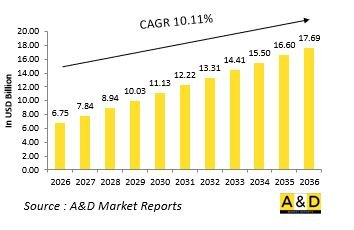

세계의 방위용 액추에이션 시스템 시장 규모는 2026년에 약 67억 5,000만 달러로 추정되고, 2036년까지 176억 9,000만 달러에 이를 것으로 예측되며, 2026-2036년의 예측 기간에 CAGR 10.11%의 성장이 전망되고 있습니다.

세계 방위용 액추에이션 시스템 소개

세계 방위용 액추에이션 시스템은 군용 플랫폼 전반에 걸쳐 전자 또는 수동 명령을 물리적 동작으로 변환하는 제어된 기계식 동작을 가능하게 합니다. 이러한 시스템은 방향 제어, 힘 가하기, 안정화, 주요 서브시스템의 위치 결정 등 동작이 매우 중요한 기능의 핵심에서 작동합니다. 그 신뢰성은 플랫폼의 안전성, 운영 정확도, 작전 연속성에 직접적인 영향을 미칩니다. 현대의 국방 환경에서 액추에이션 시스템은 가혹한 기계적 스트레스, 적대적인 운영 환경, 장기간의 배치 주기에서도 일관된 성능을 발휘해야 합니다. 센서, 제어 소프트웨어, 기계 어셈블리 간의 협력적 상호 작용을 지원하여 고속 또는 고부하 작동 시에도 예측 가능한 작동을 보장합니다. 국방 플랫폼이 통합 및 자동화 아키텍처로 진화함에 따라, 액추에이션 시스템은 개별 기계 요소가 아닌 정밀 제어를 실현하기 위한 기반으로서 설계되고 있습니다. 항공기의 기동, 함정의 조타, 육상 차량의 기동성, 무기의 조준 조정 등 그 역할은 매우 다양합니다. 국방 플랫폼의 복잡성이 증가함에 따라, 작동 시스템의 전략적 중요성이 증가하고 있으며, 현대 군의 대응성, 생존성 및 전체 플랫폼의 효율성에 기여하는 필수적인 요소로 자리 잡고 있습니다.

세계 방위용 액추에이션 시스템에서 기술이 미치는 영향

기술 개발은 방위용 액추에이션 시스템의 설계 및 배치 방법을 재정의했습니다. 최신 솔루션은 디지털 지휘 인터페이스를 중시하고, 연속적인 피드백 제어를 통해 동작을 정밀하게 실행할 수 있습니다. 센서 내장형 액추에이터는 실시간 성능 인식을 제공하여 시스템이 변화하는 동작 부하에 동적으로 적응할 수 있도록 합니다. 재료 공학의 발전은 구조적 부피를 줄이면서 높은 출력을 실현하는 컴팩트한 디자인을 지원합니다. 전동식 액추에이션 아키텍처는 효율성을 향상시키고 자동 제어 시스템과의 통합을 단순화합니다. 액추에이터에 내장된 진단 인텔리전스는 상태 기반 유지보수를 지원하여 가동률을 높이고 예기치 않은 다운타임을 줄입니다. 신호 무결성 및 내결함성 강화는 전자적으로 장애가 있는 환경에서 신뢰성을 높입니다. 이러한 기술적 변화로 인해 액추에이션 시스템은 지능형 운동 모듈로 작동하여 복잡한 방어 플랫폼 전체에서 연계성, 정확성 및 제어성을 향상시킵니다.

세계 방위용 액추에이션 시스템의 주요 추진 요인들

첨단 방위용 액추에이션 시스템에 대한 수요는 여러 가지 운영상의 전략적 요인에 의해 촉진되고 있습니다. 플랫폼 현대화 노력은 디지털화, 자동화 환경에 대응하는 운동 제어 솔루션을 요구하고 있습니다. 원격 조작 시스템 및 자율 시스템의 채택이 확대됨에 따라 인간의 직접적인 개입 없이 신뢰할 수 있는 기계적 동작에 대한 의존도가 높아지고 있습니다. 국방 조직은 또한 유지보수 부하 감소와 서비스 간격 연장을 통해 작전 수행 준비태세 향상을 추구하고 있습니다. 항공 및 육상 플랫폼의 무게 최적화 노력은 소형 고성능 액추에이터의 채택을 촉진하고 있습니다. 목표물 포착, 탐색 및 안정화에서 정밀도가 요구됨에 따라 첨단 액추에이션 솔루션의 필요성이 더욱 커지고 있습니다. 또한, 공급 보안에 대한 고려사항은 신뢰할 수 있고 현지 지원이 가능한 액추에이션 기술의 개발을 촉진하고 있습니다. 이러한 촉진요인을 종합하면, 성능 신뢰성, 운영 효율성, 시스템 내결함성에 대한 관심이 높아지고 있음을 알 수 있습니다.

세계의 방위용 액추에이션 시스템 시장에 대해 조사 분석했으며, 시장에 영향을 미치는 기술, 향후 10년간의 예측, 각 지역별 동향 등의 정보를 전해드립니다.

용도별

지역별

유형별

북미

성장 촉진요인, 억제요인, 과제

PEST

주요 기업

공급업체 Tier 상황

기업 벤치마킹

유럽

중동

아시아태평양

남미

미국

방위 프로그램

최신 뉴스

특허

이 시장에서의 현재 기술 성숙도

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카공화국

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

The Global Defense Actuation System market is estimated at USD 6.75 billion in 2026, projected to grow to USD 17.69 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 10.11% over the forecast period 2026-2036.

Introduction to Global Defense Actuation Systems

Global defense actuation systems enable controlled mechanical movement that translates electronic or manual commands into physical action across military platforms. These systems operate at the core of motion-critical functions, including directional control, force application, stabilization, and positioning of key subsystems. Their reliability directly influences platform safety, operational accuracy, and mission continuity. In contemporary defense environments, actuation systems must perform consistently under extreme mechanical stress, hostile operating conditions, and prolonged deployment cycles. They support coordinated interaction between sensors, control software, and mechanical assemblies, ensuring predictable behavior during high-speed or high-load operations. As defense platforms evolve toward integrated and automated architectures, actuation systems are increasingly designed as precision control enablers rather than standalone mechanical elements. Their role extends across aircraft maneuvering, naval steering, ground vehicle mobility, and weapon alignment. The growing complexity of defense platforms has elevated the strategic importance of actuation systems, positioning them as essential contributors to responsiveness, survivability, and overall platform effectiveness within modern military forces.

Technology Impact in Global Defense Actuation Systems

Technological development has redefined how defense actuation systems are designed and deployed. Modern solutions emphasize digital command interfaces, enabling precise execution of motion with continuous feedback control. Sensor-embedded actuators provide real-time performance awareness, allowing systems to adjust dynamically to changing operational loads. Advances in materials engineering support compact designs that deliver higher output while reducing structural mass. Electrically driven actuation architectures improve efficiency and simplify integration with automated control systems. Diagnostic intelligence embedded within actuators supports condition-based maintenance, improving availability and reducing unplanned downtime. Enhanced signal integrity and fault tolerance strengthen reliability in electronically challenged environments. These technological shifts allow actuation systems to function as intelligent motion modules that enhance coordination, accuracy, and control across complex defense platforms.

Key Drivers in Global Defense Actuation Systems

The demand for advanced defense actuation systems is driven by multiple operational and strategic factors. Platform modernization initiatives require motion control solutions compatible with digital and automated environments. Increased adoption of remotely operated and autonomous systems places greater reliance on dependable mechanical execution without direct human intervention. Defense organizations also seek improved mission readiness through reduced maintenance burden and longer service intervals. Weight optimization efforts across air and land platforms support adoption of compact, high-performance actuators. Precision requirements in targeting, navigation, and stabilization further reinforce the need for advanced actuation solutions. Additionally, supply security considerations encourage development of trusted and locally supported actuation technologies. These drivers collectively highlight the growing emphasis on performance reliability, operational efficiency, and system resilience.

Regional Trends in Global Defense Actuation Systems

Regional approaches to defense actuation systems reflect differences in platform focus, industrial capability, and operational doctrine. Aerospace-focused regions prioritize lightweight, high-precision actuation for flight control and stability. Naval-oriented regions emphasize resistance to corrosion and sustained performance in maritime conditions. Regions with extensive land force requirements focus on ruggedized solutions designed for shock tolerance and mobility support. Emerging defense markets increasingly adopt modular actuation systems that allow incremental upgrades and cross-platform compatibility. Regional investment in domestic manufacturing and technical partnerships influences system design and lifecycle strategies. These trends demonstrate how actuation systems are adapted to meet localized defense needs while aligning with global priorities for precision, durability, and integration.

The Ministry of Defence entered into a contract with Hindustan Aeronautics Limited for the acquisition of 97 Light Combat Aircraft Mk1A for the Indian Air Force, comprising 68 single-seat fighters and 29 twin-seat variants, along with related equipment. Valued at more than ₹62,370 crore, excluding taxes, the agreement was signed on September 25, 2025. Deliveries are scheduled to begin in the 2027-28 timeframe and will be completed over a six-year period. The Mk1A aircraft will feature indigenous content exceeding 64 percent, with 67 additional systems and components incorporated beyond those included in the earlier LCA Mk1A contract signed. The integration of advanced domestically developed technologies, including the UTTAM Active Electronically Scanned Array radar, Swayam Raksha Kavach self-protection suite, and indigenous control surface actuators, will further reinforce India's Aatmanirbhar Bharat objectives in the defense aerospace sector.

By Application

By Region

By Type

The 10-year Defense Actuation Systems Market analysis would give a detailed overview of Defense Actuation Systems Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

The 10-year Defense Actuation Systems Market forecast of this market is covered in detailed across the segments which are mentioned above.

The regional Defense Actuation Systems Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Hear from our experts their opinion of the possible analysis for this market.