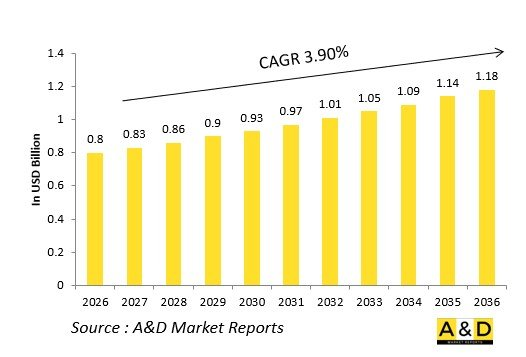

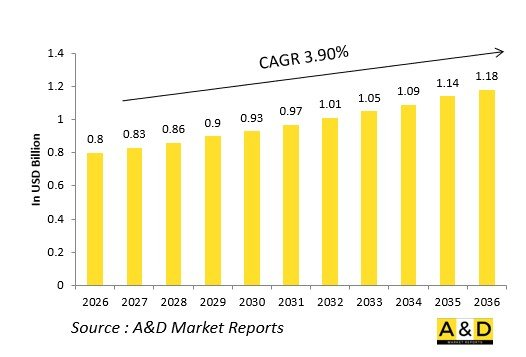

세계 방위용 애프터버너/재연소 시스템 시장 규모는 2026년에 8억 달러로 추정되며, 2036년에는 11억 8,000만 달러에 달할 것으로 예상되며, 2026-2036년 예측 기간 동안 3.90%의 CAGR로 성장할 것으로 예상됩니다.

소개

세계 방위용 애프터버너/재연소 시스템 시장은 터빈 후 연소를 제어하여 전술 항공기에 동력을 공급하고, 가시권 밖 전투 및 단거리 이륙에 사용되는 건식 추력을 증가시키는 역할을 합니다. 환형 보온기는 초음속 흐름에서 등유 분무를 안정화시키고, 냉각 라이너는 터빈의 표면을 열충격으로부터 보호합니다.

지정학적 영공권 경쟁이 개발을 촉진하고, 적응형 사이클 코어 및 FADEC 제어와의 통합이 우선순위를 차지하고 있습니다. 모듈식 설계로 구형 플랫폼에 대한 개조가 가능합니다. 공급망은 고온 합금과 세라믹 코팅에 초점을 맞추고 있습니다. 경쟁사로는 Pratt & Whitney, Rolls-Royce, Safran이 저NOx 재열 기술을 선도하고 있습니다.

이 시장은 열역학적 폭발을 통해 전투 우위를 촉진합니다.

방위용 애프터버너/재연소 시스템 기술의 영향

저배출 연소기는 리치?틸린존을 통해 가시신호를 대폭 감소시키면서 주간 요격에 필수적인 추력증강을 극대화합니다. 냉각 페탈 노즐은 증발 공기로 페탈을 박막 냉각하여 고온 에지에 의한 스텔스 기체에 대한 영향을 제거하면서 추력 벡터링을 실현합니다.

가변 지오메트리 목구멍은 비행 영역 전체에 걸쳐 배압을 조정하여 상승 시 분사 정지 및 기동 전투 시 시동 불능을 방지합니다. 플라즈마 점화 시스템은 횡풍에도 순간적으로 점화되어 화공품 카트리지가 필요 없습니다. 파일럿에서 메인으로 단계적 연료 분사는 마하 영역 전체에 걸쳐 화염을 안정화시킵니다.

라이너의 내열 코팅은 지속적인 재연소에도 견딜 수 있어 점검 주기를 연장합니다. 통합 FADEC는 터빈 회전수와 분사를 연동하여 과열을 방지합니다. 중공 프레임 홀더는 무게를 줄이면서 안정성을 유지합니다. 강화 추력은 슈퍼크루즈 코어와 연동하여 드라이에서 습식으로의 원활한 전환을 실현합니다.

디지털 트윈 기술을 통해 흡기 왜곡에 대한 분사 패턴을 최적화합니다. 세라믹 매트릭스 라이너는 터빈 흡기 온도 상승을 가능하게 합니다. 이러한 혁신은 노 이스케이프 존을 확장하여 이동식 SAM에 대한 심층 공격을 가능하게 합니다.

방위용 애프터버너/재연소 시스템의 주요 촉진요인

6세대 제작권 확보를 위해서는 극초음속 위협에 대한 슈퍼크루즈를 요격하는 지속적인 애프터버닝이 필수적입니다. 항공모함 항공전력에서는 최대 부하 하에서 투석기 발진 및 착함 제동 시 신뢰성 높은 습식 추력이 요구됩니다.

유지관리의 경제성 때문에 고온부 점검을 최소화하는 내구성 높은 라이너가 요구됩니다. 수출시장에서는 중립공역 통과를 위한 무연운항이 요구됩니다. 스텔스 통합을 통해 기체 외판과 조화를 이루는 냉각 노즐 페탈이 추진되고 있습니다.

예산의 압박으로 인해 전체 엔진의 재설계보다 모듈식 재연소가 우선시됩니다. 공급망 내성 강화는 고융점 금속 부족에 대응할 수 있습니다. 상호운용성 표준은 연합군 전체에 공통된 연료 제어를 가능하게 합니다.

도심전에서는 오버슈팅을 피하기 위한 정밀한 추력 버스트가 요구됩니다. 이러한 요구사항으로 인해 애프터버너는 전략적인 차별화 요소가 되고 있습니다.

세계의 방위용 애프터버너/재연소 시스템 시장에 대해 조사 분석했으며, 시장에 영향을 미치는 기술, 향후 10년간의 예측, 지역별 동향 등의 정보를 전해드립니다.

The Global Defense Afterburner / Reheat Systems Market is estimated at USD 0.8 billion in 2026, projected to grow to USD 1.18 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 3.90% over the forecast period 2026-2036.

Introduction

The global Defense Afterburner / Reheat Systems market powers tactical aircraft through controlled post-turbine combustion, multiplying dry thrust for beyond-visual-range engagements and short takeoffs. Annular flame holders stabilize kerosene spray amid supersonic flows, while cooled liners protect turbine faces from thermal shock.

Geopolitical air superiority competitions drive development, prioritizing integration with adaptive cycle cores and FADEC controls. Modular designs enable retrofits across legacy platforms. Supply chains focus on high-temperature alloys and ceramic coatings. Competition features Pratt & Whitney, Rolls-Royce, and Safran pioneering low-NOx reheat.

This market fuels combat edge through thermodynamic bursts.

Technology Impact in Defense Afterburner / Reheat Systems

Low-emission combustors with rich-quench-lean zones slash visible signatures while maximizing augmentation, critical for day intercepts. Cooled petal nozzles vector thrust without hot edges betraying stealth platforms, using transpiration air to film-cool petals.

Variable geometry throats adjust backpressure across flight envelopes, preventing blowout during climb or unstart in maneuvering combat. Plasma ignition systems light instantly under crosswinds, eliminating pyrotechnic cartridges. Staged fuel injection-pilot then main-stabilizes flame across Mach regimes.

Thermal barrier coatings on liners withstand sustained reheat, extending intervals between overhauls. Integrated FADEC sequences injection with turbine speeds, preventing overtemperature. Hollow flameholders reduce weight while maintaining stability. Augmented thrust links with super cruise cores for seamless dry-to-wet transitions.

Digital twins optimize spray patterns against inlet distortion, while ceramic matrix liners enable higher turbine inlet temperatures. These innovations extend no-escape zones and enable deep strikes against mobile SAMs.

Key Drivers in Defense Afterburner / Reheat Systems

Sixth-generation air dominance mandates sustained afterburning for super cruise intercepts against hypersonic threats. Carrier aviation demands reliable wet thrust for catapult strokes and arrested recoveries under max loads.

Sustainment economics favor durable liners minimizing hot-section inspections. Export markets require smoke-free operation for neutral airspace transit. Stealth integration drives cooled nozzle petals blending with aircraft skins.

Budget pressures prioritize modular reheat over full engine redesigns. Supply chain resilience counters refractory metal shortages. Interoperability standards enable common fuel controls across coalitions.

Urban combat needs precise thrust bursts avoiding overshoot. These imperatives position afterburners as mission differentiators.

Regional Trends in Defense Aircraft Afterburner / Reheat Systems

North America pioneers adaptive reheat for NGAD, emphasizing variable geometry.

Europe upgrades Typhoon and Rafale nozzles for dispersed basing.

Asia-Pacific accelerates indigenous development-India's Kaveri wet variant, China's WS-15-tailored to carrier ops.

Middle East pursues smoke-free systems for day operations.

Russia advances high-temperature alloys for Su-57 sustainment.

South Korea integrates with KF-21 export packages.

Trends favor ceramic liners; Asia-Pacific gains production share.

Key Defense Afterburner / Reheat Systems Programs

F135 afterburner powers F-35 across STOVL, CTOL, CV variants with stealthy petals.

NGAD variable cycle reheat enables super cruise without wet thrust.

EJ200 upgrades deliver dry super cruise with optimized nozzles.

India's Kaveri wet testing validates hollow reheat integration on Tejas.

WS-15 equips J-20 with indigenous augmentation.

Rafale M88 reheat sustains carrier operations.

T-50 FADEC-driven injection sequences wet thrust.

By Platform

By Nozzle Type

By Actuation

The 10-year Defense Afterburner / Reheat Systems market analysis would give a detailed overview of Defense Afterburner / Reheat Systems market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

The 10-year Defense Afterburner / Reheat Systems market forecast of this market is covered in detailed across the segments which are mentioned above.

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Hear from our experts their opinion of the possible analysis for this market.