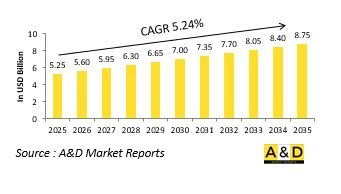

세계 소나 시스템 시장 규모는 2025년 52억 5,000만 달러에서 예측 기간 동안 5.24%의 CAGR로 2035년에는 87억 5,000만 달러로 성장할 것으로 예상됩니다.

방위용 소나(음파탐지) 시스템은 해상 상황 인식에 필수적인 도구로 수중 감시, 항해, 위협 탐지에 핵심적인 역할을 하고 있습니다. 이 시스템은 음파를 발신하고 반사되어 돌아오는 에코를 분석하여 수면 아래 물체를 식별, 위치 확인 및 추적합니다. 방위 분야에서 소나는 대잠수함전, 기뢰 탐지, 전략적인 해군 자산 보호에 널리 활용되고 있습니다. 수중 우위의 전략적 중요성은 현대 해군에게 소나 시스템을 필수적인 요소로 만들고 있으며, 특히 수중 위협이 점점 더 고도화되고 기존 수단으로는 탐지하기 어려워짐에 따라 그 필요성이 더욱 커지고 있습니다. 방위용 소나 시스템은 잠수함, 수상함정, 무인잠수함, 수중 고정시설 등 다양한 플랫폼에 배치되고 있습니다. 또한, 해양 영역 인식을 강화하기 위해 광범위한 해군 지휘 및 통제 프레임워크와 통합되는 경우가 많습니다. 수중전 전술이 진화함에 따라 보다 민감하고 적응력이 뛰어나며 스텔스에 대응할 수 있는 탐지 기술에 대한 수요도 증가하고 있습니다. 전 세계 군사 계획가들은 강력한 수중 감시 솔루션의 필요성을 점점 더 많이 인식하고 있으며, 방위용 소나 시스템은 해군의 즉각적인 대응력에 중요한 요소로 자리 잡고 있습니다. 이러한 수중 안보에 대한 전 세계적인 관심은 연안 해역 감시, 요충지 보호, 감시 레이더 라인 및 국가 해양 이익 보호와 같은 전략적 필연성을 반영합니다.

기술의 발전은 방위용 소나 시스템의 능력을 크게 변화시켰고, 탐지 정확도 향상, 작전 범위 확대, 위협 식별 개선 등을 가져왔습니다. 디지털 신호 처리를 통해 현대의 소나 시스템은 배경 소음을 제거하고 유사한 음향 특성을 가진 물체를 구별하여 수중 환경의 보다 선명한 이미지를 제공 할 수 있습니다. 또한, AI와 머신러닝을 통합하여 음향 데이터를 실시간으로 해석하고, 작업자가 수중 위협을 신속하게 식별하고 분류할 수 있도록 지원합니다. 재료 과학의 발전은 더 작고 가벼운 송수신기(트랜스듀서)의 개발에 기여하여 무인 시스템을 포함한 더 광범위한 플랫폼에 소나를 탑재할 수 있게 되었습니다. 저주파 능동형 소나는 탐지 범위를 확대하고, 고주파 소나는 지뢰와 장애물에 대한 상세한 해상도를 제공합니다. 또한, 합성개구부 소나를 이용하여 고해상도 해저지도를 제작할 수 있어 복잡한 환경에서의 항해 및 작전 계획을 지원하고 있습니다. 또한, 네트워크 기술을 통해 여러 함정 및 지휘소 간에 소나 데이터를 공유할 수 있게 되어 통합적인 해양 상황 파악이 가능해졌습니다. 이러한 기술 혁신은 소나를 전술적 도구에서 전략적 자산으로 진화시켜 해군이 진화하는 수중 위협에 보다 효과적으로 대응할 수 있도록 돕고 있습니다.

몇 가지 전략적, 작전적 요인으로 인해 전 세계 군대에서 방위용 소나 시스템에 대한 관심이 높아지고 있습니다. 첨단 잠수함과 기뢰의 확산 등 수중 위협이 증가함에 따라 국방 기관은 보다 진보된 탐지 및 추적 기술에 대한 투자를 강화하고 있습니다. 영토 분쟁과 해양경계 감시 및 집행의 필요성도 각국이 수중 감시 능력을 강화하는 요인이 되고 있습니다. 또한, 파이프라인과 통신 케이블과 같은 해저 인프라의 확장은 수중 활동을 보다 면밀하게 모니터링하는 것이 필수적이어서 소나 시스템의 중요성이 더욱 커지고 있습니다. 해군 현대화 프로그램에서는 첨단 센서군이 새로운 플랫폼의 표준 기능으로 통합되고 있으며, 소나는 미래 해양 작전의 주요 추진 요소로 자리매김하고 있습니다. 또한, 음향 조건이 더 까다로운 해안 환경에서 작동할 수 있는 시스템에 대한 수요도 증가하고 있습니다. 해군 임무에서 무인 및 자율 시스템의 사용 확대는 원격 또는 장기 배치에 적합한 소형 및 에너지 절약형 소나 유닛의 개발에 영향을 미치고 있습니다. 또한, 동맹국 해군 간의 상호 운용성의 필요성은 표준화된 음향 기술의 채택을 촉진하고 있습니다. 이 모든 요인들이 방위용 소나 시스템을 수중 상황 인식을 유지하고 평시 및 유사시 해양 우위를 확보하기 위한 중요한 투자 분야로 인식하고 있습니다.

세계의 소나 시스템 시장을 조사했으며, 시장 배경, 시장 영향요인 분석, 시장 규모 추정 및 예측, 각종 부문별·지역별 상세 분석 등의 정보를 정리하여 전해드립니다.

플랫폼별

지역별

용도별

이 장에서는 시장 성장에 대한 자세한 개요, 변화하는 시장 역학, 기술 도입 개요, 전체 시장의 매력도를 다룹니다.

향후 이 시장에 영향을 미칠 것으로 예상되는 10대 기술과 그 기술이 시장 전체에 미칠 수 있는 영향에 대해 설명합니다.

시장 예측은 위의 부문별로 상세하게 제시되어 있습니다.

시장 동향, 추진 요인, 억제요인, 도전 과제와 더불어 정치, 경제, 사회, 기술(PEST) 측면이 이 부문에서 다뤄집니다. 또한 지역별 시장 예측과 시나리오 분석도 상세히 설명합니다. 지역 분석의 마지막 부분에는 주요 기업 프로파일링, 공급업체 현황, 기업 벤치마킹이 포함되어 있습니다. 현재 시장 규모는 표준 시나리오를 기준으로 추정한 것입니다.

북미

촉진요인, 제약요인, 과제

PEST

주요 기업

공급업체 계층구조

기업 벤치마킹

유럽

중동

아시아태평양

남미

시장의 주요 방위 프로그램을 다루고, 이 분야에서 출원된 최신 뉴스와 특허를 소개합니다. 또한, 국가별 10년 시장 전망과 시나리오 분석도 이 장에서 다루고 있습니다.

미국

방위 프로그램

최신 뉴스

특허

이 시장의 현재 기술 성숙도

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카공화국

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

The Global SONAR Systems market is estimated at USD 5.25 billion in 2025, projected to grow to USD 8.75 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 5.24% over the forecast period 2025-2035.

Defense SONAR (Sound Navigation and Ranging) systems are vital tools for maritime situational awareness, playing a central role in underwater surveillance, navigation, and threat detection. These systems function by emitting sound pulses and interpreting the returning echoes to identify, locate, and track objects beneath the surface. In the defense sector, SONAR is used extensively for anti-submarine warfare, mine detection, and the protection of strategic naval assets. The strategic importance of underwater dominance has made SONAR systems indispensable for modern navies, especially as underwater threats become more sophisticated and harder to detect through conventional means. Defense SONAR systems are deployed on a variety of platforms, including submarines, surface vessels, unmanned underwater vehicles, and fixed ocean installations. They are often integrated with broader naval command and control frameworks to enhance maritime domain awareness. As underwater warfare tactics evolve, so too does the requirement for more sensitive, adaptable, and stealth-resistant detection technologies. Around the world, military planners are increasingly recognizing the need for robust underwater monitoring solutions, making defense SONAR systems a critical component of naval readiness. This global emphasis on underwater security reflects the strategic imperative to monitor littoral zones, secure chokepoints, and protect Surveillance Radar lines and national maritime interests.

Advancements in technology have significantly transformed the capabilities of defense SONAR systems, leading to enhanced detection accuracy, greater operational range, and improved threat classification. Digital signal processing has allowed modern SONAR systems to filter background noise, distinguish between objects with similar acoustic profiles, and provide clearer imagery of the underwater environment. The integration of artificial intelligence and machine learning enables real-time interpretation of acoustic data, allowing operators to quickly identify and categorize underwater threats. Improvements in materials science have contributed to the development of more compact and lightweight transducers, making it easier to deploy SONAR on a broader range of platforms, including unmanned systems. Low-frequency active SONAR systems have expanded detection range capabilities, while high-frequency systems offer detailed resolution for mine and obstacle detection. Additionally, the use of synthetic aperture SONAR has enabled the creation of high-resolution seabed maps, supporting navigation and mission planning in complex environments. Networking technologies have also made it possible for SONAR data to be shared across multiple vessels and command centers, creating a more unified and informed maritime picture. These innovations have collectively elevated SONAR from a tactical tool to a strategic asset in defense planning, enabling navies to respond more effectively to evolving underwater threats.

Several strategic and operational factors are driving the increased focus on defense SONAR systems across global military forces. Rising underwater threats, including the proliferation of advanced submarines and naval mines, are pushing defense agencies to invest in more capable detection and tracking technologies. Territorial disputes and maritime boundary enforcement needs are also prompting countries to bolster their underwater surveillance capabilities. The expansion of undersea infrastructure such as pipelines and communication cables has made it essential to monitor subsea activity more closely, further elevating the importance of SONAR systems. Naval modernization programs are incorporating advanced sensor suites as standard features on new platforms, positioning SONAR as a key enabler of future maritime operations. There is also growing demand for systems that can operate in littoral environments where acoustic conditions are more challenging. The increasing use of unmanned and autonomous systems in naval missions is influencing the development of compact, energy-efficient SONAR units designed for remote or extended deployments. In addition, interoperability between allied navies is encouraging the adoption of standardized acoustic technologies. All these factors contribute to making defense SONAR systems a critical area of investment for maintaining underwater situational awareness and ensuring maritime dominance in both peacetime and conflict scenarios.

Regional trends in defense SONAR system development and deployment reflect the specific security concerns, maritime geography, and strategic objectives of different areas. In North America, particularly within the United States, there is a strong emphasis on enhancing undersea warfare capabilities through investment in multi-frequency SONAR systems, to support both open-ocean operations and complex littoral missions. European nations are focusing on modernizing legacy fleets with quieter, more energy-efficient SONAR solutions that can seamlessly integrate with NATO's collective maritime defense infrastructure. The emphasis in this region often lies in balancing performance with compliance to environmental standards, particularly in sensitive marine ecosystems. In the Asia-Pacific, growing maritime tensions and rapid naval expansion are driving countries to develop indigenous SONAR technologies suited for archipelagic and deep-sea environments. Regional powers are also emphasizing the use of SONAR in conjunction with unmanned platforms to extend surveillance coverage. The Middle East is increasingly interested in protecting key maritime trade routes and offshore infrastructure, leading to an uptick in fixed and mobile SONAR installations for both defensive and monitoring purposes. Meanwhile, countries in Africa and Latin America are gradually adopting portable and scalable SONAR systems, often through international cooperation, to improve maritime domain awareness in coastal and exclusive economic zones.

Lockheed Martin Corporation's (LMT) Rotary and Mission Systems division has secured a contract modification from the Naval Sea Systems Command, Washington, D.C., to deliver engineering design, development, and production support for Sound Navigation and Ranging (Sonar) systems. The contract, valued at $197.5 million, is scheduled for completion by September 2026, with most of the work to be carried out in Manassas, VA, and Clearwater, FL. Growing geopolitical tensions in recent years have driven governments worldwide to boost defense investments, particularly in sonar technologies, to meet the rising need for advanced seabed mapping, improved underwater surveillance, and deployment of next-generation sonar-equipped vessels.

By Platform

By Region

By Application

The 10-year SONAR systems market analysis would give a detailed overview of SONAR systems market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

The 10-year SONAR systems market forecast of this market is covered in detailed across the segments which are mentioned above.

The regional SONAR systems market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Hear from our experts their opinion of the possible analysis for this market.