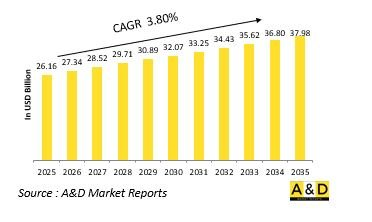

세계의 주력 전차 시장 규모는 2025년 261억 6,000만 달러에서 예측 기간 동안 3.80%의 연평균 복합 성장률(CAGR)로 성장을 지속하여 2035년에는 379억 8,000만 달러로 성장할 것으로 예측됩니다.

방위 분야의 주력 전차(MBT) 시장은 현대 지상전에서 핵심을 이루는 존재이며, 화력, 방어력 및 기동력을 겸비해 통상전부터 비대칭전까지 폭넓은 작전으로 우위성을 발휘하고 있습니다. 주력 전차는 장갑 부대의 핵심으로 다양한 지형과 전역에서 결정적인 전투 능력을 제공합니다. MBT의 진화는 다영역 통합 작전, 생존성, 정밀 공격 능력을 중시하는 현대의 군사 독트린에 의해 형성되어 왔습니다. 오늘날의 전차는 더 이상 고립된 전투 차량이 아니라 정찰부대, 드론, 사령부와 실시간으로 데이터를 공유할 수 있는 네트워크화된 전투 시스템이 되었습니다. 위협의 다양화에 따라 MBT의 역할은 직접 전투를 넘어서는 영역으로 확장되고 있습니다. 그들은 심리적 억지력으로서의 효과도 가지고 공세작전뿐만 아니라 평화유지활동에 있어서도 존재감을 발휘합니다. 첨단 장갑 소재, 디지털 화기관제 시스템, 액티브 보호 시스템(APS)의 도입으로 전차의 전투 즉응성이 대폭 향상되었습니다. 게다가 영토분쟁과 대규모 지상전의 재연이 장갑부대의 전략적 중요성을 재인식시키고 있습니다. 세계 각국에서 진행되는 근대화 프로그램 중에서 MBT는 기동성, 모듈성, 생존성 강화를 목표로 재설계되고 있으며, 급속히 진화하는 방위기술과 전투환경의 변화 속에서도 그 중요성을 유지하고 있습니다.

기술 혁신은 주력 전차의 능력을 재정의하고 고도로 네트워크화되고 유연하고 고내성의 전투 플랫폼으로 변모하고 있습니다. 복합 장갑이나 반응 장갑 등의 장갑 기술의 진보에 의해 운동 에너지탄이나 화학 에너지탄에 대한 생존성이 강화되고 있습니다. 또한 액티브 보호 시스템(APS)의 도입으로 대전차 유도 미사일(ATGM) 등의 위협을 요격, 무효화할 수 있어 승무원의 안전성이 비약적으로 향상되고 있습니다. 한편, 엔진 설계와 하이브리드 추진 기술의 진화에 의해 기동성, 연비 및 작전 행동 범위가 개선되어, 출력을 손상시키지 않고 운용 효율이 높아지고 있습니다. 디지털화도 주요 변화 요인입니다. 전장 관리 시스템의 통합으로 MBT는 상황 인식 데이터 공유, 드론과의 연계, 네트워크 중심전 환경에서의 운용이 가능하게 되었습니다. 또한 최신 화기관제 시스템과 광학장치가 정밀조준을 지원하여 악조건 하에서도 높은 명중 정밀도를 발휘합니다. 자동화나 AI 지원 기능에 의해 조작의 간략화와 승무원의 부담 경감도 진행되고 있습니다. 또한 무인화 및 옵션 유인화 전차의 등장은 전술적 유연성의 새로운 방향성을 나타내고 있습니다. 부가제조의 채용에 의한 부품 공급의 신속화나 모듈러 설계에 의한 유지관리성이나 업그레이드성의 향상도 진행되고 있습니다. 이러한 혁신으로 주력 전차는 앞으로도 기술적으로 고도인 미래 전투 환경에서 우위성을 유지할 수 있는 무기 시스템으로서 진화를 계속하고 있습니다.

주력 전차 수요는 안보상의 과제의 진화, 근대화의 필요성, 기술 진보라는 복합적인 요인에 의해 추진되고 있습니다. 지정학적 긴장의 고조와 고강도 전쟁의 재출현을 배경으로 각국의 군은 억지력과 즉응력을 강화하기 위해 장갑전력의 정비를 진행하고 있습니다. MBT는 그 중심적 존재이며, 육상전에서 압도적인 화력, 방어력 및 기동력을 제공합니다. 노후화된 전차의 근대화도 시장 성장을 지원하는 중요한 요소입니다. 많은 국가들이 구형 차량을 디지털 시스템, 첨단 센서, 개량 장갑으로 업그레이드하여 현대전의 요구에 적응시키고 있습니다. 또한 무인 시스템과 지휘 네트워크와의 상호 운용성 확보도 조달 정책에 영향을 미치고 있습니다. 게다가, 도시전이나 하이브리드전에의 대응을 목적으로, 경량으로 고기동인 MBT의 개발이 진행중입니다. 방위산업간의 협력과 국산화 추진 정책도 시장 확대를 지지하고 있으며, 장갑차량 제조의 자립성 강화를 목표로 하는 나라가 늘고 있습니다. 또한 추진 시스템, 생존성, 무장의 지속적인 혁신이 세계적으로 MBT 개발에 관심을 유지하고 있습니다. 이러한 모든 요인은 주력 전차를 억지력과 전투력 양면에서 필수적인 자산으로 자리 매김하고 있습니다.

본 보고서에서는 세계의 주력 전차 시장을 조사했으며, 시장 배경, 시장 영향요인 분석, 시장 규모 추이와 예측, 각종 구분, 지역별 상세 분석 등을 정리했습니다.

지역별

유형별

주력 전차 시장의 성장, 변화하는 동향, 기술 채용의 개요, 시장의 매력

시장에 영향을 미칠 것으로 예상되는 상위 10개 기술과 이러한 기술이 시장 전체에 미칠 수 있는 영향

북미

촉진요인, 제약, 과제

PEST

주요 기업

공급자 계층의 상황

기업 벤치마킹

유럽

중동

아시아태평양

남미

미국

방어 프로그램

최신 뉴스

특허

현재 기술 성숙도

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

The Global Main Battle Tank market is estimated at USD 26.16 billion in 2025, projected to grow to USD 37.98 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 3.80% over the forecast period 2025-2035.

The defense main battle tank market remains a cornerstone of modern land warfare, combining firepower, protection, and mobility to dominate in both conventional and asymmetric conflicts. Main battle tanks (MBTs) serve as the backbone of armored forces, providing decisive combat capability across varied terrains and operational theaters. The evolution of MBTs has been shaped by shifting military doctrines that emphasize multi-domain integration, survivability, and precision engagement. Modern tanks are no longer isolated battlefield platforms but networked systems capable of sharing data with reconnaissance units, drones, and command centers in real time. As threats evolve, the role of MBTs continues to expand beyond direct engagement. They serve as psychological deterrents, projecting strength and ensuring dominance during both offensive maneuvers and peacekeeping operations. The integration of advanced armor materials, digital fire-control systems, and active protection measures has elevated the combat readiness of these vehicles. Furthermore, the resurgence of territorial disputes and large-scale land conflicts has reaffirmed the strategic importance of armored formations. With modernization programs underway in multiple nations, MBTs are being redesigned for greater agility, modularity, and survivability, ensuring their continued relevance in an era of rapidly advancing defense technologies and changing combat dynamics.

Technological innovation is redefining the capabilities of main battle tanks, transforming them into highly networked, adaptive, and resilient combat platforms. Advancements in armor technology, such as composite and reactive armor systems, are enhancing survivability against kinetic and chemical energy projectiles. Active protection systems now enable tanks to detect and neutralize incoming threats like anti-tank guided missiles before impact, significantly improving crew safety. At the same time, advancements in engine design and hybrid propulsion are improving mobility, fuel efficiency, and operational range without compromising power. Digitalization is another major transformation driver. Integrated battlefield management systems allow MBTs to share situational awareness data, synchronize with drones, and operate as part of network-centric warfare environments. Modern fire-control systems and advanced optics enhance targeting precision, even under adverse conditions, while automation and AI-assisted functions are simplifying operations and reducing crew workload. The emergence of unmanned or optionally manned tank concepts further illustrates the direction of technological progress, offering new tactical flexibility. Moreover, the use of additive manufacturing for spare parts and modular designs simplifies maintenance and upgrades. These innovations collectively ensure that main battle tanks continue to evolve as technologically sophisticated platforms capable of maintaining dominance in future combat scenarios.

The demand for main battle tanks in the defense market is driven by a combination of evolving security challenges, modernization imperatives, and technological advancements. Increasing geopolitical tensions and the reemergence of high-intensity warfare have compelled militaries to strengthen their armored forces for deterrence and rapid response. MBTs are central to this strategy, offering unmatched firepower, protection, and shock effect in land-based combat operations. Modernization of aging fleets is a critical factor driving market growth. Many nations are upgrading legacy platforms with digital systems, advanced sensors, and improved armor configurations to meet modern warfare requirements. The push for interoperability with other battlefield assets, including unmanned systems and command networks, is also influencing procurement decisions. Additionally, the focus on urban warfare and hybrid conflict environments has led to the development of lighter, more agile MBTs capable of operating effectively in complex terrains. Defense industrial collaboration and indigenous production initiatives are also supporting demand, as countries seek self-reliance in armored vehicle manufacturing. Continuous innovation in propulsion, survivability, and weapon systems further sustains interest in MBT programs worldwide. Collectively, these factors underscore the enduring relevance of main battle tanks as essential assets in both deterrence and combat effectiveness.

Regional trends in the main battle tank market are shaped by distinct strategic priorities, industrial capabilities, and threat perceptions. In technologically advanced defense regions, modernization programs focus on next-generation MBTs equipped with active protection systems, digital connectivity, and hybrid propulsion. These areas emphasize innovation, seeking to develop highly survivable and networked platforms capable of performing within multi-domain operations. The goal is to maintain armored superiority through integration of AI-based decision support, automation, and advanced situational awareness systems. In contrast, regions facing persistent territorial disputes and internal conflicts prioritize rapid acquisition and modernization of cost-effective tanks to ensure deterrence and operational readiness. These nations often pursue upgrade packages for existing fleets, balancing capability enhancement with budget constraints. Meanwhile, defense-industrial cooperation and joint development programs are fostering cross-border collaborations, enabling emerging economies to access advanced technologies while building domestic manufacturing expertise. Environmental and logistical considerations are also influencing regional strategies, with a growing emphasis on fuel efficiency and sustainability in armored vehicle design. Furthermore, the increasing focus on export-oriented production has expanded global competition, with countries positioning themselves as suppliers of advanced MBT solutions to allied and developing nations. These regional dynamics collectively shape the evolving landscape of the global main battle tank market.

The Indian Ministry of Defence has signed a $248-million contract with Rosoboronexport to supply advanced engines for the Indian Army's T-72 Ural main battle tanks. As part of the agreement, the Russian state-owned defense exporter will deliver 1,000-horsepower engines to replace the older 780-horsepower units currently installed on India's Soviet-era T-72 fleet. The army presently operates around 2,500 of these tanks, which have been in service since their production in the 1970s. The contract also includes a technology transfer arrangement that will enable India's state-run Armoured Vehicles Nigam Ltd. to locally manufacture the new engines under license, supporting domestic production and maintenance capabilities.

By Region

By Type

The 10-year Main Battle Tank Market analysis would give a detailed overview of Main Battle Tank Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

The 10-year Main Battle Tank Market forecast of this market is covered in detailed across the segments which are mentioned above.

The regional Main Battle Tank Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Hear from our experts their opinion of the possible analysis for this market.