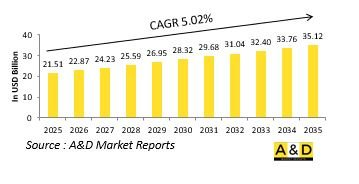

세계 스마트 무기 시장 규모는 2025년에 215억 1,000만 달러, 2035년에는 351억 2,000만 달러에 달할 것으로 예상되며, 예측 기간인 2025-2035년 연평균 5.02% 성장할 것으로 예측됩니다.

기술은 스마트 무기의 지속적인 진화에서 핵심적인 역할을 하며, 성능 향상, 비용 효율성, 적응성을 촉진합니다. 마이크로 일렉트로닉스, AI, 첨단 소재의 혁신은 정밀유도탄의 능력을 크게 향상시키고 있습니다. AI와 머신러닝을 통해 스마트 무기는 센서의 데이터를 실시간으로 처리할 수 있게 되었고, 이동하는 표적을 추적하고, 대응책을 회피하고, 비행 중 동적 판단을 할 수 있게 되었습니다. 위성 기반 내비게이션과 관성 유도 시스템은 GPS를 사용할 수 없는 환경에서도 정확도를 향상시키고 있습니다. 또한, 데이터 융합의 발전으로 여러 센서가 연동되어 조준 정확도와 환경 인식이 향상되고 있습니다. 통신 프로토콜이 강화됨에 따라 스마트 무기는 더 큰 지휘 통제 네트워크에 통합되어 비행 중에 업데이트 된 작전 매개 변수를 수신하고 실시간 인텔리전스를 기반으로 코스를 조정할 수 있습니다. 또한, 부품의 소형화로 인해 드론에서 핸드헬드 런처에 이르기까지 보다 다양한 플랫폼에 이러한 기술을 쉽게 적용할 수 있습니다. 또한, 모듈식 설계 추세로 인해 전체 시스템을 재설계하지 않고도 다양한 작전 요건에 맞게 스마트 무기를 신속하게 조정할 수 있게 되었습니다. 이러한 기술 발전은 스마트 무기의 전술적 범용성을 확대할 뿐만 아니라, 보다 광범위한 군의 채택 문턱을 낮춰 기술 선진국과 신흥 국방 강국의 미래 작전 방침을 형성할 것입니다.

여러 전략적, 전술적, 기술적 요인이 세계 스마트 무기 수요의 확대를 촉진하고 있습니다. 주요 촉진요인 중 하나는 현대 전투에서 높은 작전 효과를 유지하면서 민간인 사상자 및 인프라 피해를 최소화하기 위한 정확성의 필요성이 증가하고 있다는 점입니다. 전쟁이 도시와 비대칭 환경으로 이동함에 따라 부수적 피해를 최소화하는 표적 공격에 대한 요구사항이 더욱 중요해지고 있습니다. 스마트 무기는 선제공격 성공 가능성을 높여 작전당 필요한 탄약 수를 줄여 예산 효율화에도 일조하고 있습니다. 비국가주체, 드론, 분산된 적 조직 등 진화하는 위협 환경은 빠르게 움직이는 목표와 숨겨진 목표에 대응할 수 있는 적응형 무기를 필요로 합니다. 전략적 억제력도 그 촉진요인 중 하나이며, 스마트 무기는 기술적-군사적 우위를 알리는 힘의 과시 도구로 기능합니다. 또한, 연합군 내 상호운용성 또한 공동 또는 연합 플랫폼에서 운용할 수 있는 표준화된 네트워크 지원 탄약에 대한 수요를 촉진하고 있습니다. 국방 현대화 프로그램에서는 항상 스마트 무기를 통합하여 경쟁국과의 동등성을 유지하거나 우위를 점하기 위해 노력하고 있습니다. 디지털화된 다영역 작전으로의 전환은 공중, 해상, 육상, 사이버 환경 전반에 걸쳐 원활하게 작동하는 무기 시스템에 대한 수요를 더욱 강조하고, 그 작전적 가치를 높이고 있습니다.

스마트 무기의 개발 및 배치에 있어 지역 역학은 중요한 역할을 하고 있습니다. 북미, 특히 미국에서는 스마트 무기를 보다 광범위한 디지털 전장에 통합하는 데 중점을 두고 있으며, 종종 우주 기반 감시 및 실시간 데이터 공유 플랫폼과 연계하는 경우가 많습니다. 유럽 국가들은 특히 긴급 대응 및 평화 유지 작전에 사용하기 위한 상호 운용성과 자율 표적 시스템에 중점을 두고 공동 방위 구상에 대한 투자를 늘리고 있습니다. 아시아태평양은 특히 해군력과 공군력을 확대하는 국가들의 영토 분쟁과 군사 현대화 추진에 힘입어 큰 폭의 성장세를 보이고 있습니다. 중동의 경우, 지역적 갈등과 진행 중인 분쟁으로 인해 억지 및 적극적 개입을 위한 스마트 무기의 채택이 가속화되고 있으며, 많은 경우 인구 밀집 지역에서 민간인 피해를 최소화하는 데 초점을 맞추었습니다. 라틴아메리카와 아프리카의 신흥 경제권은 대규모 정비 없이 기존 플랫폼에 통합할 수 있는 비용 효율적인 스마트 탄약에 대한 관심이 높아지고 있습니다. 이들 지역에서는 외국 공급업체에 대한 의존도를 낮추기 위한 국내 개발 프로그램을 통해 지역 기반의 기술 혁신이 일어나고 있습니다. 이러한 지역 동향은 스마트 무기의 통합을 통해 현대 분쟁 시나리오에서 정확성, 확장성, 전략적 통제를 달성하는 데 대한 공통된 관심을 강조하고 있습니다.

세계의 스마트 무기 시장에 대해 조사 분석했으며, 성장 촉진요인, 향후 10년간의 전망, 지역별 동향 등의 정보를 전해드립니다.

지역별

내비게이션 별

유형별

북미

성장 촉진요인 및 억제요인, 과제

PEST

주요 기업

공급업체 Tier 상황

기업 벤치마킹

유럽

중동

아시아태평양

남미

미국

방위 프로그램

최신 뉴스

특허

이 시장에서의 현재 기술 성숙도

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카공화국

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

The global Smart Weapons market is estimated at USD 21.51 billion in 2025, projected to grow to USD 35.12 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 5.02% over the forecast period 2025-2035.

Smart weapons, often referred to as precision-guided munitions, represent a transformative leap in modern warfare, redefining the accuracy, lethality, and efficiency of military operations. These advanced systems integrate sophisticated guidance technologies, sensors, and real-time data processing capabilities to strike designated targets with minimal collateral damage. Unlike conventional armaments, smart weapons can adapt to changing battlefield conditions and engage targets with pinpoint precision. Their use spans across various platforms, including air-launched missiles, naval strike systems, and ground-based artillery. The evolution of smart weapons is closely linked to the broader trend of digital warfare, where connectivity, automation, and situational awareness play central roles. As militaries around the world seek to modernize their arsenals, smart weapons have become a key area of investment, particularly in scenarios requiring fast, decisive action. Their ability to reduce mission risk and enhance operational success makes them highly valuable in both conventional and asymmetric conflicts. The global defense community continues to prioritize the development and deployment of these systems as strategic assets, aiming to gain tactical superiority and deter adversaries with advanced, network-enabled capabilities. As threats evolve, the role of smart weapons in achieving precise, scalable, and timely military responses becomes increasingly critical.

Technology plays a central role in the continuous evolution of smart weapons, driving performance improvements, cost-efficiency, and adaptability. Innovations in microelectronics, artificial intelligence, and advanced materials have significantly enhanced the capabilities of precision-guided munitions. With AI and machine learning, smart weapons can process sensor data in real time, enabling them to track moving targets, avoid countermeasures, and make dynamic decisions during flight. Satellite-based navigation and inertial guidance systems have improved accuracy, even in GPS-denied environments. In addition, advancements in data fusion allow multiple sensors to work together, enhancing targeting precision and environmental awareness. Enhanced communication protocols enable smart weapons to integrate into larger command-and-control networks, allowing them to receive updated mission parameters mid-flight and adjust course based on live intelligence. Miniaturization of components also facilitates the deployment of these technologies across a wider range of platforms, from drones to handheld launchers. Furthermore, modular design trends are allowing for quicker adaptation of smart weapons to different mission requirements without redesigning entire systems. These technological advances not only extend the tactical versatility of smart weapons but also lower the threshold for adoption by a wider range of military forces, ultimately shaping the future operational doctrines of technologically advanced and emerging defense powers alike.

Several strategic, operational, and technological factors are fueling the growing demand for smart weapons worldwide. One of the primary drivers is the increasing need for precision in modern combat to minimize civilian casualties and infrastructure damage while maintaining high mission effectiveness. As warfare shifts toward urban and asymmetric environments, the requirement for targeted strikes with minimal collateral impact becomes even more critical. Budget efficiency also plays a role, as smart weapons reduce the number of munitions needed per mission by increasing the likelihood of a first-strike success. Evolving threat landscapes-marked by non-state actors, drones, and dispersed enemy formations-require adaptable weapons capable of engaging fast-moving or concealed targets. Strategic deterrence is another motivator, with smart weapons serving as tools of power projection that convey technological and military superiority. In addition, interoperability within allied forces is driving the need for standardized, network-enabled munitions that can operate across joint or coalition platforms. Defense modernization programs are consistently integrating smart weapons to maintain parity or gain an edge over peer competitors. The shift toward digitized, multi-domain operations further underscores the demand for weapons systems that can function seamlessly across air, sea, land, and cyber environments, amplifying their operational value.

Regional dynamics play a significant role in shaping the development and deployment of smart weapons. In North America, especially within the United States, there is a strong emphasis on integrating smart weapons into a broader digital battlespace, often linked with space-based surveillance and real-time data-sharing platforms. European nations are increasingly investing in collaborative defense initiatives, with a focus on interoperability and autonomous targeting systems, especially for use in rapid-response and peacekeeping missions. The Asia-Pacific region is seeing significant growth, fueled by territorial tensions and a drive for military modernization, particularly among countries with expanding naval and aerial capabilities. In the Middle East, regional rivalries and ongoing conflicts have accelerated the adoption of smart weapons for both deterrence and active engagement purposes, often with a focus on minimizing civilian harm in densely populated areas. Emerging economies in Latin America and Africa are showing increasing interest in cost-effective smart munitions that can be integrated into existing platforms without extensive overhaul. Across these regions, localized innovation is also beginning to emerge, with indigenous development programs aiming to reduce dependency on foreign suppliers. These regional trends highlight a common interest in achieving precision, scalability, and strategic control in modern conflict scenarios through the integration of smart weapons.

Raytheon, an RTX business, has secured a $400 million contract from the U.S. Air Force to manufacture and supply over 1,500 StormBreaker(R) smart weapons. This advanced air-to-surface, network-enabled system is designed to strike moving targets in all weather conditions, equipped with a tri-mode seeker and multi-effects warhead. Currently deployed on the F-15E Strike Eagle and F/A-18E/F Super Hornet, StormBreaker is also undergoing testing across all F-35 variants. In 2023, the weapon system successfully completed 28 test drops across platforms.

By Region

By Navigation

By Type

The 10-year Smart Weapons Market analysis would give a detailed overview of Smart Weapons Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

The 10-year smart weapons market forecast of this market is covered in detailed across the segments which are mentioned above.

The regional smart weapons market rends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Hear from our experts their opinion of the possible analysis for this market.