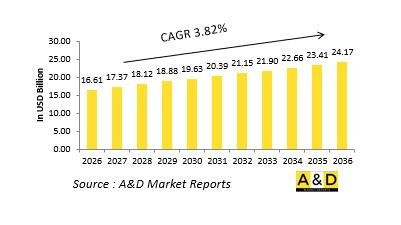

세계의 탄약 시장 규모는 2026년에 추정 166억 1,000만 달러이며, 2036년까지 241억 7,000만 달러에 달할 것으로 예측되며, 2026-2036년 예측 기간 동안 CAGR로 3.82%의 성장이 전망됩니다.

소개

탄약은 소형 화기, 포병, 장갑 시스템, 해군 무기, 공중 투하 플랫폼의 효율성을 뒷받침하는 군사 능력에서 가장 중요하고 지속적으로 소비되는 구성요소 중 하나입니다. 정기적으로 조달되는 주요 플랫폼과 달리 탄약은 일상적인 준비태세, 훈련 주기 및 전투 작전을 유지하기 위해 방어 부대에 항상 우선순위가 될 수 있습니다. 그 전략적 중요성은 실제 분쟁을 넘어 비축, 억지력, 장기적인 전력 정비에까지 이릅니다. 현대의 군대는 다양한 작전적 역할, 환경, 무기체계에 맞게 조정된 다양한 탄약을 필요로 합니다. 군사 전략이 지속적이고 빈번한 작전으로 진화함에 따라 탄약의 신뢰성, 가용성, 호환성은 작전 성공의 결정적인 요소로 작용합니다. 준비태세와 신속 대응에 대한 전 세계적인 관심으로 탄약 계획은 전략적 수준으로 격상되어 방위 산업 정책 및 공급망 관리에 영향을 미치고 있습니다. 외부 요인에 의한 혼란에 대한 취약성을 줄이기 위해 자국 생산과 안전한 조달원 확보가 점점 더 중요시되고 있습니다. 탄약은 군사력의 기초적인 요소로서 산업 능력과 전장에서의 효용성을 직접적으로 연결하는 역할을 하고 있습니다.

탄약에 대한 기술의 영향

기술 혁신은 여러 영역에 걸쳐 탄약의 설계, 성능, 안전성을 재구성하고 있습니다. 발사체의 화학 성분의 발전은 일관성, 안정성, 에너지 효율을 향상시키고 정확도를 높이며 포신의 마모를 감소시키고 있습니다. 정밀 제조 기술로 공차가 엄격해져 신뢰성이 향상되고 불발률이 감소하고 있습니다. 강화된 포탄 재료와 밀봉 방법은 특히 혹독한 기후 조건에서 보관 및 운송 시 내구성을 향상시킵니다. 유도탄과 스마트 탄약은 개선된 센서와 제어 메커니즘이 표적 포착 능력을 향상시키면서 부수적인 영향을 줄입니다. 친환경 기술도 개발에 영향을 미치고 있으며, 저독성 재료와 청정 연소 공정이 주목을 받고 있습니다. 탄약 생산의 자동화는 생산 과정에서 인적 리스크를 줄이면서 생산의 일관성과 확장성을 향상시킵니다. 디지털 품질 관리 시스템은 전체 생산 라이프사이클에 걸쳐 실시간 검사 및 추적성을 가능하게 합니다. 이러한 기술적 진보는 전장에서의 성능 향상뿐만 아니라 보다 안전한 취급, 장기 보관성, 효율적인 물류 지원도 가능하게 합니다.

탄약의 주요 촉진요인

탄약에 대한 수요는 작전 준비태세 요건, 훈련 강도, 진화하는 위협 환경의 조합에 의해 촉진되고 있습니다. 지속적인 군사 훈련과 부대 준비 프로그램은 평시에도 엄청난 양의 탄약을 소비합니다. 지정학적 긴장이 고조되면서 비축량을 유지하는 것이 더욱 중요해지고 있습니다. 무기 플랫폼의 현대화에는 호환 가능한 우수한 탄약이 필요합니다. 국방 정책은 공급망 보안을 점점 더 우선시하고 국내 생산과 장기 조달 계약을 촉진하고 있습니다. 도시와 비대칭 전쟁 환경에서는 정밀도와 효과 제어에 최적화된 특수 탄약에 대한 수요가 증가하고 있습니다. 또한, 국토안보와 국경 보안 활동의 확대로 인해 안정적인 소비가 지속되고 있습니다. 유통기한 연장 및 안전한 폐기를 포함한 수명주기 관리를 고려하는 것도 조달 전략에 영향을 미치고 있습니다. 이러한 요인들로 인해 전 세계 방산 기관에서 지속적이고 예측 가능한 탄약 수요가 발생하고 있습니다.

탄약의 지역별 동향

각 지역의 탄약 수요는 각 지역의 안보 태도와 산업 역량을 반영합니다. 북미에서는 훈련, 즉각적인 대응태세, 원정작전을 지원하기 위해 대규모 생산능력 유지에 중점을 두고 있습니다. 유럽의 수요는 연합군 간의 탄약 비축 계획과 탄약 표준화 활동에 의해 형성되고 있습니다. 아시아태평양에서는 군대의 확장, 해양 안보 문제, 훈련 강도의 증가로 인해 수요가 확대되고 있습니다. 중동의 수요는 작전 준비태세와 고위험 환경에서의 지속적인 안보 활동과 밀접한 관련이 있습니다. 아프리카의 수요는 평화 유지 활동, 국토안보 요구 사항, 단계적 현대화 활동의 영향을 받고 있습니다. 각 지역 정부는 외부 공급업체에 대한 의존도를 낮추기 위해 국내 제조 능력과 저장 인프라에 대한 투자를 진행하고 있습니다. 이러한 지역적 추세는 탄약 계획이 광범위한 방어 전략 및 위협 인식과 밀접하게 연계되어 있음을 보여줍니다.

세계의 탄약 시장에 대해 조사 분석했으며, 시장에 영향을 미치는 기술, 향후 10년간의 예측, 지역별 동향 등의 정보를 전해드립니다.

지역별

구경별

최종사용자별

북미

촉진요인, 억제요인, 도전과제

PEST

주요 기업

공급업체 티어 현황

기업 벤치마크

유럽

중동

아시아태평양

남미

미국

국방 프로그램

최신 뉴스

특허

이 시장의 현재 기술 성숙도

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카공화국

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

The Global Ammunition market is estimated at USD 16.61 billion in 2026, projected to grow to USD 24.17 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 3.82% over the forecast period 2026-2036.

Introduction

Ammunition remains one of the most essential and continuously consumed components of military capability, underpinning the effectiveness of small arms, artillery, armored systems, naval weapons, and air-delivered platforms. Unlike major platforms that are procured periodically, ammunition sustains day-to-day readiness, training cycles, and combat operations, making it a constant priority for defense forces. Its strategic importance extends beyond active conflict to include stockpiling, deterrence, and long-term force preparedness. Modern armed forces require a wide variety of ammunition types tailored to different operational roles, environments, and weapon systems. As military doctrines evolve toward sustained and high-tempo operations, the reliability, availability, and compatibility of ammunition become critical factors in operational success. The global focus on readiness and rapid response has elevated ammunition planning to a strategic level, influencing defense industrial policy and supply chain management. Indigenous production and secure sourcing are increasingly emphasized to reduce vulnerability to external disruptions. Ammunition continues to serve as a foundational element of military power, directly linking industrial capacity with battlefield effectiveness.

Technology Impact in Ammunition

Technological innovation is reshaping ammunition design, performance, and safety across multiple domains. Advances in propellant chemistry improve consistency, stability, and energy efficiency, enhancing accuracy and reducing barrel wear. Precision manufacturing techniques ensure tighter tolerances, leading to improved reliability and reduced misfire rates. Enhanced casing materials and sealing methods increase durability during storage and transport, particularly in extreme climates. In guided and smart ammunition categories, improved sensors and control mechanisms enhance targeting effectiveness while reducing collateral impact. Environmentally conscious technologies are also influencing development, with reduced-toxicity materials and cleaner combustion processes gaining attention. Automation in ammunition production improves output consistency and scalability while lowering human risk during manufacturing. Digital quality control systems enable real-time inspection and traceability throughout the production lifecycle. These technological advancements not only improve battlefield performance but also support safer handling, longer storage life, and more efficient logistics.

Key Drivers in Ammunition

The demand for ammunition is driven by a combination of operational readiness requirements, training intensity, and evolving threat environments. Ongoing military exercises and force preparedness programs consume significant volumes of ammunition even in peacetime. Heightened geopolitical tensions reinforce the importance of maintaining robust stockpiles. Modernization of weapon platforms necessitates compatible and upgraded ammunition types. Defense policies increasingly prioritize supply chain security, encouraging domestic production and long-term procurement agreements. Urban and asymmetric warfare environments drive demand for specialized ammunition optimized for precision and controlled effects. Additionally, the expansion of homeland security and border protection operations sustains consistent consumption. Lifecycle management considerations, including shelf-life extension and safe disposal, further influence procurement strategies. These drivers collectively create sustained and predictable demand for ammunition across global defense forces.

Regional Trends in Ammunition

Regional ammunition demand reflects distinct security postures and industrial capacities. In North America, emphasis is placed on maintaining large-scale production capability to support training, readiness, and expeditionary operations. European demand is shaped by coordinated stockpiling initiatives and efforts to standardize ammunition types among allied forces. Asia-Pacific regions experience growing demand driven by force expansion, maritime security concerns, and increased training intensity. Middle Eastern demand is closely tied to operational readiness and sustained security operations in high-risk environments. African demand is influenced by peacekeeping missions, internal security requirements, and gradual modernization efforts. Across regions, governments are investing in domestic manufacturing and storage infrastructure to reduce dependence on external suppliers. These regional dynamics demonstrate how ammunition planning is closely aligned with broader defense strategies and threat perceptions.

General Dynamics Ordnance and Tactical Systems received a $727.8 million U.S. Army contract in April 2025 for 120mm Insensitive Munition High Explosive with Tracer tank ammunition. The firm-fixed-price award covers production of next-generation tank rounds featuring enhanced safety characteristics that reduce accidental detonation risks during storage, transport, or combat damage. Additional contracts included $465 million for 120mm training ammunition, reflecting sustained demand for both live-fire and simulation rounds amid global armored warfare modernization efforts.

By Region

By Caliber

By End User

The 10-year ammunition market analysis would give a detailed overview of ammunition market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

The 10-year ammunition market forecast of this market is covered in detailed across the segments which are mentioned above.

The regional ammunition market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Hear from our experts their opinion of the possible analysis for this market.