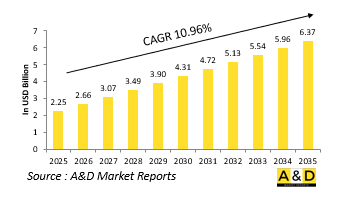

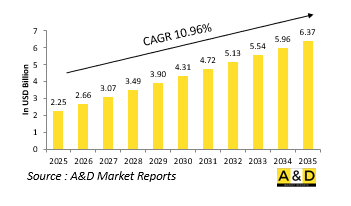

세계 공기역학 테스트 및 시뮬레이션 시장 규모는 2025년에 22억 5,000만 달러로 추정되며, 2035년까지 연평균 10.96%의 연평균 복합 성장률(CAGR)로 63억 7,000만 달러로 확대될 것으로 예상됩니다.

국방 공기역학 테스트 및 시뮬레이션 시장은 군용기, 미사일, 무인항공기 시스템의 설계, 시장 개척 및 운영 개선에 있어 매우 중요한 역할을 하고 있습니다. 국방 플랫폼이 고도화됨에 따라 공기역학적 성능은 기동성, 생존성, 연료 효율성 및 임무 효과에 직접적인 영향을 미칩니다. 테스트와 시뮬레이션을 통해 이러한 성능 매개변수를 통제된 극한 조건에서 안전하고 비용 효율적으로 평가할 수 있습니다. 풍동, 수치유체역학 도구 및 가상 비행 환경은 이 시장의 기반을 형성하며, 엔지니어와 전략가에게 복잡한 기체 전체의 기류, 열 분포 및 압력 역학을 모델링할 수 있는 능력을 제공합니다. 이러한 기능은 새로운 설계를 검증하고, 레거시 시스템을 개선하며, 다양한 환경 및 전투 조건에서 최적의 성능을 보장하는 데 필수적입니다. 또한, 공기역학 시뮬레이션은 스텔스 최적화, 무기 통합, 고속 비행 계획 등 현대전에서 중요한 요소들을 지원합니다. 또한, 이러한 기술은 실제 시나리오에서 차량의 거동을 정확하게 모델링할 수 있기 때문에 전략 수립에도 기여합니다. 공중전이 민첩성, 속도, 저관측성에 의존하게 되면서 공기역학 테스트 및 시뮬레이션의 중요성은 계속 증가하고 있습니다. 이 시장은 연구와 생산뿐만 아니라 오늘날의 진화하는 위협 환경에서 요구되는 지속적인 적응을 지원하고 있습니다.

새로운 기술은 물리 및 가상 환경 모두에서 더 높은 정확도, 확장성 및 현실감을 구현할 수 있도록 국방 항공역학 테스트 및 시뮬레이션의 환경을 변화시키고 있습니다. 고성능 컴퓨팅은 전산유체역학에 혁명을 가져왔으며, 분석가들은 매우 복잡한 유동 상태를 전례 없는 정확도와 속도로 시뮬레이션할 수 있게 되었습니다. 이러한 디지털 모델은 난류, 열 부하, 제어 표면 및 임베디드 무기 시스템 간의 상호 작용과 같은 다변량 시나리오를 고려할 수 있게 되었습니다. 머신러닝의 통합은 방대한 데이터 세트를 기반으로 성능 패턴을 식별하고 설계 반복을 최적화하여 시뮬레이션 출력을 더욱 정교하게 만듭니다. 이와 함께, 극한 고도 및 극한 속도 조건을 시뮬레이션하는 차세대 풍동은 극초음속 플랫폼과 조종 가능한 활공기 개발을 지원하기 위해 진화하고 있습니다. 또한, 가상현실과 몰입형 인터페이스는 엔지니어와 조종사가 공기역학 모델과 상호 작용하는 방식에 영향을 미치기 시작했으며, 공기역학 및 차량 거동에 대한 직관적인 통찰력을 제공합니다. 또한, 클라우드 기반 시뮬레이션 툴은 방위산업체, 연구기관, 군수업체들 간의 세계 협업과 안전한 데이터 공유를 가능하게 하고 있습니다. 이러한 기술의 융합은 개발 주기를 단축하고 시스템 검증을 강화하여 복잡한 공중 환경에서도 운영할 수 있는 보다 민첩하고 적응력 있는 방위 플랫폼에 기여하고 있습니다.

국방 공기역학 테스트 및 시뮬레이션 시장의 성장을 가속하는 몇 가지 주요 요인이 있습니다. 가장 중요한 요인 중 하나는 항공 전투 시스템의 복잡성으로, 진화하는 임무의 요구 사항을 충족하기 위해 고도의 공기역학적 프로파일이 필요합니다. 군용 항공기와 미사일은 광범위한 속도, 고도, 대기 조건에서 안정적으로 작동해야 하므로 엄격한 테스트와 고충실도 시뮬레이션이 필요합니다. 스텔스성이 현대 항공기에 대한 기대치가 높아짐에 따라, 공기역학적 형상은 성능과 안정성을 유지하면서 레이더 회피를 지원할 수 있도록 최적화되어야 합니다. 극초음속 기술의 등장은 기류 거동에 새로운 지평을 열었으며, 극한의 열 및 압력 조건에 대응할 수 있는 시뮬레이션 툴을 요구하고 있습니다. 또한, 라이프사이클 비용 절감과 효율적인 플랫폼 개발을 촉진하기 위해 비용이 많이 드는 물리적 테스트에 대한 의존도를 최소화할 수 있는 가상 테스트 환경의 사용이 권장되고 있습니다. 훈련 및 임무 리허설 시스템도 공기역학 시뮬레이션의 혜택을 받고 있으며, 항공기 승무원이 새로운 플랫폼이나 변경된 플랫폼의 핸들링 특성을 이해하는 데 도움을 주고 있습니다. 한편, 멀티롤 UAV와 부유탄에 대한 관심이 증가함에 따라 내구성, 탑재량 및 기동성을 위해 공기역학적 특성을 개선할 필요가 있습니다. 이러한 추진력은 개발뿐만 아니라 임무의 즉각적인 대응과 작전적 우위를 확보하는 데 있어서도 공기역학 시험의 역할이 확대되고 있음을 강조하고 있습니다.

세계 국방 항공역학 테스트 및 시뮬레이션 시장은 국가별 우선순위, 산업 역량, 첨단 항공우주 시스템에 대한 투자에 따라 뚜렷한 지역적 프로파일을 보이고 있습니다. 북미, 특히 미국의 경우, 시장은 탄탄한 국방 R&D 생태계와 풍동, 시뮬레이션 연구소, 비행 시험장 등 광범위한 인프라에 의해 뒷받침되고 있습니다. 이러한 시설들은 차세대 항공기 프로그램, 극초음속 무기 개발, 통합 방공 플랫폼을 지원하는 데 핵심적인 역할을 하고 있습니다. 유럽은 공동 연구 이니셔티브와 다국적 방위 프로그램에 중점을 두고 있으며, 그 결과 첨단 시뮬레이션 역량과 디지털 설계 허브에 대한 투자를 공유하고 있습니다. 프랑스, 독일, 영국과 같은 국가들은 국내 및 공동 항공우주 개발 노력을 지원하는 전용 테스트 시설을 유지하고 있습니다. 아시아태평양에서는 국내 국방 항공 프로그램의 급속한 발전으로 인해 국내 시뮬레이션 및 테스트 역량에 대한 수요가 증가하고 있습니다. 인도, 중국, 한국 등의 국가들은 외국 검증에 대한 의존도를 줄이고 자국 항공우주 개발 일정을 앞당기기 위해 기술 인프라를 확장하고 있습니다. 중동에서는 방위산업화에 대한 관심으로 국제적인 항공우주 기업과의 제휴가 진행되어 공기역학 모델링 및 검증의 현지 역량을 개발하고 있습니다. 각 지역의 궤적은 전략적 목표와 세계 방위 정세에서 진화하는 역할을 반영하고 있습니다.

미래 전투 항공 시스템(FCAS)은 국방 및 안보 주권을 유지하기 위한 유럽의 노력의 핵심이며, FCAS의 핵심은 차세대 무기 시스템(NGWS)으로 첨단 "시스템 오브 시스템"의 토대를 형성합니다. 이 통합 네트워크는 유인 차세대 전투기가 무인 원격 수송기와 함께 운영되며, 이 모든 것이 '전투 클라우드'(공중, 육상, 해상, 우주, 사이버 공간의 자산을 연결하는 안전한 데이터 네트워크)를 통해 원활하게 연결되는 것이 특징입니다. 이러한 상호 연결된 플랫폼은 센서, 이펙터, 명령 및 제어 노드 역할을 하여 신속하고 유연한 의사결정을 지원하며, FCAS를 지원하는 아키텍처는 개방형, 모듈화, 서비스 지향적이며, 미래 플랫폼과 신기술의 통합을 가능하게 합니다. 미래의 플랫폼과 신기술의 통합을 가능하게 합니다. 국가 및 동맹국 자산은 각자의 역량을 제공함으로써 NGWS를 보완하고, 상호 운용 가능한 네트워크화된 시스템의 총체적인 힘으로 여러 영역에 걸친 진정한 공동 전투 환경을 가능하게 합니다.

세계의 공기역학 테스트 및 시뮬레이션 시장에 대해 조사했으며, 향후 10년간의 분야별 시장 예측, 기술 동향, 기회 분석, 기업 프로파일, 국가별 데이터 등의 정보를 정리하여 전해드립니다.

이 장에서는 10년간에 걸치는 세계의 공기역학 테스트 및 시뮬레이션 시장 분석에 의해 세계의 공기역학 테스트 및 시뮬레이션 시장 성장, 변화하는 동향, 기술 채택 개요 및 전체적인 시장의 매력에 대해 상세한 개요가 나타납니다.

이 부문에서는 이 시장에 영향을 미치는으로 예상되는 상위 10기술과 이러한 기술이 시장 전체에 미칠 가능성이 있는 영향에 대해 설명합니다.

이 시장 10년간 세계의 공기역학 테스트 및 시뮬레이션 시장 예측은 상기 부문 전체로 상세하게 커버되고 있습니다.

이 부문에서는 지역별 대 드론 시장 동향, 촉진요인, 억제요인, 과제, 그리고 정치, 경제, 사회, 기술이라고 하는 측면을 망라하고 있습니다. 또한 지역별 시장 예측과 시나리오 분석도 상세하게 채택하고 있습니다.지역 분석 마지막에는 주요 기업 프로파일링, 공급업체 상황, 기업 벤치마킹가 포함되어 있습니다.현재 시장 규모는 통상 시나리오에 근거하고 추정되고 있습니다.

이 장에서는 이 시장 주요 방위 프로그램을 채택해 이 시장에서 신청된 최신 뉴스나 특허에 대해도 해설합니다. 또한 국가 레벨 10년간 시장 예측과 시나리오 분석에 대해도 해설합니다.

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카공화국

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

The Global Aerodynamics Testing and Simulation market is estimated at USD 2.25 billion in 2025, projected to grow to USD 6.37 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 10.96% over the forecast period 2025-2035.

The defense aerodynamics testing and simulation market plays a pivotal role in the design, development, and operational refinement of military aircraft, missiles, and unmanned aerial systems. As defense platforms become more advanced, their aerodynamic performance directly impacts maneuverability, survivability, fuel efficiency, and mission effectiveness. Testing and simulation allow for the safe and cost-effective evaluation of these performance parameters under controlled and extreme conditions. Wind tunnels, computational fluid dynamics tools, and virtual flight environments form the foundation of this market, offering engineers and strategists the ability to model airflow, heat distribution, and pressure dynamics across complex airframes. These capabilities are essential for validating new designs, improving legacy systems, and ensuring optimal performance under variable environmental and combat conditions. Aerodynamic simulation also supports stealth optimization, weapon integration, and high-speed flight planning-key elements in modern warfare. Furthermore, these technologies contribute to strategic planning by enabling accurate modeling of vehicle behavior in real-world scenarios. As aerial warfare becomes more dependent on agility, speed, and low observability, the significance of aerodynamic testing and simulation continues to grow. This market supports not only research and production but also the continuous adaptation required in today's evolving threat environments.

Emerging technologies are transforming the landscape of defense aerodynamics testing and simulation, enabling greater precision, scalability, and realism in both physical and virtual environments. High-performance computing has revolutionized computational fluid dynamics, allowing analysts to simulate highly complex flow conditions with unprecedented accuracy and speed. These digital models can now account for multi-variable scenarios, including turbulence, thermal loads, and interactions between control surfaces and embedded weapons systems. The integration of machine learning further refines simulation outputs by identifying performance patterns and optimizing design iterations based on vast datasets. In parallel, next-generation wind tunnels have evolved to simulate extreme altitude and velocity conditions, supporting the development of hypersonic platforms and maneuverable glide vehicles. Virtual reality and immersive interfaces are also beginning to influence how engineers and pilots interact with aerodynamic models, providing intuitive insights into airflow dynamics and vehicle behavior. Moreover, cloud-based simulation tools are enabling global collaboration and secure data sharing among defense contractors, research institutions, and military clients. This technological convergence is not only reducing development cycles but also enhancing system validation, contributing to more agile and adaptable defense platforms capable of operating in contested and complex aerial environments.

Several key factors are propelling growth in the defense aerodynamics testing and simulation market. One of the most significant is the increasing complexity of aerial combat systems, which require advanced aerodynamic profiles to meet evolving mission demands. Military aircraft and missiles must perform reliably across a broad spectrum of speeds, altitudes, and atmospheric conditions, which necessitates rigorous testing and high-fidelity simulation. As stealth becomes a baseline expectation in modern airframes, aerodynamic shaping must be optimized to support radar evasion while maintaining performance and stability. The rise of hypersonic technologies has introduced a new frontier in airflow behavior, demanding simulation tools that can handle extreme thermal and pressure conditions. Additionally, the push for reduced lifecycle costs and more efficient platform development encourages the use of virtual testing environments that minimize reliance on costly physical trials. Training and mission rehearsal systems also benefit from aerodynamic simulations, helping aircrews understand the handling characteristics of new or modified platforms. Meanwhile, growing interest in multi-role UAVs and loitering munitions requires aerodynamic refinement for endurance, payload, and maneuverability. These drivers highlight the expanding role of aerodynamic testing not just in development, but also in ensuring mission readiness and operational superiority.

The global defense aerodynamics testing and simulation market exhibits distinct regional profiles shaped by national priorities, industrial capabilities, and investment in advanced aerospace systems. In North America, particularly the United States, the market is supported by a robust defense R&D ecosystem and an extensive infrastructure of wind tunnels, simulation labs, and flight test ranges. These facilities play a central role in supporting next-generation aircraft programs, hypersonic weapons development, and integrated air defense platforms. Europe places strong emphasis on collaborative research initiatives and multinational defense programs, which has led to shared investment in advanced simulation capabilities and digital design hubs. Countries like France, Germany, and the United Kingdom maintain dedicated testing facilities that support both national and joint aerospace development efforts. In Asia-Pacific, rapid advancements in indigenous defense aviation programs are driving demand for domestic simulation and testing capabilities. Nations such as India, China, and South Korea are expanding their technical infrastructure to reduce dependency on foreign validation and accelerate their own aerospace timelines. In the Middle East, interest in defense industrialization is leading to partnerships with international aerospace firms to develop local capabilities in aerodynamic modeling and verification. Each region's trajectory reflects its strategic objectives and evolving role in the global defense landscape.

The Future Combat Air System (FCAS) is a cornerstone of Europe's efforts to maintain sovereignty in defense and security. At the heart of FCAS lies the Next Generation Weapon System (NGWS), forming the foundation of a sophisticated "system of systems." This integrated network will feature manned New Generation Fighters operating in tandem with Unmanned Remote Carriers, all seamlessly connected through the "Combat Cloud"-a secure data network linking assets across air, land, sea, space, and cyberspace. These interconnected platforms will function as sensors, effectors, and command-and-control nodes, supporting rapid and flexible decision-making. The architecture behind FCAS is open, modular, and service-oriented, allowing for the integration of future platforms and emerging technologies. National and allied assets will complement the NGWS by contributing their distinct capabilities, enabling a truly collaborative combat environment across multiple domains through the combined strength of interoperable, networked systems.

Global aerodynamics testing and simulation market- Table of Contents

Global aerodynamics testing and simulation market Report Definition

Global aerodynamics testing and simulation market Segmentation

By Test method

By Technology

By End Use

By Region

Global aerodynamics testing and simulation market Analysis for next 10 Years

The 10-year Global aerodynamics testing and simulation market analysis would give a detailed overview of Global aerodynamics testing and simulation market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global aerodynamics testing and simulation market Forecast

The 10-year Global aerodynamics testing and simulation market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Global aerodynamics testing and simulation market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Global aerodynamics testing and simulation market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Global aerodynamics testing and simulation market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Global aerodynamics testing and simulation market

Hear from our experts their opinion of the possible analysis for this market.