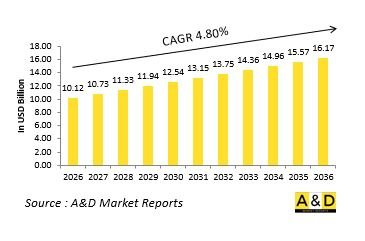

세계의 대함 미사일 시장 규모는 2026년에 101억 2,000만 달러로 추정되며, 2026년에서 2036년까지 예측 기간에 CAGR 4.80%로 성장하여 2036년까지 161억 7,000만 달러에 달할 것으로 전망됩니다.

소개

대함 미사일은 해상 전투 능력의 핵심 요소이며, 전략 해로와 해안 지역에서 적의 이동의 자유를 방해하도록 설계되었습니다. 이러한 시스템을 통해 해군 부대는 가시거리를 넘어 전력을 투사하여 수상 함대에 대한 강력한 억제력을 발휘할 수 있습니다. 해상 경쟁이 심화되고 해군 작전이 분쟁 중인 연안 지역까지 확대되면서 그 중요성이 더욱 커지고 있습니다. 대함 미사일은 수상함정, 잠수함, 항공기, 해안포대, 이동식 육상 발사대 등 다양한 플랫폼에 배치되어 있습니다. 이러한 유연성을 통해 방위군은 다층적인 해상 방어 체제를 구축하여 적의 작전 계획을 복잡하게 만들 수 있습니다. 현대 해군 전술 교리는 해상 거부 및 접근 통제를 중시하고 대함 미사일은 비대칭 우위를 실현하는 중요한 수단으로 자리매김하고 있습니다. 그 역할은 고강도 분쟁을 넘어 억지 순찰과 전략적 시그널링에 이르기까지 다양합니다. 해군 플랫폼의 네트워크화 및 센서 중심화가 진행됨에 따라 대함 미사일은 광범위한 해상 감시 및 표적 포착 시스템에 통합되고 있습니다. 그 지속적인 진화는 정밀한 교전 능력과 해양 영역 지배에 대한 강조의 증가를 반영합니다.

대함 미사일의 기술적 영향

기술 발전은 대함 미사일 시스템의 효율성과 생존성을 재정의하고 있습니다. 시커 기술의 향상으로 혼잡한 해상 환경에서 목표물 식별 능력이 강화되었습니다. 고급 유도 알고리즘을 통해 미사일은 비행 프로파일을 조정하고 방어 시스템을 회피할 수 있습니다. 추진 시스템의 개선은 기동성을 유지하면서 작전 사거리를 연장합니다. 저가시성 설계 기술은 말기 단계에서의 탐지 가능성을 낮춥니다. 네트워크 지원 목표 포착은 실시간 센서 입력에 기반한 중간 궤도 수정을 가능하게 합니다. 개선된 전자적 대응책은 방해와 속임수에 대한 저항력을 높입니다. 탄두 설계의 혁신은 현대 함정 방어에 대한 충격 효과를 최적화합니다. 멀티 도메인 센서 네트워크와의 통합은 목표물 포착 정확도를 향상시킵니다. 이러한 기술적 발전으로 대함 미사일은 방어가 강화되는 해상 환경에서도 확고한 위협으로 남을 수 있습니다.

대함 미사일의 주요 촉진요인

대함 미사일에 대한 수요는 변화하는 해양 안보 역학 및 진화하는 해군 전략에 의해 주도되고 있습니다. 영해 및 배타적 경제수역 보호의 필요성은 해안 방어 능력에 대한 투자를 지속하고 있습니다. 해군 현대화 계획은 분산형 살상 능력과 장거리 공격 옵션에 중점을 두고 있습니다. 해상교통로 보호와 군사력 투사에 대한 중점 강화는 수상 공격 시스템의 중요성을 더욱 높이고 있습니다. 예산 효율성 측면에서 대규모 함대 확장보다 미사일 기반 억지력이 우선시됩니다. 동맹국 해군과의 상호운용성도 시스템 개발에 영향을 미칩니다. 접근 거부 전략의 부상은 첨단 미사일 솔루션에 대한 수요를 더욱 촉진하고 있습니다. 이러한 요인들이 결합되어 대함 미사일 능력의 전략적 중요성을 유지하고 있습니다.

대함 미사일의 지역적 동향

지역별 해상 우선순위는 대함 미사일의 채택과 배치에 큰 영향을 미칩니다. 북미 해군은 항공모함 타격군과의 통합 및 다영역 해상 작전에 중점을 두고 있습니다. 유럽 해군은 해안 방어와 공동 해양 안보 이니셔티브를 중시하고 있습니다. 아시아태평양은 혼잡한 해역에서의 해상 거부 전략과 섬 방어 전략을 우선시합니다. 중동 국가들은 전략적 수로와 주요 인프라 보호에 주력하고 있습니다. 아프리카 연안 국가들은 해상 안보와 억지력을 강화하기 위해 미사일 능력 탐구에 박차를 가하고 있습니다. 지역을 불문하고 국내 개발 및 기술 제휴가 확대되고 있습니다. 이러한 추세는 현대 해군 전략에서 대함 미사일의 중심적인 역할을 강조하고 있습니다.

록히드마틴은 지난 7월 미 국방부와 AGM-158C 장거리 대함 미사일 및 합동 공대지 스탠드오프 미사일 대량 조달에 대한 95억 달러 규모의 계약을 체결했습니다. 이 계약에는 2033년까지 JASSM 22-26롯트, LRASM 9-12롯트 생산이 포함되어 있으며, LRASM의 급증하는 생산량을 위해 43억 달러의 추가 예산이 배정되어 있습니다. 이 스텔스 정밀 유도 미사일은 미국 및 동맹국 공군에 적의 방공권 밖에서 작전하면서 고가 해상 표적을 무력화할 수 있는 대치 능력을 제공합니다.

플랫폼별

지역별

유형별

이 장에서는 10년간의 대함 미사일 시장 분석을 통해 대함 미사일 시장의 성장, 변화하는 동향, 기술 채택 개요, 시장 매력에 대한 상세한 개요를 제공합니다.

이 부문에서는 이 시장에 영향을 미칠 것으로 예상되는 상위 10가지 기술과 이러한 기술이 전체 시장에 미칠 수 있는 영향에 대해 설명합니다.

이 시장의 10년간 대함 미사일 시장 예측은 위의 부문에 걸쳐 상세히 다루고 있습니다.

이 부문에서는 지역별 대함 미사일 시장 동향, 촉진요인, 저해요인, 과제, 정치, 경제, 사회, 기술 등 다양한 측면을 다루고 있습니다. 또한 지역별 시장 예측과 시나리오 분석도 상세히 다루고 있습니다. 지역 분석의 마지막 부분에서는 주요 기업 프로파일링, 공급업체 현황, 기업 벤치마킹에 대해 설명합니다.

북미

촉진요인, 억제요인, 도전과제

PEST

주요 기업

공급업체 계층 현황

기업 벤치마크

유럽

중동

아시아태평양

남미

이 장에서는 이 시장의 주요 방어 프로그램을 다루고, 이 시장에서 출원된 최신 뉴스와 특허에 대해 설명합니다. 또한, 국가별 10년 시장 전망과 시나리오 분석에 대해서도 설명합니다.

미국

국방 프로그램

최신 뉴스

특허

이 시장의 현재 기술 성숙도

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카공화국

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

기회 매트릭스는 독자들이 이 시장에서 기회가 높은 부문을 이해하는 데 도움이 됩니다.

이 시장의 향후 전망에 대해 당사 전문가들의 의견을 정리해 보았습니다.

The Global Anti-Ship Missiles market is estimated at USD 10.12 billion in 2026, projected to grow to USD 16.17 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.80% over the forecast period 2026-2036.

Introduction

Anti ship missiles are a central element of maritime combat capability, designed to deny adversaries freedom of movement across strategic sea lanes and coastal regions. These systems enable naval forces to project power beyond visual range and impose significant deterrence against surface fleets. Their importance has increased as maritime competition intensifies and naval operations extend into contested littoral zones. Anti ship missiles are deployed across a wide range of platforms, including surface vessels, submarines, aircraft, coastal batteries, and mobile land-based launchers. This flexibility allows defense forces to establish layered maritime defense architectures that complicate adversary planning. Modern naval doctrine emphasizes sea denial and access control, positioning anti ship missiles as key instruments of asymmetric advantage. Their role extends beyond high-intensity conflict to include deterrence patrols and strategic signaling. As naval platforms become more networked and sensor-driven, anti ship missiles are increasingly integrated into broader maritime surveillance and targeting ecosystems. Their continued evolution reflects the growing emphasis on precision engagement and control of maritime domains.

Technology Impact in Anti Ship Missiles

Technological advancements are redefining the effectiveness and survivability of anti ship missile systems. Improvements in seeker technology enhance target discrimination in cluttered maritime environments. Advanced guidance algorithms allow missiles to adapt flight profiles and evade defensive systems. Propulsion enhancements extend operational reach while maintaining maneuverability. Low-observable design techniques reduce detectability during terminal phases. Network-enabled targeting allows mid-course updates based on real-time sensor inputs. Improved electronic counter-countermeasures increase resistance to jamming and deception. Warhead design innovations optimize impact effectiveness against modern ship defenses. Integration with multi-domain sensor networks enhances targeting accuracy. These technological developments ensure anti ship missiles remain credible threats in increasingly defended maritime environments.

Key Drivers in Anti Ship Missiles

The demand for anti ship missiles is driven by shifting maritime security dynamics and evolving naval doctrines. The need to protect territorial waters and exclusive maritime zones sustains investment in coastal defense capabilities. Naval modernization programs emphasize distributed lethality and long-range strike options. Increased emphasis on sea lane protection and power projection reinforces the importance of surface strike systems. Budget efficiency considerations favor missile-based deterrence compared to large fleet expansion. Interoperability with allied naval forces also influences system development. The rise of anti-access strategies further drives demand for advanced missile solutions. These drivers collectively sustain the strategic relevance of anti ship missile capabilities.

Regional Trends in Anti Ship Missiles

Regional maritime priorities strongly influence anti ship missile adoption and deployment. North American naval forces focus on integration with carrier strike groups and multi-domain maritime operations. European navies emphasize coastal defense and joint maritime security initiatives. Asia-Pacific regions prioritize sea denial and island defense strategies in congested waters. Middle Eastern forces focus on protecting strategic waterways and critical infrastructure. African coastal states increasingly explore missile capabilities to enhance maritime security and deterrence. Across regions, domestic development and technology partnerships are expanding. These trends highlight the central role of anti ship missiles in modern naval strategy.

Lockheed Martin received a $9.5 billion Pentagon contract in July 2025 covering large-lot procurement of AGM-158C Long Range Anti-Ship Missiles and Joint Air-to-Surface Standoff Missiles. The award includes production lots 22-26 for JASSM and lots 9-12 for LRASM through 2033, with additional $4.3 billion allocated specifically for LRASM surge production. These stealthy, precision-guided missiles provide U.S. and allied air forces with stand-off capability to neutralize high-value maritime targets while operating outside enemy air defense envelopes.

By Platform

By Region

By Type

The 10-year anti ship missiles market analysis would give a detailed overview of anti ship missiles market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

The 10-year anti ship missiles market forecast of this market is covered in detailed across the segments which are mentioned above.

The regional anti ship missiles market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking.

North America

Drivers, Restraints and Challenges

PEST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Hear from our experts their opinion of the possible outlook for this market.