학 추진

전기추진 및 이온추진

하이브리드 추진 시스템

제9장 시장 추계 및 예측 : 최종 용도별(2022-2035년)

정부 및 방위기관

우주 탐사 기관

민간 항공 우주 기업

연구기관

제10장 시장 추계 및 예측 : 지역별(2022-2035년)

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

인도

일본

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제11장 기업 프로파일

세계 주요 기업

Lockheed Martin Corporation

Northrop Grumman Corporation

NASA

Roscosmos

Airbus SE

지역의 주요 기업

북미

Blue Origin

Canadian Space Agency

아시아태평양

ISRO

Japan Aerospace Exploration Agency(JAXA)

China Academy of Space Technology

유럽

European Space Agency

Spacebit Technologies

틈새 기업 및 디스럽터

Astrobotic Technology

ispace, inc.

AJY

영문 목차

영문목차

The Global Space lander and Rover Market was valued at USD 2 billion in 2025 and is estimated to grow at a CAGR of 9.7% to reach USD 5 billion by 2035.

Growth is supported by rising worldwide focus on planetary exploration missions and continuous progress in autonomous mobility, navigation, and robotic systems. Governments and private organizations are increasingly committing long-term funding toward off-Earth exploration goals, which is driving demand for advanced surface exploration platforms. Expanding private sector participation is accelerating innovation cycles, encouraging the development of lighter, more capable, and cost-efficient landers and rovers. Technological improvements in onboard intelligence, durability, and energy efficiency are further strengthening market momentum. As exploration ambitions extend beyond short-term missions, the need for reliable systems capable of operating in extreme environments continues to increase. This evolving landscape is pushing manufacturers to develop adaptable platforms that support extended missions and future infrastructure development, reinforcing steady growth across the global market.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$2 Billion

Forecast Value

$5 Billion

CAGR

9.7%

The lunar surface exploration segment accounted for 57% share in 2025. This segment benefits from the growing demand for autonomous systems capable of operating efficiently in harsh surface conditions. Manufacturers are prioritizing advanced mobility platforms and resource utilization technologies designed to support sustained lunar missions while maintaining cost efficiency and operational reliability.

The scientific research segment generated USD 936.4 million in 2025. Growth in this segment is driven by increased investment in exploration missions and the expanding need for accurate scientific data from planetary surfaces. Manufacturers are focusing on high-precision instruments, robust data collection systems, and adaptable mission architectures to meet evolving research objectives.

North America Space lander and Rover Market held a 48% share in 2025. Regional dominance is supported by strong public funding, increasing collaboration with private space companies, and rapid development of autonomous technologies aimed at improving mission performance and lowering operational expenses.

Key players operating in the Global Space lander and Rover Market include Lockheed Martin Corporation, Airbus SE, Northrop Grumman Corporation, Blue Origin, Roscosmos, ISRO, European Space Agency, Canadian Space Agency, Japan Aerospace Exploration Agency (JAXA), China Academy of Space Technology, Spacebit Technologies, Astrobotic Technology, ispace, inc., and NASA. Companies in the Global Space lander and Rover Market strengthen their competitive position through sustained investment in advanced robotics, autonomous navigation, and modular spacecraft design. Manufacturers focus on developing versatile platforms that can support multiple mission profiles while reducing overall system weight and complexity. Strategic collaboration with government agencies and private partners helps secure long-term project pipelines. Firms also prioritize durability and reliability to ensure performance in extreme extraterrestrial environments.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2022 - 2035

2.2 Key market trends

2.2.1 Mission type trends

2.2.2 Vehicle type trends

2.2.3 Propulsion type trends

2.2.4 Application trends

2.2.5 End use trends

2.2.6 Regional

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Surging global interest in lunar and martian exploration missions

3.2.1.2 Technological advancements in autonomous navigation and mobility systems

3.2.1.3 Private sector investment and expansion in space exploration technologies

3.2.1.4 Governmental commitments to long-term lunar and mars colonization plans

3.2.1.5 Development of In-Situ resource utilization (isru) capabilities for space exploration

3.2.2 Industry pitfalls and challenges

3.2.2.1 High development costs and technological complexity

3.2.2.2 Risks of mission failures due to harsh extraterrestrial environments

3.2.3 Market opportunities

3.2.3.1 Development of sustainable space habitats

3.2.3.2 Advancements in autonomous technology for exploration

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Technology and innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Emerging business models

3.9 Compliance requirements

3.10 Defense Budget Analysis

3.11 Global Defense Spending Trends

3.12 Regional Defense Budget Allocation

3.12.1 North America

3.12.2 Europe

3.12.3 Asia Pacific

3.12.4 Middle East and Africa

3.12.5 Latin America

3.13 Key Defense Modernization Programs

3.14 Budget Forecast (2026-2035)

3.14.1 Impact on Industry Growth

3.14.2 Defense Budgets by Country

3.14.3 Defense Budget Allocation by Segment

3.14.3.1 Personnel

3.14.3.2 Operations and Maintenance

3.14.3.3 Procurement

3.14.3.4 Research, Development, Test and Evaluation

3.14.3.5 Infrastructure and Construction

3.14.3.6 Technology and Innovation

3.15 Supply Chain Resilience

3.16 Geopolitical Analysis

3.17 Workforce Analysis

3.18 Digital Transformation

3.19 Mergers, Acquisitions, and Strategic Partnerships Landscape

3.20 Risk Assessment and Management

3.21 Major Contract Awards (2022-2025)

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East & Africa

4.2.2 Market Concentration Analysis

4.3 Competitive benchmarking of key players

4.3.1 Financial performance comparison

4.3.1.1 Revenue

4.3.1.2 Profit margin

4.3.1.3 R&D

4.3.2 Product portfolio comparison

4.3.2.1 Product range breadth

4.3.2.2 Technology

4.3.2.3 Innovation

4.3.3 Geographic presence comparison

4.3.3.1 Global footprint analysis

4.3.3.2 Service network coverage

4.3.3.3 Market penetration by region

4.3.4 Competitive positioning matrix

4.3.4.1 Leaders

4.3.4.2 Challengers

4.3.4.3 Followers

4.3.4.4 Niche players

4.3.5 Strategic outlook matrix

4.4 Key developments

4.4.1 Mergers and acquisitions

4.4.2 Partnerships and collaborations

4.4.3 Technological advancements

4.4.4 Expansion and investment strategies

4.4.5 Sustainability initiatives

4.4.6 Digital transformation initiatives

4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Mission Type, 2022 - 2035 (USD Million)

5.1 Key trends

5.2 Lunar surface exploration

5.3 Mars surface exploration

5.4 Asteroids and comet exploration

Chapter 6 Market Estimates and Forecast, By Vehicle Type, 2022 - 2035 (USD Million)

6.1 Key trends

6.2 Space landers

6.3 Space rovers

Chapter 7 Market Estimates and Forecast, By Propulsion Type, 2022 - 2035 (USD Million)

7.1 Key trends

7.2 Chemical propulsion

7.3 Electric/Ion propulsion

7.4 Hybrid propulsion systems

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

8.1 Key trends

8.2 Chemical propulsion

8.3 Electric/Ion propulsion

8.4 Hybrid propulsion systems

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 (USD Million)

9.1 Key trends

9.2 Government and defense

9.3 Space exploration organizations

9.4 Private aerospace companies

9.5 Research institutions

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

10.1 Key trends

10.2 North America

10.2.1 U.S.

10.2.2 Canada

10.3 Europe

10.3.1 Germany

10.3.2 UK

10.3.3 France

10.3.4 Spain

10.3.5 Italy

10.3.6 Netherlands

10.4 Asia Pacific

10.4.1 China

10.4.2 India

10.4.3 Japan

10.4.4 Australia

10.4.5 South Korea

10.5 Latin America

10.5.1 Brazil

10.5.2 Mexico

10.5.3 Argentina

10.6 Middle East and Africa

10.6.1 South Africa

10.6.2 Saudi Arabia

10.6.3 UAE

Chapter 11 Company Profiles

11.1 Global Key Players

11.1.1 Lockheed Martin Corporation

11.1.2 Northrop Grumman Corporation

11.1.3 NASA

11.1.4 Roscosmos

11.1.5 Airbus SE

11.2 Regional key players

11.2.1 North America

11.2.1.1 Blue Origin

11.2.1.2 Canadian Space Agency

11.2.2 Asia Pacific

11.2.2.1 ISRO

11.2.2.2 Japan Aerospace Exploration Agency (JAXA)