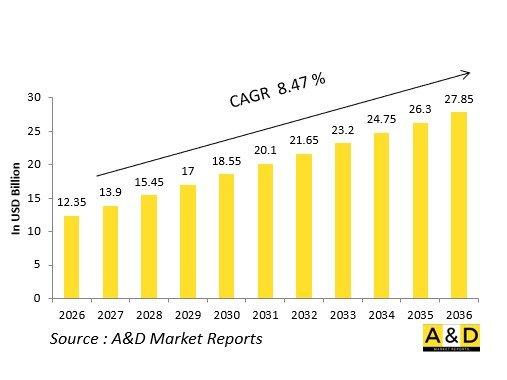

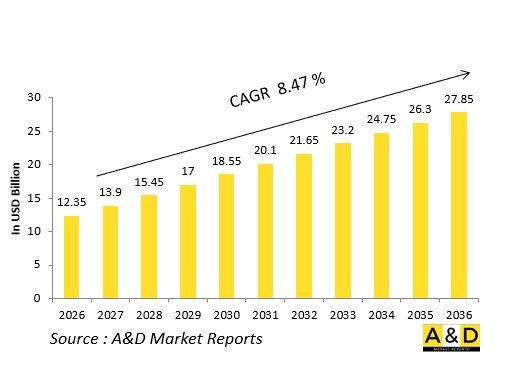

세계 AESA 레이더 시장 규모는 2026년에 123억 5,000만 달러로 추정되며, 2026년부터 2036년까지 예측 기간 동안 8.47%의 CAGR로 성장하여 2036년에는 278억 5,000만 달러에 달할 것으로 예상됩니다.

소개

세계 AESA 레이더 시장은 현대 항공 우위의 기반이 되는 고체 위상배열을 통해 전투기 사격통제, 해군 감시, 지상 미사일 방어를 지원하고 있습니다. 수천 개의 송수신 모듈(TRM)을 통해 신속한 빔 가변성, 동시 공대공 추적, 지상 매핑을 실현하여 신뢰성과 범용성에서 기계식 레이더를 능가합니다.

지정학적 긴장이 조달을 촉진하고 있으며, 각국 공군은 다목적 전투기 및 무인항공기를 위한 확장 가능한 아키텍처를 요구하고 있습니다. 상호운용성 표준은 수출을 촉진하고, 개방형 시스템 설계는 업그레이드를 용이하게 합니다. 반도체 부족 속에서 공급망은 내결함성이 높은 반도체에 초점을 맞추고 있습니다. GaN 기반 모듈 분야에서는 기존 대기업과 신생업체들이 경쟁하고 있습니다.

이 시장은 네트워크화된 전쟁에서 센서 융합의 역할을 구현하고 있습니다.

AESA 레이더의 기술적 영향

AESA 기술은 전자빔 조향을 통해 레이더 성능을 혁신적으로 개선하고, 기계식 짐벌을 제거하여 즉각적인 방위각 및 고도 변화를 실현합니다. GaN 기반 TRM은 출력과 효율을 향상시키고, 어레이를 소형화하면서 스텔스 목표물 및 극초음속 항공기에 대한 탐지 거리를 늘릴 수 있습니다.

다기능 능력으로 수십 개의 표적을 동시에 추적할 수 있으며, 소음 환경에서도 추적 및 스캔 동시 방식으로 미사일 유도가 가능합니다. 적응형 파형은 방해 전파를 피하고 적의 반응 속도를 능가하는 주파수 호핑을 실현합니다. 저포획확률 모드에서는 스펙트럼 확산 신호를 사용하여 수동형 검출기의 전파 방출을 은폐합니다.

디지털 빔 포밍은 정밀 검출을 위한 얇은 연필 빔과 탐색을 위한 넓은 팬 빔을 형성하여 지상 모드에서 합성 개구부 해상도를 최적화합니다. 비협조 목표물 인식은 마이크로 도플러 특성을 분석하여 아군/적군 식별을 수행합니다. 전자전 시스템과의 통합을 통해 지향성 노이즈로 위협을 억제합니다.

인지 알고리즘은 잡음과 속임수에 대해 스스로 최적화하고, 디지털 트윈 기술은 모드 개발을 가속화합니다. 함정 탑재형은 선체 동요에 견딜 수 있는 견고성을 갖추고, 넓은 범위의 탐색과 수평선 확장을 지원합니다. 이러한 발전은 킬 체인을 단축시켜 분쟁 영공에서 '선제공격 우위'를 실현할 수 있습니다.

AESA 레이더의 주요 촉진요인

전투기 부대의 현대화가 AESA 도입을 추진하고 있으며, 스텔스 위협과 포화 공격에 대응하기 위해 구형 기체의 개조가 진행되고 있습니다. 해군 항공전력은 원양에서의 경쟁 환경에서 다목적 항공모함을 위한 소형 기수 레이더를 필요로 합니다.

증식하는 극초음속-저가시성 무기는 기계 스캐닝의 한계를 넘어선 민첩한 추적을 필요로 합니다. 수출 시장에서는 다양한 플랫폼에 적응할 수 있는 확장 가능한 TRM 수와 오프셋 생산을 결합한 솔루션이 호황을 누리고 있습니다.

상호운용성 요구사항은 연합 작전을 위한 공통 아키텍처를 추진하고 있습니다. 질화갈륨(GaN)으로의 전환으로 크기, 무게, 전력이 크게 감소하여 드론과 충실한 윙맨의 무리를 실현할 수 있게 되었습니다. 전자전의 격화는 ECCM 내성 설계에 유리하게 작용하고 있습니다.

예산 압박으로 인해 유지보수 부담이 큰 진공관보다 수명이 긴 고체 소자를 채택하는 경향이 있습니다. 도시 공방전 교리에서는 멀티 모드 대응의 유연성이 우선시됩니다. 공급망 현지화는 취약성 대책이 될 수 있습니다.

효율적인 모듈을 통한 지속가능성은 녹색 조달과 일치합니다. 이러한 요소들이 AESA를 C4ISR의 기반이 될 수 있도록 합니다.

AESA 레이더의 지역별 동향

북미는 F-35 파생 기종과 이지스함 업그레이드를 위한 성숙한 GaN 프로그램을 주도하고 있으며, 멀티 도메인 융합을 중시하고 있습니다.

유럽에서는 유로파이터 및 라팔을 위한 확장성 어레이의 공동 개발이 진행되고 있으며, NATO 표준에 따라 동부 전선에서 조화를 이루기 위해 노력하고 있습니다.

아시아태평양에서는 도서 및 히말라야 지역의 위협에 대응하기 위해 인도의 테자스용 '우탐', 중국의 J-20용 장비 등 독자 개발이 가속화되고 있습니다.

중동 지역에서는 항공 우위 확보를 위해 서방 국가로부터의 수입품과 현지 조립을 통합하고 있습니다.

러시아는 전자전 포화에 강한 갈륨비소 어레이를 개발하고 있습니다.

한국과 일본은 해상거부작전을 위해 소형 함정 탑재형 AESA 레이더를 우선적으로 도입하고 있습니다.

라틴아메리카 지역에서는 영토 감시를 위해 지상 배치형 수입 장비에 집중하고 있습니다.

디지털 AESA와 AI 처리 동향 수렴, 아시아태평양은 대량 생산으로 우위 확보.

주요 AESA 레이더 계획

전투기 프로그램이 AESA 진화의 기반 - AN/APG-81은 스텔스기 플랫폼에 A2A/A2G 모드의 상호운용성과 전파방해 저항성을 갖추고 있습니다.

라팔 RBE2-AA는 수출용 함대를 위한 컴팩트한 GaN 전력을 제공합니다.

유로파이터 Captor-E는 역할의 유연성을 위해 TRM을 확장합니다.

인도 Uttam의 국산 어레이는 멀티 모드의 기동성으로 LCA의 후계기를 뒷받침합니다.

해군용 AN/SPY-6는 구축함의 광역 수색에 대응하는 확장성을 갖췄습니다.

지상 배치형 AN/TPY-4 이동식 어레이는 미사일 방어를 유도합니다.

MQ-9 프레데터와 같은 무인항공기(UAV)의 개량형은 장거리 정찰 및 감시(ISR) 능력을 확장합니다.

디지털 AESA의 로드맵은 인지 모드를 위해 양자 프로세서를 융합합니다.

공동 개발 시제품을 통한 극초음속 추적 테스트 실시.

수출 패키지는 미사일과 일체화되어 종합적인 살상 능력을 실현합니다.

이러한 노력으로 레이더는 역동적인 효과 장치로 재정의되고 있습니다.

The Global AESA Radar Market is estimated at USD 12.35 billion in 2026, projected to grow to USD 27.85 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 8.47% over the forecast period 2026-2036.

Introduction

The global AESA Radar market anchors modern air dominance, powering fighter fire control, naval surveillance, and ground-based missile defense with solid-state phased arrays. Thousands of transmit-receive modules (TRMs) enable rapid beam agility, simultaneous air-to-air tracking, and ground mapping, surpassing mechanical radars in reliability and versatility.

Geopolitical tensions drive procurement, with air forces seeking scalable architectures for multirole fighters and UAVs. Interoperability standards facilitate exports, while open-system designs ease upgrades. Supply chains focus on resilient semiconductors amid chip constraints. Competition pits established primes against emerging players in GaN-based modules.

This market exemplifies sensor fusion's role in networked warfare.

Technology Impact in AESA Radar

AESA technology revolutionizes radar performance through electronic beam steering, eliminating mechanical gimbals for instantaneous azimuth and elevation shifts. GaN-based TRMs boost power output and efficiency, shrinking arrays while extending detection against stealthy targets and hypersonics.

Multi-function capabilities track dozens of contacts simultaneously, cueing missiles via track-while-scan amid clutter. Adaptive waveforms evade jamming, hopping frequencies faster than adversaries react. Low-probability-of-intercept modes use spread-spectrum signals, concealing emissions from passive detectors.

Digital beamforming shapes narrow pencil beams for precision or wide fans for search, optimizing synthetic aperture resolution in ground modes. Non-cooperative target recognition analyzes micro-Doppler signatures for friend-foe decisions. Integration with EW suites suppresses threats via directed noise.

Cognitive algorithms self-optimize against clutter or deception, while digital twins accelerate mode development. Naval variants ruggedize for ship motion, supporting volume search and horizon extension. These strides compress kill chains, enabling first-look-first-kill advantages in contested airspace.

Key Drivers in AESA Radar

Fighter fleet modernization propels AESA adoption, retrofitting legacy airframes to counter stealthy threats and saturation attacks. Naval aviation demands compact nose radars for multirole carriers amid blue-water rivalries.

Proliferating hypersonic and low-observable munitions necessitate agile tracking beyond mechanically scanned limits. Export markets thrive on scalable TRM counts suiting diverse platforms, bundled with offset production.

Interoperability mandates drive common architectures for coalition ops. GaN transitions slash size-weight-power, enabling UAV and loyal wingman swarms. Electronic warfare escalation favors ECCM-hardened designs.

Budget pressures favor long-life solid-state over maintenance-heavy tubes. Urban air combat doctrines prioritize multi-mode flexibility. Supply chain localization counters vulnerabilities.

Sustainability via efficient modules aligns with green procurement. These forces embed AESA as C4ISR cornerstone.

Regional Trends in AESA Radar

North America leads with mature GaN programs for F-35 derivatives and Aegis upgrades, emphasizing multi-domain fusion.

Europe collaborates on scalable arrays for Eurofighter and Rafale, harmonizing via NATO standards for eastern flanks.

Asia-Pacific accelerates indigenous development-India's Uttam for Tejas, China's J-20 suites-tailored to island and Himalayan threats.

Middle East integrates Western imports with local assembly for air superiority.

Russia advances gallium arsenide arrays resilient to EW saturation.

South Korea and Japan prioritize compact naval AESA for sea denial.

Latin America focuses ground-based imports for territorial vigilance.

Trends converge on digital AESA with AI processing, Asia-Pacific gaining via volume production.

Key AESA Radar Programs

Fighter programs anchor AESA evolution: AN/APG-81 equips stealth platforms with interleaved A2A/A2G modes and jamming resistance.

Rafale RBE2-AA delivers compact GaN power for export fleets.

Eurofighter Captor-E scales TRMs for role flexibility.

India's Uttam indigenous array powers LCA successors with multimode agility.

Naval AN/SPY-6 scales for destroyer volume search.

Ground-based AN/TPY-4 mobile arrays cue missile defenses.

UAV variants like MQ-9 Predator upgrades extend endurance ISR.

Digital AESA roadmaps fuse quantum processors for cognitive modes.

Collaborative prototypes test hypersonic tracking.

Export packages bundle with missiles for holistic lethality.

These initiatives redefine radar as dynamic effectors.

By Region

By Fit

By Platform

The 10-year AESA radar market analysis would give a detailed overview of AESA radar market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

The 10-year AESA radar market forecast of this market is covered in detailed across the segments which are mentioned above.

The regional AESA radar market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Hear from our experts their opinion of the possible analysis for this market.