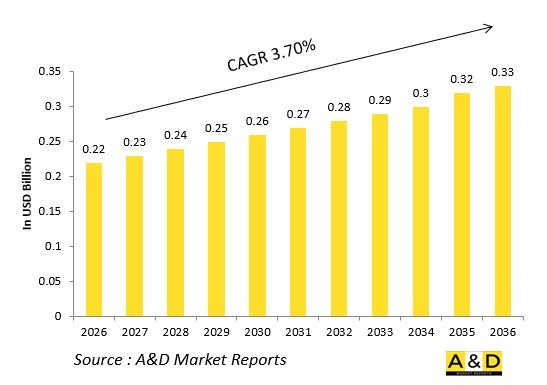

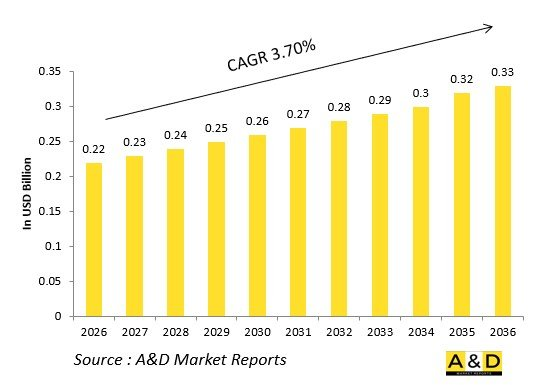

세계의 방위용 기상 센서 시장 규모는 2026년 2억 2,000만 달러에서 2026-2036년의 예측 기간 중 CAGR 3.70%로 성장하며, 2036년에는 3억 3,000만 달러에 달할 것으로 전망되고 있습니다.

세계 국방용 기상센서 시장은 항공, 육상, 해상, 우주 영역에서 정밀한 작전 수행을 위해 군에 실시간 기상정보를 제공합니다. 이 소형 장비는 풍속, 기압, 기온, 습도, 시야를 측정하고 그 데이터를 화기 관제, 항로 설정, 물류 계획 등에 활용합니다. 기후 변화가 작전을 방해하는 가운데 드론, 부표, 최전방 기지 등 가혹한 환경에 견딜 수 있는 견고한 센서에 대한 수요가 급증하고 있습니다. 드론에 통합할 수 있는 저 SWaP 설계의 멀티-파라미터 프로브가 혁신을 가져오고 있습니다. 해군용이 주류를 이루며 함정 조종과 미사일 탄도 계산을 지원하는 반면, 지상군은 포격 수정에 의존하고 있습니다. 공중 투하형 드롭존데와 풍선존데는 적의 지배지역으로 관측 범위를 확대합니다. 본 시장은 멀티 도메인 전략과 연동하여 기상 데이터를 AI와 융합하여 예측적 전장 인식을 실현합니다. 전반적으로 이러한 센서는 의사결정의 정확성을 높이고 현대전에서의 자연적 예측불가능성을 감소시킵니다.

국방용 기상 센서: 기술적 영향

기술 혁신은 국방용 기상 센서의 변화를 가져왔고, 역동적인 전장에서 초국지적 정확도를 실현하고 있습니다. 소형화된 MEMS 관성 유닛은 드론 탑재시 정확도 향상을 위해 운동 보정 및 풍속 측정을 통합하고 있습니다. 레이저식 LIDAR는 난류와 에어로졸을 감지하여 조종사에게 경고 기능을 강화합니다. 하이퍼스펙트럼 이미저는 구름의 미세물리학적 특성을 식별하고 표적 예측을 가능하게 합니다. 엣지 AI는 기내에서 원시 데이터를 처리하여 전술 네트워크의 지연을 크게 줄입니다. 고체형 습도계는 먼지 환경에서도 오염을 견딜 수 있습니다. 위성 연계형 컨스텔레이션은 메시 중계로 지속적인 모니터링을 실현합니다. 자체 보정 알고리즘은 소금이나 먼지로 인한 오염에 적응합니다. 레이더와 융합하여 종합적인 기상 상황을 파악할 수 있습니다. 이러한 비약적인 발전으로 소형화, 저소비전력화를 달성하여 공중부양형 무기나 성층권 풍선에 군집 전개가 가능해졌습니다. 센서는 수동적인 감시 장치에서 기상 내성 작전을 능동적으로 지원하는 기반으로 변모했습니다.

국방용 기상 센서 시장의 주요 촉진요인

국방용 기상 센서 시장을 촉진하는 주요 촉진요인은 다음과 같습니다. 정밀유도무기는 탄도 드리프트를 보정하기 위해 마이크로스케일의 풍향-풍속 데이터를 필요로 합니다. 원정대는 가혹한 환경에서의 신속한 전개로 인해 휴대용 키트를 필요로 합니다. 기후 변화의 진행은 강습상륙작전에서 폭풍 예측 능력의 중요성을 높이고 있습니다. 무인 시스템의 급증은 자율 항해를 위한 통합형 기상 센서 탑재를 필수적으로 요구하고 있습니다. 통합 전 영역 지휘는 기상 정보를 킬체인에 통합합니다. 전자전에 의한 간섭은 내결함성과 저 시그니처 설계를 촉진합니다. 물류 라인은 공수 작전을 위한 시각화 센서에 의존하고 있습니다. 군종 간 상호운용성 확보를 위해 데이터 포맷 표준 통일도 추진하고 있습니다. 반도체 부족에 대응하기 위해 공급망 강화가 이루어지고 있습니다. 예산 측면에서는 비용 효율성을 중시하고 민군겸용 COTS 제품이 우선시되는 경향이 있습니다. 이러한 요인들이 복합적으로 작용하여, 특히 물류가 경쟁하는 상황에서 센서는 의사결정 우위의 중요한 거점으로 자리매김하고 있습니다.

방산용 기상 센서의 지역별 동향

지역별로 운영 환경이 국방용 기상 센서의 사양과 도입 전략을 규정하고 있습니다. 북미는 태평양에서 항공모함 타격군 작전 및 북극권 순찰을 위해 드롭존데를 주도적으로 채택하고 있습니다. 유럽은 NATO 훈련에서 북대서양 항로 기상 예측을 위해 부이 네트워크와의 통합이 진행되고 있습니다. 아시아태평양은 몬순 시즌 작전을 위해 태풍 내성 센서를 중요시하고 있습니다. 인도 태평양 제도에서는 산호초 상륙 작전을 상정하고 태양광발전식 관측소를 도입하고 있습니다. 중동에서는 사막 항공 작전을 위한 먼지 폭풍 감지기가 주류를 이루고 있습니다. 아프리카에서는 사헬 지역의 먼지 회오리바람에 대응하기 위해 저비용 레이더를 채택하고 있습니다. 남미에서는 안데스 산맥 지역의 항공 작전에 대응하는 고고도 관측 센서가 우선시되고 있습니다. 국제 동맹은 데이터 피드를 공유하고, 미국의 기술과 지역 생산을 결합하는 형태로 협력을 진행하고 있습니다. 국제연합에서는 미국 기술과 지역 제조를 융합한 데이터 공유가 진행되고 있습니다. 드론 군집의 소형화, 초국지적 실시간 예측을 위한 AI 활용 등의 동향은 해양 우위 및 원정 작전의 요구를 반영하고 있습니다.

세계의 국방용 기상 센서(Defense Weather Sensor) 시장을 조사했으며, 주요 동향, 시장 영향요인, 주요 기술 및 그 영향, 주요 지역 및 국가별 동향, 시장 기회 분석 등의 정보를 정리하여 전해드립니다.

The Global defense meteorological sensors market is estimated at USD 0.22 billion in 2026, projected to grow to USD 0.33 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 3.70% over the forecast period 2026-2036.

The Global defense meteorological sensors market equips forces with real-time weather intelligence for precise operations across air, land, sea, and space domains. These compact devices measure wind, pressure, temperature, humidity, and visibility, feeding data into fire control, aviation routing, and logistics planning. As climate variability disrupts campaigns, demand surges for rugged sensors enduring extreme conditions on drones, buoys, and forward bases. Innovations integrate multi-parameter probes with low-SWaP designs for unmanned integration. Naval applications dominate, aiding ship handling and missile trajectories, while ground units rely on them for artillery corrections. Airborne dropsondes and balloon sondes extend reach into denied areas. The market aligns with multi-domain ops, fusing weather data with AI for predictive battlespace awareness. Overall, these sensors sharpen decision edges, mitigating nature's unpredictability in modern warfare.

Technology Impact in Defense Meteorological Sensors

Technological advances revolutionize defense meteorological sensors, delivering hyper-local accuracy in dynamic theaters. Miniaturized MEMS inertial units combine motion correction with anemometry for drone-mounted precision. Laser-based LIDAR detects turbulence and aerosols, enhancing pilot warnings. Hyperspectral imagers discern cloud microphysics for targeting forecasts. Edge AI processes raw data onboard, slashing latency for tactical nets. Solid-state hygrometers resist contamination in dusty ops. Satellite-linked constellations enable persistent monitoring via mesh relays. Self-calibrating algorithms adapt to fouling from salt or sand. Fusion with radar paints comprehensive weather pictures. These leaps cut size and power draws, enabling swarm deployments on loitering munitions and stratospheric balloons, transforming sensors from passive monitors to active enablers of weather-resilient maneuvers.

Key Drivers in Defense Meteorological Sensors

Pivotal drivers propel the defense meteorological sensors market. Precision-guided munitions demand microscale wind data to counter drift. Expeditionary forces require portable kits for rapid deployment in austere sites. Climate shifts amplify storm forecasting needs for amphibious assaults. Unmanned systems proliferation mandates integrated sensors for autonomous navigation. Joint all-domain command fuses weather into kill chains. Electronic warfare clutter spurs resilient, low-signature designs. Logistics chains depend on visibility sensors for airlift ops. Interoperability standards unify data formats across services. Supply resilience counters chip shortages. Budgets favor dual-use COTS for cost efficiency. Together, these forces elevate sensors as critical nodes in decision superiority, especially amid contested logistics.

Regional Trends in Defense Meteorological Sensors

Regional dynamics tailor defense meteorological sensors to local challenges. North America leads with dropsondes for Pacific carrier strikes and Arctic patrols. Europe integrates buoy networks for North Atlantic weather routing in NATO exercises. Asia-Pacific emphasizes typhoon-hardened sensors for monsoon-season ops. Indo-Pacific islands deploy solar-powered stations for reef assaults. Middle East trends focus on dust storm detectors for desert air ops. Africa adapts low-cost radars for Sahel dust devils. South America prioritizes high-altitude sensors for Andean aviation. Global alliances share data feeds, merging U.S. tech with regional manufacturing. Trends highlight miniaturization for drone swarms and AI for hyperlocal nowcasting, reflecting maritime primacy and expeditionary demands.

Key Defense Meteorological Sensors Program

Prominent programs showcase defense meteorological sensors in operational contexts. Naval fleets equip buoys with multi-sensor arrays for ocean basin coverage. Air force tankers integrate fuselage probes for mid-air refueling safety. Artillery brigades field vehicle-mounted kits linking to counter-battery radars. Special ops drops portable stations via parachute for denied access intel. Allied ventures develop standardized sondes for shared battlespaces. Unmanned programs embed sensors in loyal wingmen for formation flying. Milestones include live-fire validations and hurricane simulations. Carrier air wings test LIDAR for deck landing cues. These initiatives pioneer networked constellations, delivering fused data to command nodes and ensuring weather never grounds the fight.

By Region

By Platform

By Parameter Measured

By Installation

The 10-year Defense Meteorological Sensors Market analysis would give a detailed overview of Defense Meteorological Sensors Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Meteorological Sensors Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

The 10-year Defense Meteorological Sensors Market forecast of this market is covered in detailed across the segments which are mentioned above.

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Meteorological Sensors Market Report

Hear from our experts their opinion of the possible analysis for this market.

About Aviation and Defense Market Reports