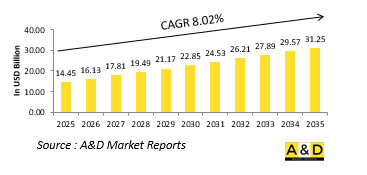

세계의 전술 커뮤니케이션 시장 규모는 2025년에 144억 5,000만 달러로 추정되고, 2035년까지 312억 5,000만 달러로 성장할 것으로 예측되며, 예측 기간인 2025-2035년 연간 평균 성장률(CAGR) 8.02%로 성장이 전망되고 있습니다.

국방 전술 커뮤니케이션은 작전 환경에서 실시간 안전한 정보 교환을 가능하게 함으로써 군사 작전의 백본으로서 기능합니다. 육지, 하늘, 바다, 사이버의 각 영역을 포함한 다양한 부대의 지휘 통제를 지원합니다. 그 주된 목적은 가혹하고 예측 불가능한 상황 하에서 신속하고 신뢰성 높은 커뮤니케이션을 촉진함으로써 임무를 확실하게 성공시키는 것입니다. 전략적 또는 관리적 목적을 달성할 수 있는 광범위한 방위 커뮤니케이션 시스템과 달리 전술 시스템은 기동성, 회복력, 적응성을 위해 구축됩니다. 이러한 네트워크는 전투, 평화 유지, 긴급 지원의 역할을 불문하고 적극적인 전개 중에 사용됩니다. 군사 작전이 진화함에 따라 커뮤니케이션 요구의 복잡성도 증가하고 있습니다. 전술 시스템은 기존 네트워크가 위험에 처하거나 이용할 수 없게 되는 적대적인 환경에서도 기능해야 합니다. 상황 인식 유지, 자산 조정, 위협에 대한 신속한 대응에 중요한 역할을 합니다. 무인 시스템이나 인공지능과 같은 새로운 기술과의 통합은 이러한 커뮤니케이션 플랫폼의 중요성을 더욱 확대합니다. 다자간 공동작전 사례가 증가하는 가운데 상호운용성과 국경을 초월한 안전한 정보교환은 매우 중요합니다. 효과적인 전술 커뮤니케이션은 임무 수행을 지원할 뿐만 아니라 역동적이고 이해관계가 큰 시나리오에서의 연계를 강화하고 리스크를 경감함으로써 요원의 안전을 지키는 데도 도움이 됩니다.

기술의 진보는 방위 전술 커뮤니케이션의 정세를 재구축해, 스피드, 정밀도, 내장해성에 새로운 가능성을 가져오고 있습니다. 소프트웨어 정의 무선, 메쉬 네트워크, 위성 강화 연결 등의 기술 혁신은 부대가 실시간으로 통신하는 방식을 확 바꿔놓았습니다. 이러한 도구는 원격지나 전자적인 다툼이 있는 환경에서도 분산화된 부대가 연결을 유지할 수 있도록 합니다. 인공지능과 머신러닝은 현재 방대한 전장 데이터를 처리하고 실행 가능한 인사이트에 우선순위를 매김으로써 보다 신속한 의사결정을 지원하고 있습니다. 엣지 컴퓨팅은 로컬 데이터 분석을 가능하게 하여 중앙 사령부에 대한 의존을 줄이고 작전 대응을 신속화합니다. 암호화 기준은 보다 세련되어 감청이나 사이버 침입으로부터의 보호를 제공합니다. 클라우드 기반 인프라와 디지털 트윈을 통해 플래닝과 시뮬레이션 능력이 강화되고 작전 개시 전 준비 태세가 강화됩니다. 한편, 소형화의 진전으로 보다 많은 장비를 개인 장비에 통합할 수 있게 되어 기동성을 희생하지 않고 병사 개인의 능력이 향상되고 있습니다. 상호운용성 과제는 레거시 시스템을 차세대 기술과 연결시키는 통합 플랫폼에 의해 해결되어 보다 원활한 연합 활동을 가능하게 하고 있습니다. 이러한 기술 혁신은 기존의 군사 작전을 강화할 뿐만 아니라 사이버 방위, 우주 기반 자산, 하이브리드전 시나리오 등 전술적 커뮤니케이션의 범위를 넓히고 있습니다. 이처럼 기술은 촉매와 이네블러 모두의 역할을 해 전술 커뮤니케이션이 민첩하고 임무 대응 가능한 상태를 유지할 수 있도록 하고 있습니다.

방위용 전술 커뮤니케이션의 진화를 가속시키고 있는 주요 요인은 몇 가지입니다. 점점 복잡해지는 전투 환경에서는 분산된 부대 간의 원활한 연계가 요구되며, 많은 경우 다국적군과 멀티 도메인 편성으로 활동하고 있습니다. 이 때문에 육지, 하늘, 바다, 우주, 사이버의 각 영역에서 통합된 작전을 지원할 수 있는 시스템에 대한 요구가 높아지고 있습니다. 지정학적 긴장이 증가하고 예측할 수 없는 분쟁지대에는 전자전과 사이버 위협에 견딜 수 있는 견고하고 민첩한 커뮤니케이션 솔루션이 필요합니다. 또한 시가전과 비대칭적인 분쟁 환경도 유연하고 적응성이 높은 통신 플랫폼 수요에 기여하고 있습니다. 또 다른 큰 원동력은 군의 현대화이며, 각국은 레거시 시스템을 업그레이드하여 현대 및 미래 임무 요구 사항을 충족하려고합니다. 무인 차량, 자율형 플랫폼, 센서 네트워크의 역할이 높아짐에 따라 전술 커뮤니케이션이 대처해야 할 복잡성이 새롭게 생깁니다. 또한 실시간 데이터 공유 및 의사 결정으로의 전환은 저지연의 광대역 통신 채널을 더욱 강조합니다. 예산 배분과 국방 정책은 특히 정부가 디지털 변혁을 우선시하는 시스템 도입과 기술 혁신에 영향을 미칩니다. 마지막으로, 동맹군 간의 상호 운용성의 필요성은 표준화된 통신 프로토콜과 장비 개발의 중요한 힘이 되고 있습니다. 이러한 복합적인 압력이 전술 커뮤니케이션 시스템의 향후 방향성을 세계적으로 형성하고 있습니다.

지역 역학은 방위 전술 커뮤니케이션 시스템의 개발, 배포 및 우선 순위에 큰 영향을 미칩니다. 북미, 특히 미국에서는 세계의 전략적 이점을 유지하기 위해 레거시 플랫폼에 최첨단 기술을 통합하는 것이 중요합니다. 초점은 분쟁 환경에서도 운영할 수 있는 탄력적이고 다중 도메인 통신 능력을 구축하는 것입니다. 유럽에서는 공동 이니셔티브와 다국간 방위 협력이 동맹군 간의 상호 운용성과 표준화를 추진하는 원동력이 되고 있습니다. 여기에서 전술 커뮤니케이션 시스템은 국방과 집단 안보 모두 임무를 지원하도록 설계되었습니다. 아시아태평양에서는 해상 긴장 증가와 방위 예산 확대로 전술 커뮤니케이션 인프라의 현대화가 급속히 진행되고 있습니다. 이 지역의 국가들은 전통적인 전쟁 시나리오와 하이브리드 전쟁 시나리오 모두에 적합한 모바일로 적응 가능한 시스템에 투자하고 있습니다. 분쟁이 끊임없이 국내 안보의 과제에 직면하고 있는 중동에서는 도시에서도 사막지대에서도 기능하는 안전하고 신속한 전개가 가능한 시스템이 우선되고 있습니다. 한편, 아프리카와 라틴아메리카에서는 평화 유지 및 재해 대응의 역할을 중시하고 예산 제약과 능력의 균형을 맞춘 비용 효율적인 솔루션이 중시되고 있습니다. 어느 지역에서나 동향은 통합 네트워크 중심의 작전으로 향하고 있으며, 전술 커뮤니케이션이 방어 계획에서 평가되고 구현되는 방식의 보편적인 변화를 반영합니다.

라인메탈은 독일 연방군(Bundeswehr)에서 독일 전군에게 횡단적인 의미를 가지는 중요한 전술 커뮤니케이션 프로젝트의 대형 계약을 수주했습니다. 이 계약에 따라 라인메탈은 최대 19만 1,000유닛의 '청각보호장치 일체형 인컴시스템'을 공급하게 됩니다. 이 기본 계약은 7년간에 걸친 것으로, 순가치는 최대 4억 유로에 이를 수 있습니다. 이 프로젝트는 독일 연방의회 예산위원회에 의해 설정된 조건이 적용됩니다. 2024년 납품을 위해 접속 케이블을 포함한 3만 대의 초기 발주가 확정되었습니다. 추가로 30,000 유닛이 2025년에 납품될 예정입니다. 특별 기금을 통해 대출되는 이 두 배치는 순으로 최대 1억 4,000만 유로에 해당합니다.

본 보고서에서는 세계의 전술 커뮤니케이션 시장에 대해 조사했으며, 10년간의 부문별 시장 예측, 기술 동향, 기회 분석, 기업 프로파일, 국가별 데이터 등을 정리했습니다.

유형별

지역별

플랫폼별

기술별

이 장에서는 10년간의 전술 커뮤니케이션 시장 분석을 통해 전술 커뮤니케이션 시장의 성장, 변화하는 동향, 기술 채용의 개요 및 시장의 매력에 대한 상세한 개요를 제공합니다.

이 부문에서는 이 시장에 영향을 미칠 것으로 예상되는 상위 10개 기술과 이러한 기술이 시장 전체에 미칠 수 있는 영향에 대해 설명합니다.

이 시장의 10년간의 전술 커뮤니케이션 시장 예측은 위의 전체 부문에 걸쳐 상세하게 설명되어 있습니다.

이 부문에서는 지역별 전술 커뮤니케이션 시장 동향, 촉진요인, 억제요인, 과제, 그리고 정치, 경제, 사회, 기술 등의 측면을 포괄하고 있습니다. 또, 지역별의 시장 예측 및 시나리오 분석도 상세하게 다루고 있습니다. 지역 분석의 최종 단계에서는 주요 기업의 프로파일링, 공급업체의 정세, 기업 벤치마크 등에 대해 분석하고 있습니다. 현재 시장 규모는 일반 시나리오에 따라 추정되고 있습니다.

북미

촉진요인, 억제요인 및 과제

PEST

주요 기업

공급자 계층의 상황

기업 벤치마킹

유럽

중동

아시아태평양

남미

이 장에서는 이 시장에서 주요 방위 프로그램을 다루며 이 시장에서 신청된 최신 뉴스와 특허에 대해서도 설명하고, 국가 수준의 10년간 시장 예측 및 시나리오 분석에 대해서도 설명합니다.

미국

방위 프로그램

최신 뉴스

특허

이 시장의 현재 기술 성숙도

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

The global Tactical Communication market is estimated at USD 14.45 billion in 2025, projected to grow to USD 31.25 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 8.02% over the forecast period 2025-2035.

Defense tactical communication serves as the backbone of military operations by enabling real-time, secure exchange of information in operational environments. It supports command and control across various units including land, air, sea, and cyber domains. The primary aim is to ensure mission success by facilitating fast and reliable communication under harsh and unpredictable conditions. Unlike broader defense communication systems that may serve strategic or administrative purposes, tactical systems are built for mobility, resilience, and adaptability. These networks are used during active deployments, whether in combat, peacekeeping, or emergency support roles. As military operations evolve, so does the complexity of the communication needs. Tactical systems must function in hostile environments where traditional networks may be compromised or unavailable. They play a vital role in maintaining situational awareness, coordinating assets, and responding swiftly to threats. Integration with emerging technologies like unmanned systems and artificial intelligence further extends the importance of these communication platforms. With increasing instances of joint multinational operations, interoperability and secure cross-border information exchange are critical. Effective tactical communication not only supports mission execution but also safeguards personnel by enhancing coordination and reducing risks in dynamic, high-stakes scenarios.

Technological advancement is reshaping the landscape of defense tactical communication, introducing new possibilities for speed, accuracy, and resilience. Innovations such as software-defined radios, mesh networks, and satellite-enhanced connectivity have transformed how forces communicate in real-time. These tools allow decentralized units to stay connected, even in remote or electronically contested environments. Artificial intelligence and machine learning now support faster decision-making by processing vast amounts of battlefield data and prioritizing actionable insights. Edge computing enables local data analysis, reducing reliance on central command structures and speeding up operational responses. Encryption standards have become more sophisticated, offering protection against interception and cyber intrusions. Cloud-based infrastructures and digital twins enhance planning and simulation capabilities, fostering improved pre-mission preparation. Meanwhile, advancements in miniaturization allow more equipment to be integrated into personal gear, increasing individual soldier capabilities without sacrificing mobility. Interoperability challenges are being addressed through unified platforms that link legacy systems with next-generation technologies, enabling smoother coalition efforts. These innovations are not only enhancing traditional military operations but also broadening the scope of tactical communication to include cyber defense, space-based assets, and hybrid warfare scenarios. Technology thus acts as both a catalyst and an enabler, ensuring that tactical communication remains agile and mission-ready.

Several core factors are accelerating the evolution of defense tactical communication. Increasingly complex combat environments demand seamless coordination between dispersed units, often operating in multinational and multi-domain formations. This creates a growing need for systems that can support integrated operations across land, air, maritime, space, and cyber domains. Rising geopolitical tensions and unpredictable conflict zones require communication solutions that are both robust and agile, capable of withstanding electronic warfare and cyber threats. Urban warfare and asymmetric conflict settings also contribute to the demand for flexible and adaptive communication platforms. Another major driver is the modernization of armed forces, as countries seek to upgrade legacy systems to meet the requirements of contemporary and future missions. The growing role of unmanned vehicles, autonomous platforms, and sensor networks introduces new layers of complexity that tactical communication must address. Additionally, the shift toward real-time data sharing and decision-making places greater emphasis on low-latency, high-bandwidth communication channels. Budget allocations and defense policies also influence system adoption and innovation, especially as governments prioritize digital transformation. Finally, the need for interoperability among allied forces continues to be a major force behind the development of standardized communication protocols and equipment. These combined pressures are shaping the future direction of tactical communication systems globally.

Regional dynamics significantly influence how defense tactical communication systems are developed, deployed, and prioritized. In North America, particularly the United States, there is a strong emphasis on integrating cutting-edge technologies with legacy platforms to maintain global strategic advantage. The focus is on building resilient, multi-domain communication capabilities that can operate in contested environments. In Europe, joint initiatives and multinational defense collaborations drive the push for interoperability and standardization among allied forces. Here, tactical communication systems are designed to support both national defense and collective security missions. In the Asia-Pacific region, growing maritime tensions and expanding defense budgets have led to a surge in the modernization of tactical communication infrastructure. Countries in this area are investing in mobile, adaptable systems suited for both traditional and hybrid warfare scenarios. The Middle East, facing persistent conflict and internal security challenges, prioritizes secure, rapid-deployment systems that can function in both urban and desert terrains. Meanwhile, regions in Africa and Latin America focus on cost-effective solutions that balance capability with budget constraints, often emphasizing peacekeeping and disaster response roles. Across all regions, the trend is moving toward integrated, network-centric operations, reflecting a universal shift in the way tactical communication is valued and implemented in defense planning.

Rheinmetall has been awarded a major contract by the Bundeswehr for a key tactical communications project that holds cross-cutting significance for the entire German armed forces. Under this agreement, the technology group will supply up to 191,000 units of its "intercom system with integrated hearing protection." The framework contract spans seven years and has a potential net value of up to €400 million. The project is subject to conditions set by the Budget Committee of the German Bundestag. An initial order of 30,000 units, including connection cables, has been firmly placed for delivery in 2024. An additional 30,000 units are expected to be called off for delivery in 2025. These two batches, financed through the special fund, are valued at up to €140 million net.

By Type

By Region

By Platform

By Technology

The 10-year tactical communication market analysis would give a detailed overview of tactical communication market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

The 10-year tactical communication market forecast of this market is covered in detailed across the segments which are mentioned above.

The regional tactical communication market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Hear from our experts their opinion of the possible analysis for this market.